Thank you for the feedback!

Avanti posts good results this Quarter And Water base has taken some cues with Avanti feeds … The Sea food exporters have Lobbied with MPEDA ( Marine products export authority ) to expand markets to South American markets like Chile , Argentina and Brazil to secure more orders . The sea food industry was at 5.5$ bn in 2014-15 which dwindled to 4.7 $ Bn . They are expecting a 9 % increase in the Unit realisation in 17 Fy .

Water base with 3 fold increase in Capacity utilisation etc and emerging into new product as per managements view should be able to capitalise the changing environment and leveraging the internal factors .

Waterbase reported their Q4 and FY17 numbers today. Numbers are not that impressive nor is the management commentary. there is no reference to the Insurance claim as well.

While Avanti declared super results, Waterbase declares an average set - mangement says profitability was impacted due to rise in raw material price.

Disc : Holding a small tracking quantity. No transactions in the last 12 months.

I had sent below queries to waterbase on 9th june and received their reponse today.Its a bit lengthy but request you all to have a look at it and provide an input.

Results

- It’s been a terrific quarter in terms of demand, sales and prices wherein many companies posted robust performance and yet we posted only 11% growth sales. Avanti Feeds posted 50% increase in sales YOY and its profit margins are spectacular to say the least. Our dealer network increased but we are unable to find the same level of sales and its contrary in the sense q4 witnessed unprecedented demand and more than that we even increased our network then why such a dismissal performance when compared to whole industry.

A: There are some reasons to this for which we have to share a brief background. As you may recall that through the period 2010-2014 Waterbase was constrained for capacity while other players were able to implement capacity addition plans. Due to this, some of our large dealers decided to turn into feed millers by setting up their own plants. The attrition began in 2015 thereby impacting overall demand for the last two farming seasons. While there has been impressive progress in new markets in last two years, the loss of volumes from the exit of these large dealers has neutralised a large part of gains from new markets leading to moderate growth rates for Waterbase on a combined basis. Due to the unfortunate sequence of events pre-2014, Waterbase was the only feed company to have undergone this kind of impact. Had it not been for this loss of volume from dealer exits, Waterbase would have been in a position to match the volume growth being reported by other organised players.

Having said that, we are confident of our offerings across multiple business verticals. We have deep expertise in the feed business and our repository of Research & Development allows us to be at the forefront of evolving requirements of customers. In addition, we are scaling up and diversify our presence across the country and we are also working towards increasing our dealership network to develop our business. All the above measures though are in the early stages and as such would take time to deliver and transform the business. Lastly, we are also working towards improving our product mix, which should further accelerate our growth. We are confident that such strategic actions would help us in delivering a much better performance going forward.

- Going forward what kind of performance can we expect from the company?

A: The Company is focussed on growing sales volumes in order to leverage the combined capacity of TWL and Pinnae Feeds. Increase in dealers as well as strengthening of marketing and after sales team will allow us to enhance our farmer connect. There will be some benefit on costs as raw material prices have declined. The outlook for the feed business is cautiously optimistic. Given the large share of the feed business in the overall revenue mix, we expect this to positively contribute to the profitability profile of the Company

On the other business lines, the Company is incubating these businesses and expects to see healthy growth rates in revenues. However, as these businesses are currently in the initial stages it will take some more time for them to scale up to critical mass and contribute to profitability. Some of the key business initiatives are setting up of a hatchery; sale of farm care products, sale of frozen shrimp and crabmeat in the domestic market as well as processing and export of shrimps. We are confident that the above initiatives will strengthen the business model of the Company due to greater integration as well as more touch points for customers across the value chain. Most importantly there will be a improvement in sustainability for customers of TWL along with added advantage of traceability for Waterbase products.

Presentation

1 ) Quote “Capacity constraints are no longer a hindrance” Kindly explain in practical sense when was this a constraint ?Why we have to remind our company that its misleading to say there ever was a capacity constraint.

