This is my first post on ValuePickr, So please forgive any mistakes. I was going through the company called Waterbase and has come up with my analysis. Please provide your comments.

The company is into manufacturing of shrimp feeds and exporting it to the US,EU, Africa,Asia etc.

Their revenue has grown from 47cr in 2011 to 277cr in 2015 which is good 51% CAGR. Their net profit has grown from 0.7cr to 19.5cr, excellent growth.

The balance sheet is good with cash and equivalents of 30cr and debt of around 12 crore which means company is debt free at net level.

Equity is about 100cr so on 3.86 crore shares book value comes to about rs.26. Share is trading P/B of 3.8.

Promoters holds 52.47 % of shares none of which are pledged.

Growth drivers -

with an export size of 20000 crores there is tremendous potential to gain market share

with the amalgamation of Pinnea Foods the capacity will increase to 1,10,000 MTPA from 35,000 MTPA which should drive revenue growth

Management indicated they are starting hatcheries unit which should again aid revenue

Threat

if Rupee appreciate that will affect margins

need to look at balance sheet of Pinnea goods, it may have debt in the books which may burden waterbase balance sheet.

As per the annual report, below are the challenges and Threats -

The rainfall prediction for this year is not favourable.

An unfavourable monsoon would lead to increased input costs like feed and in turn may affect the growth of

shrimp farmers.

Delayed monsoon has affected power generation in Andhra Pradesh, which is one of the major producers of

Vannamei shrimps.

Andhra Pradesh Government has recently declared a day in a week as “Electricity holiday” for all industry.

This would increase the production cost of shrimp feed as well as increase the cost of shrimp production.

Any increase in the cost of Feed production would directly impact the net margins of the company.

The price of Raw Materials like Soya, Fish meal, Wheat etc have risen to record highs which continue to be of

concern to the industry.

Disease has devastated the shrimp industry in Thailand, Vietnam, China and Malaysia over the last few years.

India has been free of disease but like all living technologies, this continues to be a threat.

hi.

this is my first post.

just wanted to say that even i am quite excited abt the company as i find the export of shrimps picking up in a very big way to america & europe.

the reason i am excited is because i clearly remember that some years ago even Avanti feeds would be in the same spot & also after acquiring the subsidiary its capacity would increase by 3 times &

also 1 of the family members is married to soft bank vice chairman nikesh arora. softbank is a japanese bank. japanese cos r looking at investing in promising indian cos. in future it could be a possibility of going for a stake sale.

Disclaimer: i hv invested in this promising co.

this is in no way a recommendation to buy the stock.

thanks.

Pinnae Feeds Limited (PFL) which was incorporated in July 05, 2012 is a wholly owned subsidiary of KCTBL; the flagship company of the KCT Group of Kolkata which is one of the largest coal logistics and services companies of India. The KCT group which was promoted in 1929 by Late Shri Karam Chand Thapar enjoys significant presence in several sectors including coal and bulk commodities, infrastructure, capital and engineering goods, real estate, aquaculture and power trading. PFL is engaged into the business of shrimp feed manufacturing and has a manufacturing unit located at Nellore, Andhra Pradesh having an installed capacity of 40,000 Tonne Per Annum(TPA). The manufacturing facility of the company was established at a total cost of Rs.50.0 crore which was financed at a debt-equity ratio of 3:1. The manufacturing unit commenced commercial operation from July 02, 2014 onwards.The day-to-day affairs of the company are looked after by Mr.Ramakant Akula (CEO) and is well supported by an experienced team of professionals.As per unaudited results for M9FY15 (refers to the period April 01 to December 31),PFL reported a PBT of Rs.0.04 crore on a turnover of Rs.15.99 crore.

There is some discussion going on in Avanti feed forum. You can check for the kind of headwinds the shrimp export may face in near future and other ideas about the industry as a whole.

It looks like Waterbase is going to carry debt of Pinnae in their books. The topline of only 16cr and bottomline of 0.04 crore doesnt look very encouraging.

