-

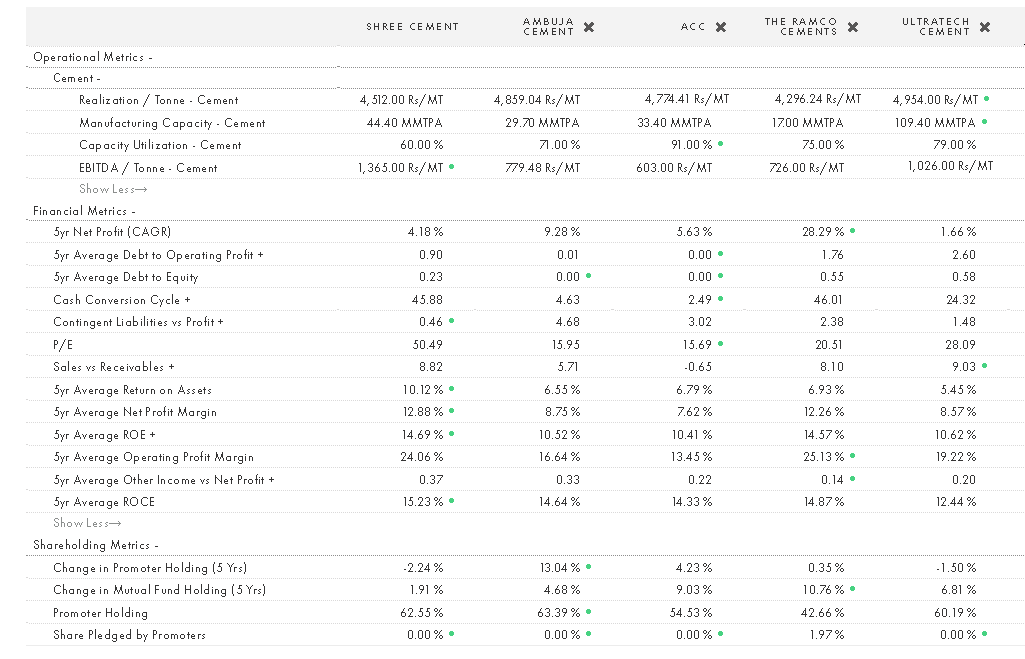

Find cost of production/ton for all cos and rank them in terms of best to worst

-

Find benchmarks of cement deals and see what was the cost of production for those cos

-

Find where your selected co lies in those benchmark

-

Check Debt Levels, corp governance issues etc

3 Likes

Hey @ashwinidamani why market is giving so low valuation to Ambuja/Acc?

–Debt free balance sheet

–Strong Brand,Distribution,Strategic Plant Location across India,Experienced Management

–improving OPM,Utilization

–Yes Cost structure is little bit strch(EBITDA/Tonn is less wrt Shree but comparable with ramco)

and on other side Ramco & Shree are still at exorbitant price ?

–RM /Cost structure is one reason but such huge valuation Delta ?

Any other Reason?

You have given a good understanding of business … but a bit on how to value this sector ??

Cement is low or at max medium ROCE business with single digit Gr or Flat Gr in profit for years together … Largest player too is not able to rein in debt or interest cost

Inspite of consolidation it still has large number of players – Why then PE is so high from 20s unto 50s …

If we consider Cement as Cyclical as you have stated and we ignore PE - even P/B is too high … ranging from 3 to 8 in some case … Even EVEBITDA in this down market for Real estate / general construction for Ultra tech is >12 and Shree Cement is > 18 …

I am not able to understand where is optimism coming from ??

What are international benchmarks for valuing this sector ??

Lack of Growth mindset. Their parent is in deep stress and has agenda of its own. ACC/Ambuja are being run on guidelines of MNC Parent with little or no regard to India Realities.

Their purpose is to throw cash to help parent and just be self sustainable.

