Premier energies IPO opens for subscription from 27th Aug 2024. Market will decide the valuation of pure play Solar cell and module manufacturer’s. Premier energies has 2 GW Cell & 4 GW module capacity with an order book of close to 6000 Crs. Though, it has presence in other verticals like EPC, IPP & O&M, the order book is negligible.

Waaree energies is valued at Mcap/sales of 8x in unlisted zone (FY23 sales).

Let us hope that listed competitor Websol energy gets benefited with the same valuation of 8x to FY25 sales from market as it has better margins than others as of now. Fingers crossed. Please share your views.

All - sharing a IPO document by Niveshaay on Premier Energies. It gives a good view of how things stack up against the peers for Websol and the solar industry prospects in India.

Websol Annual Report.pdf (5.8 MB)

A very interesting Annual Report was published by Websol. My key takeaways were that the company is looking at a 4x expansion in by FY 27 on its current cell business of 600 MW. Apart from that they might get into commercial wafers and ingots production apart from captive use and this might help them retain good margins. Also, they are entertaining getting into solar rooftop EPC side of the business.

With all these optionalities I see this company as a 25000 cr Mcap business in next 2-3 years if they are able to execute professionally like they have till now.

Disclaimer ~ All disclaimers are useless, we are all responsible for our own decisions. I am currently 92% net wealth invested in this company and I am up almost 90% in one month. This makes me biased but at the same time, I can sell and switch to any company without being liable to inform. My projections of 25000 cr mcap comes from a topline estimation of 2500-3000 cr topline with 10 Mcap to Sales and an assumption that 2-3 years down the line the company will be aspiring to reach 5gw capacity and hence the elevated exit multiples shall be assigned. Also, Premiere Energies with a Quarterly Topline of 1600+cr and almost 50,000 cr Mcap will be a good North Star metric for a company like Websol. There is no reason why Websol cant be 2-3 years down the line where Premiere is right now

Ending my Disclaimer with the theme of the Annual Report

“BOLDNESS IS EVERYTHING”

Hi Friends,

I was busy with a personal work last week. so, couldn’t read the AR. However, with the announcement of the appointment of Mrs. Ritu S Jain as Non-Executive Independent Director of the company, it is clear that the management is very keen to tap on the EPC business as early as possible.

She is the chairman of SR Corporate consultant Pvt. Ltd which is majorly into Solar EPC business. Her experience will surely help Websol to venture into EPC as quickly as possible.

Please refer their below website for further details.