Waterbase’ cash can be used for reducing the debt of Pinnae Foods…

The figures are only for 9 months of 2014-15 and that too the operations commenced only in July 2014… So, only 2 quarters…

Debt equity ratio of Pinnae Foods is 3:1, so that shows why the profits were less…

Any business cannot make money from the beginning… So, can’t judge the performance of Pinnae Foods with just 6 months of operataional results available in public domain…

Waterbase will consider the merger along with Q1 results Board Meeting… Let’s see what comes out…

The key to consider in the merger is 3x capacity expansion in quick time can do wonders for Waterbase… Of course, after the operations result in the performance of the company… Let’s see how it goes…

Yes I agree. The tripling of capacity looks like a game changer.

I read the other thread on Avanti Feeds on VP, the voices there suggests imminent slowdown in the Shrimp exports.

in FY 14 - 15, Waterbase managed to clock topline of 277cr with bottomline of 19cr i.e. 7% NPM. So with tripling of capacity Waterbase should be able to atleast double the topline.

The following two things may affect their Margins,

slowdown in the industry

the interest outgo will increase with transfer of Pinnae Feeds debt

My estimate is that they would do about 360 - 380 cr in the current year (2015-16) and near 1000 cr by FY 2018. The industry does suffer from excess capacity right now and so margins may not shrink further. While the current year may only be marginally higher as compared to last year’s PAT margins of 7%, it should improve over the next couple of years to around 8 to 10% on account of their backward integration (setting up hatcheries) as well as branding exercise.

So let’s see for FY 2018. 1000 cr topline, 80 Cr PAT. EPS of 20. A modest pe of 10 around that time would put the price at 200 implying a doubling from the current levels of Rs.100 over a 3 year period.

Risks -

The Vannamei shrimp has been largely disease resistant, but who know how the viruses morph?

Execution risk is another factor to be considered.

Disclosure - I hold a small position bought at around Rs.70 levels a few weeks back.

One key factor why this company warrants investment is…the management & entry barriers which are strong for any compete to enter in this industry. Be invested for long term… It will give multiple returns…

Hi,this is my 1st post.Just to tell that Softbank is not a Bank but 2nd largest phone co. In Japan after NTT.It baught Sprint in USA and invested in various business in diff.countries led by Masayoshi Son,actually of Korean origin Japanese national.He has excellent business acumen n huge cash .If he show interest in waterbase it will get huge boost…

Also to mention,Japan is still cautious about Indian prawn as in recent past lots of cargo failed for pesticides and returned to India.If all is well Japan market will boost in future.

I am not invested but thinking to buy soon.

Waterbase Limited announces merger ratio for merger of Pinnae Foods Limited

No cash outflow for the merger

4 shares of Waterbase Limited will be given for 17 shares of Pinnae Feeds Limited

Pinnae Feeds Limited has an installed capacity of 75000 MTPA at Nellore

Capacity of Waterbase Limited will triple from 35000 MTPA to 110000 MTPA

Expected completion of merger by Q1FY17

KPMG is the advisor for the transaction

The paid-up capital of Pinnae Feeds Limited is Rs. 10 crores and with this merger ratio, the equity capital of Waterbase Limited will increase by 2352941 shares or Rs. 2.35 crores… Debt as per CARE rating is Rs. 77.20 crores… These are my assumptions as per data available on internet…

Negative:

Debt will increase, but Waterbase has almost 30 crores cash… So, shouldn’t be high I feel…

Note: Have vested interest… So, take my assumptions with a pinch of salt…

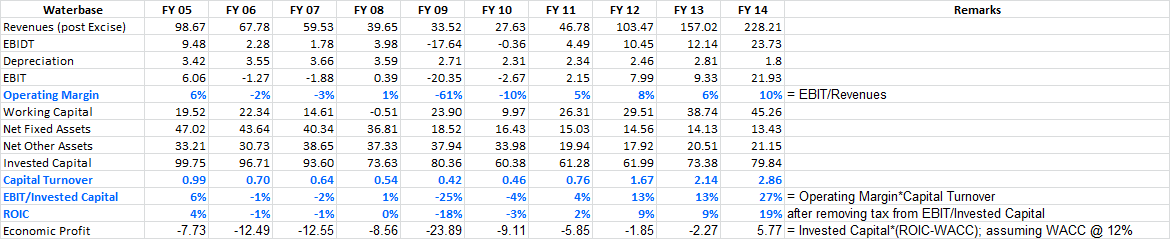

The way i see it is that the company has now started on a path of creating high ROIC and Economic Profit. It would be interesting if someone could do the same exercise on Avanti Feed so that we can compare these two businesses.