For the period 2010-2014 Waterbase faced a capacity constraint and was unable to cater to the entire demand from its customers and was rationing it production of 35,000 MTPA among dealers and customers. Due to being wrongly designated as an NPA by one of its bankers, it was unable to source growth capital at reasonable rates. The promoters of the Company stepped in to support the growth plans by financing the equity for the establishment of a feed mill within Pinnae Feeds. The Pinnae plant was to have manufacturing capacity of 75,000 MTPA available in phases. The construction commenced in FY14 and the first phase of the Pinnae feeds plant of 40,000 MTPA was commissioned in H2FY15 while the second phase of the plant was commissioned in FY16 raising Pinnae Feeds capacity to 75,000 MTPA.

Thus, the commissioning of Pinnae Feeds, in FY16, brought about a tripling of capacity (to 1,10,000 MTPA) from Waterbase’s then prevailing capacity of 35,000 MTPA. So for 5 long years, until commissioning of phase 1 of Pinnae Feeds, capacity was a constraint for the Company

Link: https://www.youtube.com/watch?v=y90aGX6jhk4

In the above video CEO states that Waterbase was stuck with 35k MT and were unable to service customers requirement and could not venture in to other states with Waterbase capacity and he states that they now have access to higher capacity. It baffles me as how Waterbase was restrained as PFL was part of same group and it has the capacity of 75k MT of which less than 50% was being utilized.

The feed manufacturing plant of the Waterbase Ltd. plant, when originally set up, enjoyed a capacity of 15,000 MTPA. In 2009, when the industry was faced with sharp spike in demand for feed due to increase in shrimp cultivation, the most rapid and suitable reaction was to de-bottleneck the plant, add new lines, undertake all steps to enhance capacity of the plant based on original design and layout. Following these initiatives, the Company was able to enhance capacity to 35,000 MTPA. For some years, Waterbase was constrained as it could not take capacity beyond 35,000 MTPA even as demand grew sharply.

The Pinnae plant was to have manufacturing capacity of 75,000 MTPA available in phases. The construction commenced in FY14 and the first phase of the Pinnae feeds plant of 40,000 MTPA was commissioned in H2FY15 while the second phase of the plant was commissioned in FY16 raising Pinnae Feeds capacity to 75,000 MTPA.

Prior to availability of capacity under Pinnae Feeds, the Waterbase Ltd. was running at full capacity and turning down customers. For those five years, due to lack of capacity, sales team at Waterbase were not able to expand presence in newer markets, did not pursue customer leads and / or enhance marketing efforts due to the constraint on capacity. Hence, there were constraints until the capacity of Pinnae was available.

- Waterbase entered Gujarat, West Bengal and Orissa 2014, 2015 and 2016.Kindly provide an update upon the sales in these 3 states in terms of volume.

Due to competitive sensitivities, the Company does not share state wise volumes of its feed sales. At this moment the Company can share that dealer network has expanded and the initial performance in the new states has been highly encouraging.

- Why same signages and dealers pics are there in the past 1 year of presentation.

The Company is updating the pictures in the latest Investors Presentations to be made after Q1 results.

- Why our market share is stuck at 7% for the past two years?

A) In FY15, after a strong start, the Company lost significant momentum due to floods in Nellore. In FY16, again after a strong start to the year, there was disease in the home market where the sales are concentrated. Further, while the Company has made progress in new markets, the Company has lost some volumes from few large dealers and customers who have set up their own plants. Thus, the sales volumes have grown only moderately in the last two years. At the same time, the industry was also hampered by incidence of floods and disease in last two years. There is also significant transfer of market share from unorganised players to organised players. Thus while some of the organised players are reporting strong growth, this is coming from market share gains and not purely from industry growth. Lastly, the overall industry numbers are not reported, especially by the unorganised segment. As a result, TWL has maintained its sales volumes and market share over the last two years.