Having said this…Value might be emerging here

2 Likes

HI Ashwini Damani,

Thanks for the detailed thread. I just had few questions. Would be glad if you can reply.

a. Why UltraTech Cement is able to earn higher realizations/tone as compared to the industry? As cement is a commodity and pricing power is almost nil, am a bit surprised on the realization front

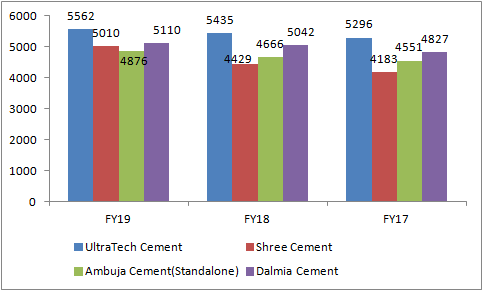

Realizations/Tone of Cement Players

Is it because of the fact that UltarTech has the leading market share in term of capacity? Here is the market share as per capacity it commands in some of the geographies:

| Market Share on the basis of Capacity as of FY19 | North | West | Central | East | South |

|---|---|---|---|---|---|

| UltraTech Cement | 23.3% | 33.9% | 34.0% | 12.7% | 12.9% |

| Shree Cement | 25.8% | - | - | 9.3% | 1.9% |

| Ambuja Cement | 11.5% | 10.8% | 5.5% | 1.4% | - |

| ACC | 8.7% | 5.9% | 6.9% | 2.6% | 7.7% |

| The Ramco Cement | - | 1.5% | - | 1.0% | 9.2% |

| Dalmia Cement | - | - | 4.2% | 12.8% | 7.6% |

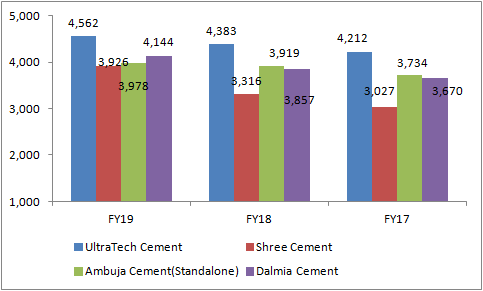

Question 2: Despite having a huge capacity base & enjoying economies of scale, the cost/tone of UltraTech is higher as compared to other players. Am really not able to reconcile why the cost/tone is higher for UltraTech. Could you please throw some color on this.

Cost/Tone of UltraTech as Compared to Others:

Question 3: The Clinker to Cement Factor of UltraTech stands at 78%. It is quite higher as compared to peers. Could that be the reason for the higher costs?

Warm Regards,

Parth Parekh

Disc: Invested in UltraTech Cement

Hi Ashwini Damani,

Thanks for the detailed thread. I want to understand the percentage of costs in the cost structure which are controllable in the hands of UltraTech.

Here is the break-up of costs for UltraTech Cement for FY19. Almost 59% of the overall costs are incurred on power & fuel and logistics cost.

| Particulars | FY 19 Cost Bifurcation of UltarTech Cement (in crore) | As a % to Overall Cost | Expenses Includes |

|---|---|---|---|

| Increase/Decrease in Stock | -120 | -0.4% | . |

| Raw Material Consumed | 6648 | 21.7% | Limestone, Fly Ash, Slag |

| Power & Fuel Cost | 8428 | 27.5% | Petcoke/US Coal & Cost of Running Captive Power Plants |

| Employee Cost | 2059 | 6.7% | . |

| Other Manufacturing Expenses | 2666 | 8.7% | . |

| General and Administration Expenses | 419 | 1.4% | . |

| Selling and Distribution Expenses | 9627 | 31.4% | Diesel & Freight Expense |

| Miscellaneous Expenses | 928 | 3.0% | . |

| Total Cost | 30655 | 100.0% | . |

Petcoke, Diesel, Logistics & cost of power generating power seems to be market determined. So, 60% of the cost are linked to market rates and not controllable. Is this assessment correct?

Further, planned shutdowns are also compulsorily taken in a year which is a fixed component. There cannot be savings on this front.

