Market gives value for multiple reason. Dmart is much more valuable than Future retail. That is because of Capital Allocation, Promoter Quality, Focus etc.

Shree Cement is valuable because of absolute focus of Promoters.

No Diversification

Great father Son Duo

Humble and Down to Earth promoters

Hunger for Grwoth - keep trying something (low risk bets) every few years

Not a single instance of Mis-Governance

A Good Balance Sheet which allows headroom for Growth

Basically here you are paying premium for future. Good business + Good promoter will surprise from time to time.

In case of Emami, it was the case of a desperate seller - which was not offering anything great.

In my view, margins are made in Trade, but for that Non Trade has to do well too.

If there is sufficient volume uptick in Non trade (Infra Sector), then bulk of cement gets diverted there and hence gives pricing power to Trade Segment Cement Cos.

@Donald : Cement cannot be stored (gets stoned, takes space etc)

One cant even stop production every now and then…Because if you shut down the kiln once, there is huge cost involved. Infact after shutting down kiln - you have to reheat kiln for two days by burning expensive fuel just to bring the temperature to a level where grinding can again be done.

So shutdowns are taken carefully.

Hence the only option left is to produce and sell above your Variable Cost of Production and hence recover some part of Fixed Costs.

Now when Capacity utilisation goes up beyond the Break Even point. you have the option to either produce or not produce depending upon market situation (you no longer have to worry about Fixed Costs under-recoveries).

This is the time when companies take calculated decisions and decide whether they want to produce more (if market is willing to give higher price)

So if market gives higher price, capacity utilisation goes up - and not the other way round

What do I mean by market willing to give higher price

Basically companies increase the price and check if market is ready to absorb or do buyers vanish

if they dont vanish, then you produce some more, and then take some more hike and then produce more.

Buyers vanish when they feel there is no urgency to build a House or a Bridge or a Dam

Awesome. Abhi bahut time lagega mujhe saare issues smajhne me. This answer of your should go back into the main flow at an appropriate place - why shutdowns dont get taken - and why price rise happens beyond…etc.

I will go back through the thread in detail after a week (my own work) to see what more nuggets I have missed - judging by a quick scan of the Likes - there is huge masala waiting…cant wait…but :(. Also I plan to create a Cement Primer including Key Trackables/Key Thresholds - as a starting point for new guys like me to start following the various companies. (Otherwise mere dimag mein baittha nahi hain) Have taken @jitenp inputs for same, will refine with him again after next week, and also check if you have additional inputs to offer.

A style we follow which has come in handy for us every time. We learn from one expert and use that small knowledge to quiz the next expert better…by the time we have spoken to 5 experts and captured that back in a Primer/Template, we mostly have working knowledge on the main issues/variables/key monitorables in the business. Then of course is upto individual interest and diligence to use this theoretical knowledge practically over current market opportunities.

Thanks again for being so generous with your time and diligently answering earnest questions from us. You should have a huge fan following at VP, and may God bless you to keep having the space and the time and the generosity, always!

Dear Ashwini, what does Absolute EBITDA mean? How is this calculated?

Also, the concept of looking at cost per ton or EBITDA per ton is appealing. The low cost producers or better still, the companies with high profit per ton can survive cycles better. These metrics indicate cost efficiency (and EBITDA per ton incorporates sales into that as well).

Do you think adding a layer of investment efficiency / capex efficiency will add further teeth to an analysis? For e.g. typical cement capacity addition costs ~US$ 100-120 per ton. If a company is able to add capacity at, say, US$ 50 per ton, will that offer a structural advantage, just like cost efficiency does? If the capex costs only US$ 50 per ton, then even an EBITDA/ton of, say INR 600-800 could result in better return efficiencies.

My current view is to use capex efficiency also as an evaluation factor - and perhaps could make it to the framework @Donald talks about. Will be good to know your thoughts!

Some data from screener for quick historical comparison of the companies in the cement industry. PT Chart is the worksheet to refer to. Also, it has two graphs for absolute and % based parameters for comparison, so scroll down. Use the slicers on the right of the graph to get to the data parameters you are looking for. The worksheet is sized for a 27 in. monitor, you may need to resize or zoom out for complete view.

there is good article at Kanvic Consulting please find below it is for vision 2030 However it is outdated but capture good points about indian cement industry future out look where they are focusing the major demand will come from infrastructure so in that case govt budget allocation for the infrastructure will have a huge impact. Future of Cement Industry in India : Vision 2030 | Kanvic Consulting it is emphasised by honrable PM https://twitter.com/i/status/1225377912062300162 but infrastructure is very wide scope .

Cement is basically a commodity and like all commodities, the rule is…Be prepared for sudden cyclical downturns.

Like all cyclicals Fixed Costs remains high in Cement also

Like all cyclicals Price is not in control of seller

The traits one should look at therefore is - What is the company doing to protect itself from downturn

Is it low on Debt, so that when cycle is bad, interest cost doesnt kill it

Is it ensuring lower cost of production and capability (not capacity) increase

One needs to judge what is the source of EBITDA for Cement player.

Is it Higher pricing which leads to EBITDA increase or is it better cost control.

Always assume the worst possible Sales Price for Cement and then calculate what EBITDA will the company make. If it can sustain worst possible times, then you have a winner in hands.