B) Having said that, it is important to mention that maintaining market share is a credible development as a number of players have entered the segment lured by its potential which invariably has resulted in a heightened competition. The entry of newer players have also resulted in softening of the realisations as they have resorted to offering their products at lower prices in an attempt to gain market share. We have had to fend off a lot of competition and significantly tweak our business strategy and product mix in the area which has resulted in maintaining our market share. Sustaining market share is credible given the underlying changes which have been taking place in the market.

Amalgamation and Insurance Claim

- You have stated that NCLT requested for some clarification on 5th June, 2017 and company requested for 2 weeks to provide the same. Kindly elaborate what were the clarifications sought by the NCLT.

NCLT had requested for an affidavit containing the clarifications it had asked for. Both the Transferor and Transferee Company had submitted the affidavits containing the clarifications to NCLT within the 2 weeks’ time and we are expecting the order from NCLT shortly.

- Management talks about ethical business practices yet we fail to understand why it is shying away from declaring the status of Insurance Claim to the exchange as its been 18 months now and we are yet to hear it officially from the management on this.

The Insurance Company is following the due procedures to investigate the developments, assess the damage and process the claims. Given that this natural calamity covered a large area, there are numerous claims from this region and the progress of each claim, while certainly gradual, is progressing in accordance with availability of requisite technically competent manpower. The Company has provided updates on these developments proactively as can be gauged from the filings from the stock exchange. When there is material progress in the insurance claim the Company will duly communicate the developments in accordance with regulatory procedures. A matter such as an insurance claim is not driven or controlled by the company but by a third party. The Company will share details of the final position of the Insurance claim once all matters are completed. In fact, it is highly ethical for the Company to await full and final developments in the matter before communicating the same to the stakeholders. Further, in keeping with its spirit of corporate governance and ethics, the Company will also share such details on the appropriate forum and cannot be responding to individual shareholders based on query by email.

- Kindly share the name of the bank with which we had availed the insurance with relevant file/tracking no.

The Insurance claim is pending with New India Assurance Company and the Company has submitted all the documents with the Insurer. We are awaiting settlement of the claim.

- Doesn’t it look we are going forward at snail’s pace in terms of growth as its taking us more than 2 years just for amalgamation and if that is the case then it’s really difficult for a company claiming to be a pioneer in the industry to be able to match the industry requirement.

A) The Company is following the stated procedure pertaining to amalgamation and has on a timely basis complied with the entire regulatory requirement. The Company is following the law of the land and is subject to process prescribed by regulators. There has been no delay or lax from the Company’s end towards completing the process.

It would be more appropriate for investors to direct such statements and comments to the Finance Ministry, Company Law Board, RoC, SEBI and other regulators who can act on such feedback and hasten the process for amalgamation.

4)Can we expect setting up of Hatcheries to be completed by the end of this month as its already delayed from q4 fy17 to q1 fy18 even after relevant approvals were granted by the govt. of Andhra Pradesh on time.

Phase I of the Hatchery is nearing completion and we are now involved in operationalising the Hatchery.

Investors Meet

Q) In a span of one year we initiated 5 Institutional Investors meeting. Given the factors stated above why anyone will be interested to invest in our company when we are unable to match up with the market. Why aren’t we concentrating on matching up with the industry so that based on our performance Institutional investors themselves will have an eye on us. An excellent example is Avanti Feeds and now one can find many houses performing coverage on it.

A) Your feedback has been noted and will be acted upon by Company’s officials. The Management has been actively pursuing multiple initiatives to drive growth and elevate performance the results of which will be visible in coming quarters.

Q) It’s a good thing that promoters are increasing their stake in the company what is appalling is retail investors are being left in the dark on why nothing works on time on the waterbase front.

A) The Waterbase has made appropriate disclosures in its filings with the stock exchanges. The Waterbase Ltd. has been highly proactive in its communication with its shareholders and has undertaken significant measures to further its position in the industry with a view to create value for all stakeholders. It takes pride in its track record of wealth creation and is highly cognizant of responsibilities towards minority shareholders. An extensive examination of its record speaks for itself. Many of the points raised in your email pertain to delays by the insurance company, NCLT, etc. which are externalities and cannot be controlled or influenced by the Company.

