Updates on Websol

-

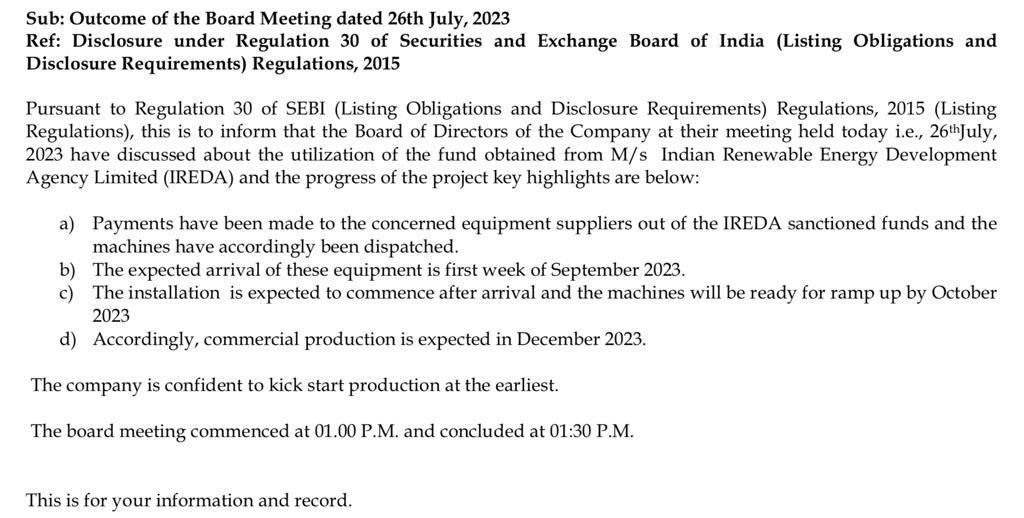

Loan received from Ireda 179 cr

2 . Timelines uploaded

-

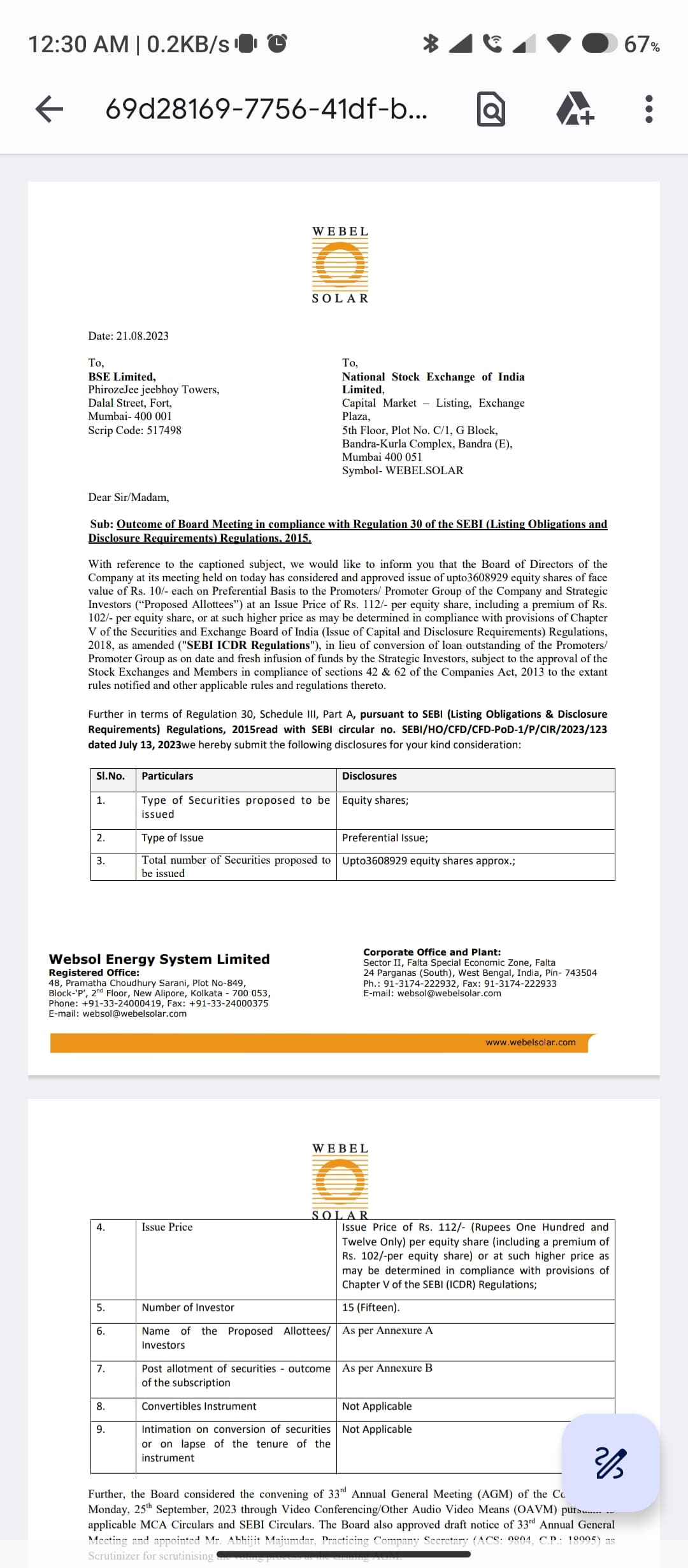

Preferential raised at 112, 36Lakh shares

-

Strong Charts – Monthly looks set to breach multi year high of 172

Summary of Websol for someone new

Websol is mainly engaged in solar cell manufacturing company located at Falta SEZ in Kolkata….company was established in 1992 and public issue by 2002

Company had very rough years till 2016……after safe guard duty implemented company managed to come out of BFIR and wipe out all most all the debt of around 150cr or so in past 5 years

Company as on 2023 March has debt of only 27-30cr

Company’s plant was closed from 1/4/2022 due to old technology plus custom duty on solar cell and module

In March23 company got IREDA loan of 179cr for 1st phase of 600MW cell and module plant

Plant is expected to arrive by September and commercial production is expected by December

New plant is with either mono perc or topocon technology

Company is going for 1.8GW solar cell manufacturing by 2024 end

This is the only listed company manufacturing solar cell while solex Waaree and others are mainly in module manufacturing or EPC companies and planning to go for cell manufacturing in coming years

Websol has very good technical team which will keep company ahead of their competitors

From the first phase we expect around 500cr plus revenue from cell with EBITA in the range of 15-20%

From full expansion of 1.8GW solar cell manufacturing we expect 1500-1600cr revenue and around 100-120cr NP with diluted equity of 50cr

We had not calculated any module manufacturing revenues and PLI benefits in our estimates

Solar cell is heart of solar module and it’s having very good EBITA margins of 15-20% while module manufacturing EBITA is 5-8% only

This is just the general view of the company.

Even at 1.8 GW we can achieve turnover of 1500-1600cr and EBITA of 300-320cr and PAT of 110-125cr which means EPS of 20-22 with diluted equity of 50cr

Company has carry forward losses so no tax burden for at least 2-3 years plus here I had not calculated any PLI benefits or subsidy benefits and plant efficiency of 80%

This is very good for turnaround company to achieve in next 2 years and if they achieve above figures then 30-40 PE will be given……rest time will tell