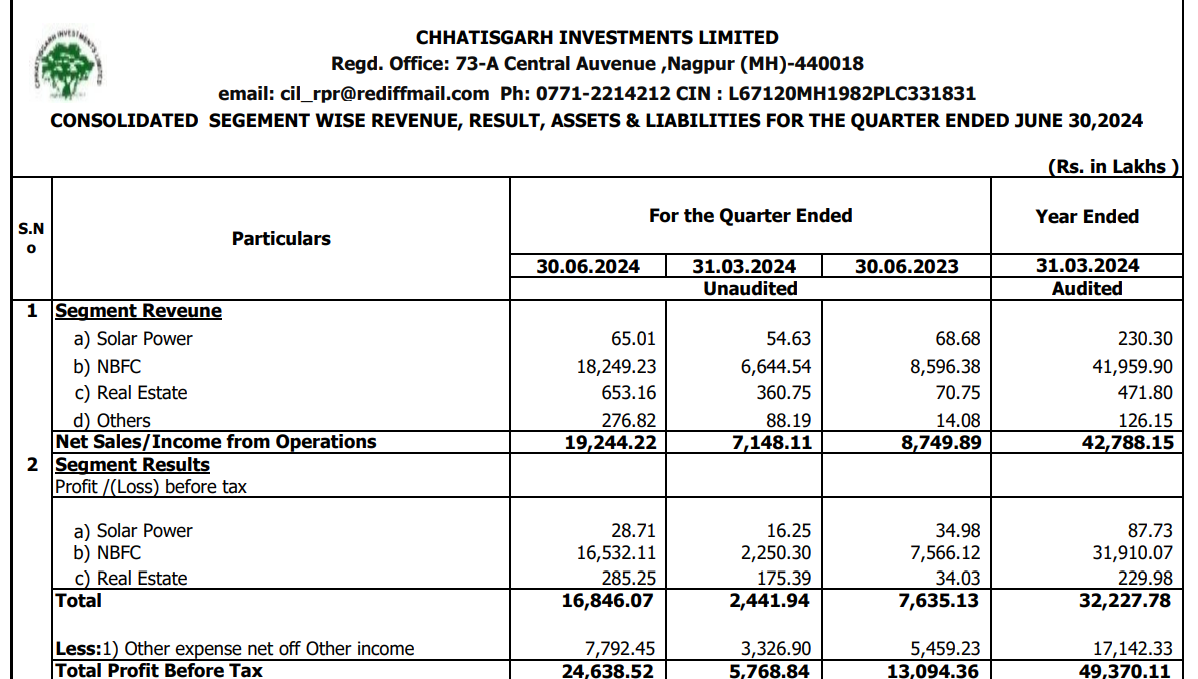

She is also a director at Chhattisgarh Investments Ltd -CIL (Websol disclosed in their annexure) which is majorly into NBFC and also has solar power generation & Real estate as minor business. Her Business network in NBFC circle will surely help Websol to secure funds if required for their upcoming ambitious phase-2 expansion plan.

The Q1 FY2425 performance of CIL is appended below.

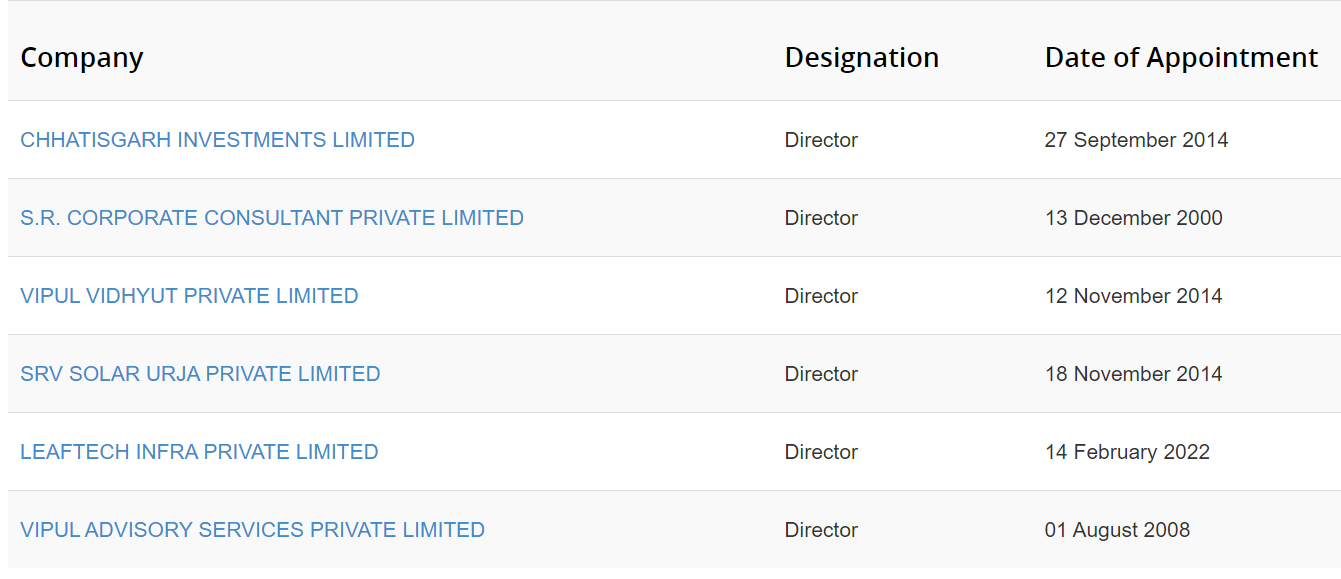

She is also holding position as a Director in the below companies. Mostly Solar power generation and real estate related companies. Real estate plays a important role in securing the land required for installing the solar power plants as it decides the cost/Wp.