So, what i am trying to understand is what proportion of expenses are controllable in the hands of cement players? Which are these expenses? And how players such as Shree Cement, Ambuja Cement, Dalmia and Heidelberg are able to keep its cost structure low (i.e ex-depreciation)?

Hello Ashwaini

I took your work and tried to get more insights into it. I calculated a lot more ratios and tried to see which stocks are attractive.

Below are some other observations I have.

-

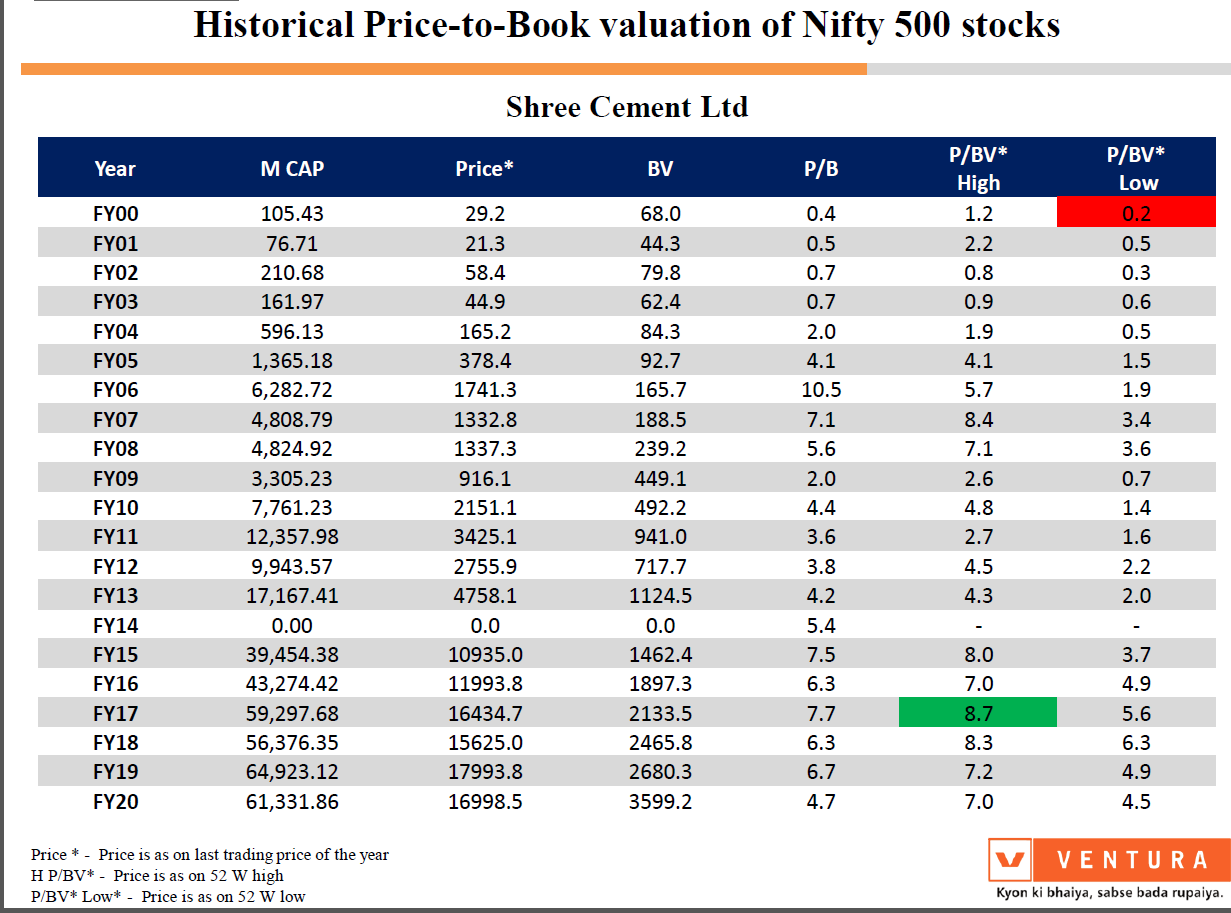

Shree definitely is doing great because of low debt and high EBIDTA/Ton. However, the stock is trading at 6 times Book Value.

