Here is a gist of Ahmed’s (invstr88) email exchange with the Waterbase management. No surprises there! All answers on expected lines regarding merger, insurance claim, capacity, impact of merger, comparison with Avanti.

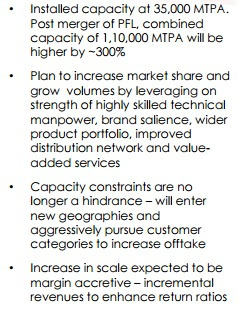

Question - PFL has 75k MTPA capacity at the moment. Any idea what is the current utilization levels of PF? PF is selling everything to WB (120 cr revenue in 2016) so how is Waterbase topline going to increase after the merger? Operational synergies might help bottomline somewhat, but that is the max one is going to get from the merger. PF has debt of 42 odd cr, which is coming along with some equity dilution. Why are the promoters in presentations advertising (three times the capacity, and they will be able to target newer geographies as there will be no capacity constraints post merger. My understanding is that we were getting whatever amount needed from PF before merger as well. So where were the constraints in terms of capacity? What can we expect out of this merger as far as topline and bottomline are concerned?

Ans - The primary objective for setting up PFL was to tap the growing business opportunity which wasn’t getting addressed given the limited capacity of TWL. Expanding capacities under TWL on its own got a lot more challenging post Canara Bank’s declaration of us as NPA. However, the promoter’s faith and commitment in the business along with the budding business opportunity it was eventually decided that PFL would be established as a separate entity with TWL being its only client and getting eventually merged with TWL. Pinnae Feeds Ltd. was incorporated in July 2012 and the full capacity was available from Farming season 2015.

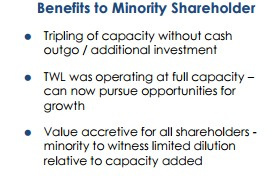

The benefits of the merger have been captured in the topline already to the extent of the prevailing demand in the markets over the last two years in the face of disease and natural disasters like floods. Entry into newer markets like West Bengal, Gujarat and Odisha over the last two seasons combined with sustained marketing efforts and the enhancement of the distribution infrastructure in existing markets is expected to result in increased volumes under normal demand / market conditions (i.e. absence of disease / non-occurrence of natural disasters).

In terms of profitability, it is expected that EBITDA margins should be positively impacted post-merger as the interest and depreciation in the books of PFL were already included in the purchase cost of traded goods in TWL’s books (given that these were at arm’s length). Post-merger, these expenses will revert to below the line items from an EBITDA perspective.

From a PAT perspective, the trend of steady increase in sales volume should provide positive momentum to the PAT which is expected to benefit from operating leverage as utilization increases. However, as a company policy, we do not provide any specific guidance either for Sales, EBITDA or PAT.

My take - MEANS NO IMPACT ON PAT DUE TO MERGER

Question - Why was this restriction imposed by Canara bank in the first place? And was this restriction really effecting WB as far as capacity is concerned? Waterbase was still getting whatever amount needed from PF.

Ans - The tsunami of December 2014 had a cascading effect on the business as it impacted the functioning of our key customers who experienced delays in meeting their obligations, in turn lengthening our receivables cycle. Cash flow and liquidity constrain impaired our ability to make timely payments. Canara Bank, which was part of the consortium, following their internal assessment classified us as NPA as they deemed the risk to the business had heightened to a large extent. The view was however was to Canara Bank only as the rest of the members didn’t agree to the same. Our borrowing cost went up following the NPA classification which in turn affected the project viability for the greenfield expansion.

However to circumvent the restriction, and to grow the business promoters incorporated PFL with the goal of eventually merging PFL with TWL. Had the above scenario not occurred, TWL would have undertaken expansion on its own without the need for PWL to be incorporated.

Question - Avanti is operating from the same region and is not complaining about diseases and stuff. Why Waterbase alone is facing these issues while Avanti is boosting its performance big time? I understand some companies are more efficient than others, but if farmers are facing diseases, then two companies operating in the same region must be having similar commentary.

Ans - Nellore is the core business area for both TWL and PFL. Besides the plant, WB’s customer base is also situated in that area. Avanti Feeds on the other hand is much bigger in size with a diversified presence, which reduces the concentration risk for the business. TWL as you must be aware, wasn’t able to fully capitalize on the business opportunities in the past given its limited scale, however post the amalgamation, we would be targeting newer markets to meet the growing demand which in turn will help us lower our geographic risk. We believe that the acute impact of the floods in 2015 and the disease outbreak in 2016 on the business was primarily owing to our concentrated presence and as such we are working towards addressing the same by widening our reach post amalgamation. Avanti Feeds, given their ability to shift focus to other markets, was able to insulate their performance from the impact.

Question - Is getting back the insurance amount IFFY? It has been almost 16 months and there is no concrete word from the mgmt yet on this. Do they care for minority shareholders?.Request to provide the name of the insurance company and its file no of insurance claim if possible.

Ans - The Insurance claim process is pending with the Insurance Co., and we are undertaking all requisite steps and following the necessary procedure. We do agree that the settlement procedure is taking longer than anticipated time but rest assure all the parties involved are going by the standard process. Also one needs to keep in mind that given the natural calamity covered a large area, there are numerous claims from this region and the progress of each claim, while certainly gradual, is progressing in accordance with availability of requisite technically competent manpower. The Company is constantly following-up with the Insurance Company.

TWL has however always kept shareholders abreast of the developments irrespective of the development being material or not, and we will continue to carry on with the same practice in the future as well.

Thanks for this Ahmed bhai!