Disc: Invested

8 Likes

Thx for this extensive follow-up. The fact is that this is a mediocre conpany, which is obvious from the answers regarding growth, market share, etc. They were unable to take advantage of the business tailwinds when others kept posting tremendous growth. Merger is just an eyewash! Insurance claim, well, we don’t know if the money would come, as the force majeure situations are typical. Regarding future, the fact is that they had full additional 75000 mtpa capacity available from last 1 year which they have been unable to put into use during last 1 year. How is merger going to help in future uf they are unable to grow despite 75k free capacity. Certainly the capacity constraint talk is just nonsense?

They are just happy for retaining their mkt share. Competition is there and increasing. Better to be with a company which has negotiating power, better proactive mgmt, and visible good growth trajectory.

I wonder that with both avanti and waterbase trading close to 35 pe, why will one invest in waterbase? Avanti is going to post two blockbuster results for h1, so fwd pe would ne much lower than 35. And there is no guarantee of better result in case of waterbase for h1…right?

2 Likes

Thanks for the follow up on this. My view is the management is trying for a smoke screen to hide their inability to scale up…They always had Pinnea capacity which they have not been able to fully utilize. Both Avanti and Waterbase are currently trading around same PE which may not sustain for Waterbase and as usual, this one may correct post Q1…While raw material cost has come down, this one is capable of saying one of significant expense towards merger of Pinnae…with every passing quater, conviction level only goes down…

Disc : Holding a small tracking quantity. No transactions in the last 12 months.

1 Like

@Mridul you are right mridul. What ever they are saying is not something which a company states when whole industry is performing extremely well.Any idea about share holder “NISHITA KIRIT SHAH” ? She is director of precious shipping which owns 44 ships and one of the richest in thailand. Why waterbase didn’t care about tie-up with any major with thailand based company like how avanti did is something which i am curious about.

@tbhavesh As they are yet to confirm about pinnae and WB merger they won’t be able to publish pinnae results and when they do it will have expenses which will be more than our expectations for sure.Lets hope for the best for minority share holders.

Waterbase declared their Q1 numbers today…I am really disappointed with teh numbers.

-

Revenue has gone down marginnally from 135 Cr to 131 Cr. They are unable to expand / grow.

-

Cost of Raw material has gone down significantly from 49 Cr to 34 Cr. - There is nothing great that the management has done here.

-

Employee Expenses, Finance cost, Other expenses have all gone up.

-

Net profit has gone up from 8.9 Cr to 13.4 Cr - this is solely due to decrease in Raw Material cost. Had the raw material cost not gone down, this company would have declared loss…

http://www.bseindia.com/xml-data/corpfiling/AttachLive/d4f2b03f-8321-4f4c-9912-5fe59e8a69ca.pdf

Disc : Invested…planning to move out soon

5 Likes

does waterbase will be affected if this happens ?

apex frozen foods? anybody read the documents ? how is it vis a vis waterbase

http://waterbaseindia.com/online_pdf/Investor%20Presentation%20August%20,2017.pdf Investor presentation… deleted earlier post had pasted a wrong link

1 Like

Excellent result posted by waterbase Limited we can expect Bounce of price from here.

Stock locked in at upper circuit today. In last one month its up more than 60% and more than double in last 3 months. Any specific news due to which its running high. At the same time Avanti feed which is better in every aspect from waterbase has not seen any action.

Is it because waterbase was undervalued when valuations are compared with Avanti and Mr. market is assigning the similar valuations like Avanti to waterbase. Or thier is something else.

Please share your comments.

Disc : Invested

Avanti Feeds has appreciated almost 6 times in last 12 months.

The reason for the exuberance is the rise in Processed Shrimp demand and the fall in Raw Shrimp prices. I don’t really see the company otherwise operating a good business in the past. The erratic EPS looks highly risky.