-

There has to be a minimum utilization factor for the plants to remain functional. With demand dropping precipitously, those companies which have were having higher utilization % previously would be better placed.

-

Where will the partial lockdown be lifted first? In states and districts which don’t have as many cases. Mostly the eastern states (Bihar, Chattisgarh etc). So, companies here can be faster to restart operations. Also, in South or West, there would also be a paucity of labour to be able to restart.

-

When the complete lockdown is lifted, it is a possibility that while Real Estate would see muted construction activity, govt driven infra would be pushed. Again where would this be mostly done? States where infra improvement is required. Again it points to Eastern & North Eastern states.

Attaching the excel as well, if others want to work on top of it.

Cement.xlsx (11.2 KB)

7 Likes

Hi Ashwani, thanks for the insights on the industry. Could you also tell us the dynamics of White cement. I believe Ultratech and JK Cement are the only companies which can manufacture White cement in India. My basic knowledge on white cement is that it is used for decorative purposes and is more expensive than the Grey cement.

Any insights on the dynamics of demand, EBITDA, reason why only these two companies have capacities of white cement would be helpful. thanks

As of now more than 50% cement is used in housing sector out of which quite a good amount is used in tile installation (wall , floor , Swinning pool etc).

In last few years size of tile used have increased from 2’2’ to much larger size like 84, 4*4 etc.

Tile companies, architect & even masons have started to recommend using adhesive for installation on bigger tile instead of cement. Below brand is mainly used in central india regions as per my knowledge.

https://myklaticrete.com/products/tile-adhesive/

I have 3 queries if I may ask

- Do you have any insights how cement cos are dealing with above trends are they supplying cement as raw material and then adhesives made from them or directly planning to make finish products?

- What % of total cement consumption comes under tile installation

3.Are other product being made like roofon by shree cement (specially for roof slab casting)

Thanks for excellent work on cement industry dynamics @ashwinidamani

2 Likes

hello, i found this link on twitter, it gives some insights on cement industry

P.S. recently started looking into cement industry

hey parth,

A.1 i believe Ultratech has a very good brand recall across nation. As ashwani sir very well elaborated that a laymen cant understand the product well. I feel like a person would prefer brand because high amount of cement is required for house construction.

being a brand which is easily recallable and have a trust of people helps Ultratech charge a little more than peers.

A2 cost/tone consist of freight inwards + it also depends on how deep limestone mine has already been dug + do they have a big plants and few small plants or its like evenly distributed. i feel that it leads to higher costing whereas in shree cement they have one huge plant in rajasthan which makes them really cost effective and area specific. thats why they have high amount of market share which is competitive for ultratech in north region

I dont know about 3rd answer

i have recently started understanding cement industry. i hope this is helpful to you.

White Cement is a very small market. If any new player were to enter, it wont be be to create any outsized profit. The market size prohibits new players from entering.

Cement demand to contract as Covid-19 hurts - Crisil

Covid-19 has cast a long shadow over a much-anticipated mild recovery in Indian economy in fiscal 2021. Along with external factors such as weak global demand, supply disruptions, and global financial shocks, the economy is grappling with lockdown, factory shutdowns, reduced discretionary spending, and delayed capex cycle.

cement-cracks.pdf (1.1 MB)

All this is expected to affect construction, and thereby cement demand.

1 Like

Across various states, there has been an increase of Rs100-250 per cement bag and about Rs2,000-2,500 per tonne of steel

Shree Digvijay posted good results

Hi Ashwini,

First of all thanks for a very informative thread on cement sector. I haven’t tracked this sector in past and don’t have any knowledge.

As discussed earlier with you, and to carry forward the discussion on Shree Digvijay Cement, you have been highlighting risk on their mining reserves - however, the co keeps mentioning about a high number (reserve) and there were rumors about them bagging some additional mining right (though cost maybe higher than before). So what are the concern here? Do they have RM linkage for next few years only or there is no risk for next 5-7 years?