Just my views, I may be wrong. So, please share your anti -thesis if any as it will keep us vigilant, unbiased and neutral in processing the information available to us.

I will share my comments after completely reading the AR if any interesting thing is there other than already publicly available information.

Too many big players are entering into this space Solar manufacturing and epc business like Tata power, Adani, newly listed premier etc.

2 Many are also working on backward integration. This space is getting overcrowded due to favourable government policies for green energy.

In this space many companies have big order book unlike websol.

Opportunities:

Websol is still trading at cheap valuation 35-40 forward pe based upon last quarter earnings. I think websol will also catch up premium valuation once it show good QoQ results.

Their full capacity utilisation will be completed within 8-12 months which offer lucrative opportunities.

However, I recently added more quantity but still I am trying to figure out weather should I hold it for long term? My main worry is competition in this space. Please share your knowledge in this regard. Thank you

Of 170 GW of demand, what makes you worry about competition? How can Adani, reliance and Tata with a manufacturing capacity of 10 GW each fill this 150GW void? Please enlighten us.

As of 2024, India’s solar manufacturing capacity is growing significantly. The country’s solar PV module production capacity has reached about 40 GW annually, with major companies like Adani Solar, Vikram Solar, and RenewSys, premier energy etc leading the charge. Several more expansions are expected, with the goal of ramping up capacity even further in the coming years.

On the demand side, India’s solar power installation target for 2024 is estimated at 20 GW annually, driven by government initiatives to boost renewable energy adoption as part of its 500 GW renewable energy target by 2030. Now rest of the calculations you can do easily.

So as per the India’ s targeted installed capacity is fairly balanced with new plants. However, internationally indian manufactured Solar panel demand is rising as US and other countries put ban on Chinese solar panel. So personally I am very bullish on this sector.

This EPS is for cell manufacture only. The 550 MW module capacity has started in August. So it will add to the cell EPS and annualized EPS can be much higher than 25.16

Hi, as they need to raise funds for next phase of growth, equity will be diluted, and eps will be less than what we think. So better not to evaluate by PE basis. I am also feel for next 12 months they will have super growth, however by that time two things needs to be monitored 1. The new capacity of bog players coming into market 2. How fast websol do scale up by raising capacity from 600 MW to 1800 MW