1 Like

3 Q working is important as now the capacity of waterbase is almost 25 % of Avanti. But the gap in price is too high. Dislosure : Invested

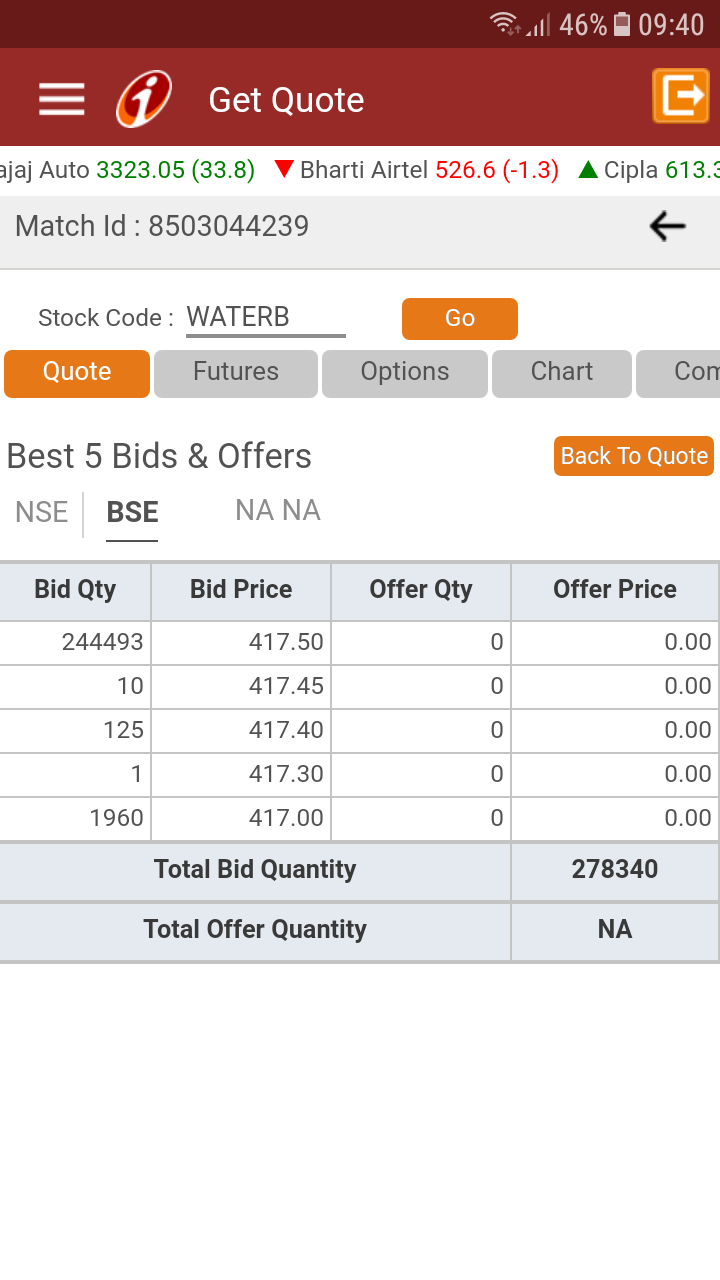

Is this price manipulation?

Yesterday there were bids for >200000 shares at 397 and today similar quantity at 417.

its the bids at circuit, so its expected. how is it manipulation?

Water base results have come.Q3-2017 vs Q3 - 2016 the results are good. 9 months last year vs 9 months this year also good. Yes q3 perf vs q2 performance. Q3 is lower due to seasonal - cyclical nature of business. Management forward commentary is good.

It is a turnaround company coming out from loss and getting into huge profit zone. Now PE ratio looks high but in next few quarters PE ratio will come down drastically. This business will do great for next 5-6 years at least. All companies will do well. Indian companies are taking the space vacated by China and Vietnam. As government is giving support to rural income and export there will be positive surprise. Just 25 days back Government allowed duty drawback to make our shrimp export more competitive. May be biased views are invited

(disclosure invested)

2 Likes