Personally I used to feel its like a simple side-car investment as TrueNorth fund seems to have acquired the company at a real distress valuation from Brazilian company. Based on the numbers of the company and the youtube talk it seems the company was turning around but the earlier promoters lost patience.

I feel a PE fund will only come in if it believes that it can generate good IRRs from investment till selling off of the company.

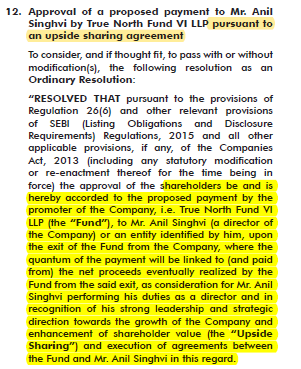

The most interesting thing has been that they have roped in Anil Singhvi who has been a veteran in the cement industry and it was interesting to see that he has been incentivised to generate an high IRR. Extract from AR19:

Recently he was buying aggressively from the open market when the market was melting down in Feb and March. I was surprised to see the action but now one can understand seeing the March qtr nos and the liberal dividend.

Co has generated fantastic cash flow in FY20.

Given Covid, H1FY21 maybe really bad for cement cos. So I’m trying to understand more about ShreeDigvijay and if in coming months if the stock falls sharply, will it be an opportunity? What all should we track here? Can you include Shree Digvijay in your peer comparison and share the key metrics?

Thanks,

Ayush

Disc: Invested along with clients

19 Likes

Shree Digvijay is a case of Good management trying to turn around things.

Couple of things which an analyst can do. Try converting all PL line items into per ton basis.

1.So take Net Sales and divide by per ton produced

2. Divide RM Cost by per ton produced

3. Divide Power Cost by per ton produced

4. Divide Other Expenses by per ton produced

Plot all these numbers over 5-6 qtrs and see where is the profit coming from.

- Is a particular line item contributing to profit

- Are volumes als contributing.

In my view , in Shree Digvijay most of the profits are coming from Sales Price increase. Is it sustainable (after Corona)

Also where will next leg of growth come from. Co is operating at 98-99% capacity.

So they are sitting on peak sales price, peak capacity utlisation.

As far as limestone is concerned, if we do google searches, we can clearly observe that their limestone mines havent been approved since 15 odd years, The one which they might win is also very small and hardly will suffice 2 years.

Now good things are

- Very capable management

- Cost levers can be managed and next set of profit growth will come from there.

Disclosure : Not a registered investment advisor

25 Likes

Cracks loom for cement dealers

CRISIL Research conducted a survey of 100+ dealers across 13 states. Notably, trade channels account for ~60% of total annual sales of cement and are, therefore, a vital indicator of the sector’s condition.

Covid-19 to stretch credit cycle, up working capital needs

Key takeaways from the survey

-

Almost all the dealers foresee 10-30% drop in demand in fiscal 2021 due to delay/freeze in construction activity

-

More than 60% respondents have a minimal inventory of 2-4-days, but spoilage is a concern nonetheless

-

The dealers’ credit cycle is likely to get stretched from 4 weeks to 8 weeks over the next 2-3 quarters

-

Working capital requirement is expected to increase 12-17% in a best case scenario, assuming dealers are able to limit operational expenditure, reduce credit sales and infuse additional capital in their business. A probable risk of retailers defaulting on payment dues will aggravate the financial pain

-

Traders are hoping for manufacturers’ support in terms of better margins (higher incentives)

-

Chances of swift resumption to normalcy post the unlocking look bleak because of delay in return of migrant workers and resumption in freight operations

-

Urban centres are likely to fare worse than rural ones given higher dependence on migrant labourer

Shree Digvijay Cement Reports Strong Q4 Numbers : Anil Singhvi

4 Likes

Hi Ashwini ,

What are thoughts on star cement and if you can throw some light as to why the tax outgo for star cement is so low ?

Thanks

Chirag

1 Like