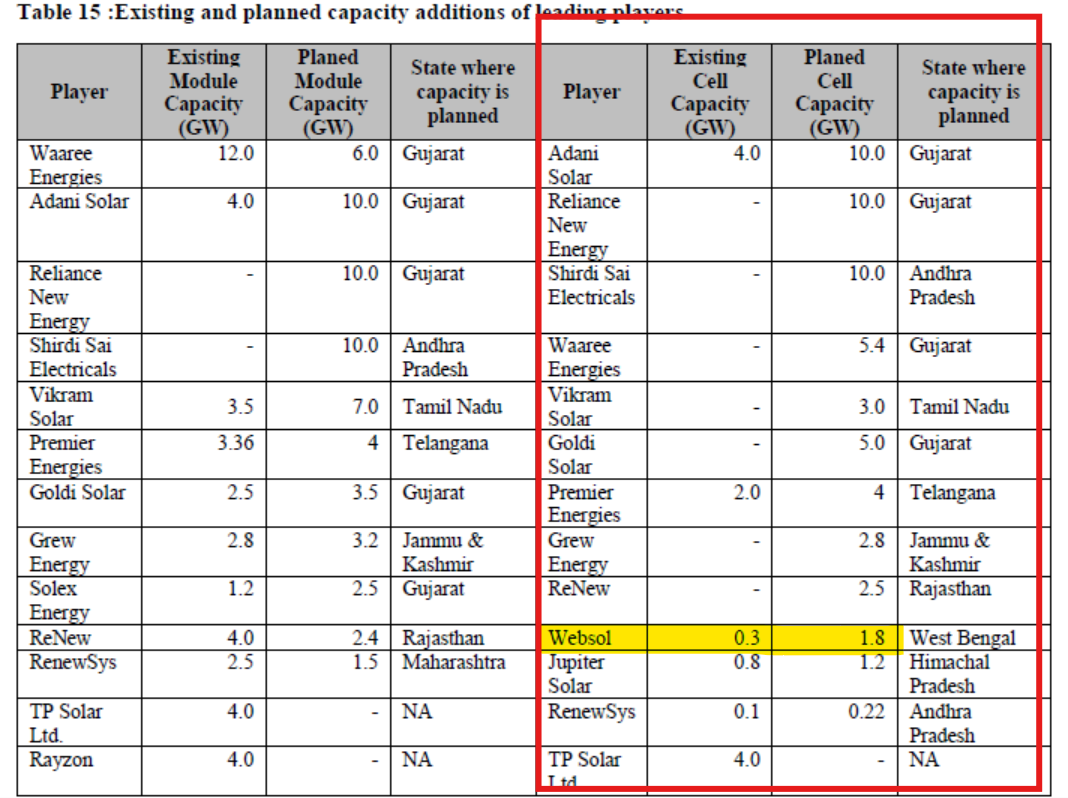

As you can see, 45 GW of modules Vs 11.5 GW of Cells (Websol is 0.6 GW cell & 0.55 GW Module). The Ultra big player’s capacity will be consumed internally for captive projects. Pure play non-captive player shall supply to the Indian market/exports.

The Solar Cell demand-supply gap is huge for next 5-6 years. Absolute free run till 2027 for Websol as proposed Cell capacities will come live by that time only. Even then if Govt. Policies remains same, Solar Cells will the most sought after product till 2030.

However, Websol’s phase-2 is big dream for their size as funding requirement would be close to 1000 Crores to establish 1.8 GW Cells. In the recently held AGM, Mr. SL Agarwal hinted on collaborating with a US based company for export of modules. Ideally, they should bring in some collaboration in manufacturing for the funding needs.

It should be noted that Vikram Solar’s existing factory is located just beside Websol’s Falta SEZ, Kolkata which is the sole reason for me to study this file. You can read this DRHP to understand the Govt. subsidies and tax related benefits which are being provided to SEZ players to promote export and reduce their overall manufacturing cost. Just my opinion.

The phase 2 execution is pivotal, but big players’ new capacity may not matter for the next 3-5 years as the demand is huge. Big players will not be able to fill the demand-supply gap until 2030 I feel.

This stock fits a lot of good boxes. Had spotted this earlier on and decided not to invest sadly but have taken a tracking position. My only worry is that the margins for such companies depends on the tariffs imposed by the govt. Borosil renewables also suffered due to this issue. Now the margins look great and a 1 year forward PE makes this stock dirt cheap compared to other players but time will tell if the margins can last.

Hi friends,

Only 8 companies registered themselves as DCR solar cell manufacturers and Websol is one of them.

Websol registered 242 MW solar cell capacity in DCR portal till now. It should become 600 MW by April 2025.

Company Name

KW

Jupiter International Limited

8,04,569.59

FS India Solar Ventures Private Limited

7,01,838.13

Premier Energies International Private Limited

5,84,023.63

Mundra Solar Energy Limited

4,22,083.81

Premier Energies Photovoltaic Private Limited

3,59,011.69

Websol Energy System Limited

2,42,451.16

Mundra Solar PV Limited

2,18,073.20

Tata Power Solar Systems Limited

1,97,671.80

DCR Solar module space is highly crowded. Websol is yet to register there.

The Solar cell margin is huge due to DCR requirement and i expect it to continue for next 2 years.

They have 600 MW capacity already live as per annual reports, I guess this registration form would be filled 1-2 quarters live ans Partial capacity would be operational at that point of time.