The numbers are from screener.in, if there are any mistakes or changes that need to be made let me know (I am new to equity analysis).

Disc: Hold a few shares at Rs.100 level. Currently trying to increase my confidence in the company.

Expansion undertaken in 2 phases; Phase I which was completed in FY15 comprised capacity of 40,000 MTPA and Phase II which was completed in FY16 comprised the balance capacity of 35,000 MTPA

Commenced commercial operation in H2FY14; supplied 6,062 MTPA of feeds to TWL during FY15

Post completion of Phase II - Capacity of 75,000 MTPA is now fully operational

Aims to supply ~15,000 M.T. of feeds to TWL during FY16

Capacity tripling on nil cash outflow…

Another key point to note was this: Expansion could not be undertaken within TWL due to restrictions placed by one of its bankers…

The Waterbase Ltd, a leading manufacturer of high quality shrimp feed, has launched ‘Bay White Enriched’, a new generation shrimp feed formulated with essential nutrients required for producing healthy shrimps.

Bay White Enriched is a mixture of highly digestible marine and vegetable proteins matching the ideal protein specification for the Vannamei shrimp. The product contains natural sources of phospholipids, cholesterol and omega-3 fatty acids to fulfil the shrimp’s requirements for essential lipids.

Given the growth in shrimp exports which accounted for 67 per cent of the marine export revenues, good farming practices coupled with availability of quality seed and feed would help the industry to increase shrimp production.

The company’s major focus is to develop shrimp feeds that are high on nutrition and are anti-biotic free, Ramakanth V Akula, CEO, The Waterbase Ltd, said in a release.

Bay White Enriched is available in all the Waterbase dealer outlets across the country.

Had a talk with IR team. The person gave a brief idea about the business. He told that the company will go for its first hatchery this year at a cost of 12 crores. Each hatchery gives 20 crores in revenue. Revenues from hatcheries will flow in FY 17 and onwards. EBITDA margins here are 20%.

Regarding the feed business - he told that there is huge demand - supply gap - demand being very less compared to overall supply. Supply is - 14lacs, demand is mere - 7-8lacs.

This will create pressure on margins. So what we see as 10-12% EBITDA margins will reduce in years to come.

Company currently processes 4000MT and doesnt want to expand it as of now. But company has entered into exports and wants to export all its 4000MT of processing one day (next 5 years). Sad part is exports provide a mere 2-3% EBITDA margins.

Industry is running in a rough phase. With much less bargaining power in the business and over supply, the coming business is going to be really tough.

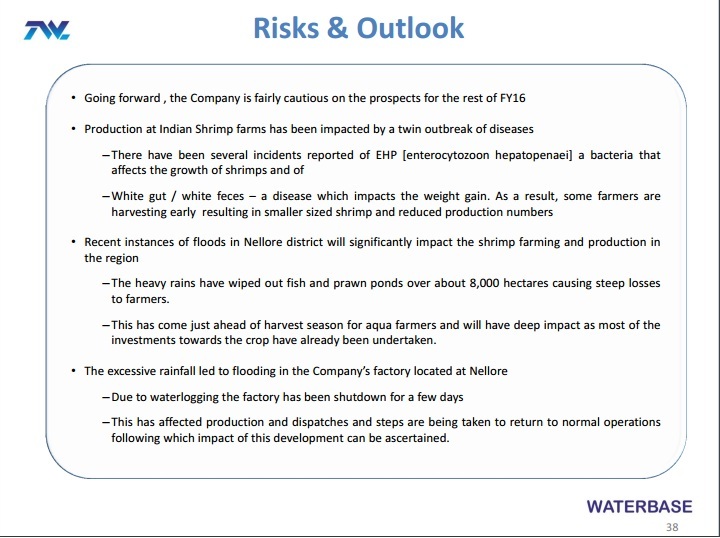

Adding to the worries, those who are expecting a good quarter result, flood in Nellore has destroyed the farming practise, leading to big impact on revenues.

Disc: Invested at 100 level. It is scary, if the IR team is negative about the business. Thinking to switch my investment.