Price trend for gray cement per 50 kg bag across regions:

DATE

PRICE (AVG)

CHANGE

EAST

CHANGE2

WEST

CHANGE3

NORTH

CHANGE4

SOUTH

CHANGE5

CENTRAL

CHANGE6

Apr-18

326

336

309

300

326

317

May-18

331

5

336

0

323

14

296

(4)

331

5

314

(3)

Jun-18

328

(3)

336

0

319

(4)

296

0

328

(3)

319

5

Jul-18

332

4

342

6

321

2

309

13

332

4

338

19

Aug-18

330

(2)

345

3

314

(7)

302

(7)

330

(2)

325

(13)

Sep-18

325

(5)

334

(11)

308

(6)

304

2

325

(5)

322

(3)

Oct-18

324

(1)

329

(5)

310

2

301

(3)

324

(1)

325

3

Nov-18

320

(4)

331

2

302

(8)

303

2

320

(4)

323

(2)

Dec-18

319

(1)

331

0

304

2

301

(2)

315

(5)

322

(1)

Jan-19

321

2

331

0

304

0

306

5

310

(5)

335

13

Feb-19

335

14

331

0

314

10

306

0

360

50

340

5

Mar-19

342

7

331

0

319

5

309

3

385

25

340

0

Apr-19

361

19

350

19

339

20

340

31

375

(10)

375

35

May-19

372

11

360

10

355

16

365

25

370

(5)

385

10

Jun-19

362

(10)

345

(15)

345

(10)

360

(5)

360

(10)

375

(10)

Jul-19

352

(10)

330

(15)

337

(8)

355

(5)

335

(25)

375

0

Aug-19

340

(12)

320

(10)

329

(8)

345

(10)

305

(30)

369

(6)

Sep-19

338

(2)

310

(10)

325

(4)

335

(10)

325

20

366

(3)

Oct-19

337

(1)

315

5

325

0

335

0

315

(10)

366

0

Nov-19

334

(3)

312

(3)

325

0

338

3

305

(10)

360

(6)

Dec-19

323

(11)

302

(10)

305

(20)

338

0

285

(20)

355

(5)

Jan-20

340

17

312

10

320

15

358

20

315

30

365

10

Feb-20

349

9

320

8

332

12

358

0

335

20

370

5

The most interesting case to me so far is the central region. Price has been the highest since April 2019 and was maintained. The average price for the year so far is 370 per bag which trumps the 2019 average of all regions.

There is no significant capex coming up in this region.

Just read on True North’s website which had acquired Digvijay Cement last year that it has 13MT of limestone capacity. Is there any reason it would not be shown as an Intangible Asset in Balance Sheet of this company or any other? https://truenorth.co.in/current-business-cement.html

@Donald

A recent report by Nirmal Bang highlights a few points that I found useful :

They analysed for cos which have been out performers in Cement Space in last 10 years

Shree Cement - 27% CAGR over 10 years

Ultratech - 26% CAGR over 10 years

JK Cement - 24% CAGR over 10 years

Ramco Cement - 21% CAGR over 10 years

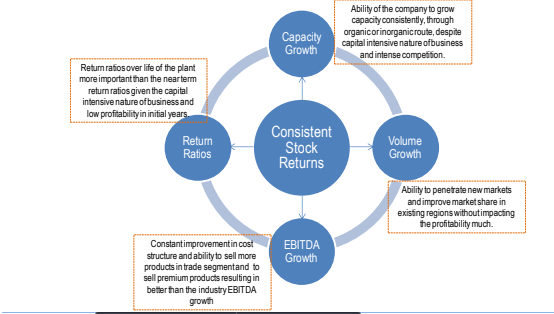

What the study claims is that consistent performers depicted following traits

Capacity

Cement being a capital intensive business, very few companies have been able to add capacities consistently without impacting the balance sheet.

While India has abundant reserves of limestone, key limestone bearing belts called clusters generally houses the majority of cement plants in the country. There are seven such clusters in India viz. Chanderiya (Rajasthan), Satna (Madhya Pradesh), Chandrapur (Maharashtra), Bilaspur (Chhattisgarh), Gulbarga (Karnataka), Yerraguntala (Andhra Pradesh) and Nalagonda (Andhra Pradesh). Despite the abundance of the mineral, key limestone bearing lands/mines are already being taken up by the incumbent players. Sourcing of new mines and erecting a cement plant on greenfield basis has become increasingly difficult and time

consuming

Therefore companies which have historically done well have had the vision to identify

and develop new sites for cement plants and execute their capex plan well without compromising on Balance Sheet.

Since higher capex leads to higher interest and depreciation cost, if the commissioning of the plant coincides with weak demand or pricing scenario, the payback period as well as profitability from the new operations gets delayed

Volume Growth

While building a cement plant comes with its own set of challenges, selling the manufactured cement in the market has its own obstacles

Cement demand in India has grown at a CAGR of ~6% over the past decade. This compared to growth in supply at a CAGR of 7.4% over the same period means supply has outstripped demand. Hence, achieving higher volume growth, we believe, is more challenging given the intense competition, especially in a new region where the company has to set up the entire distribution network from scratch.

The first two points indicate that Outperformers should have

(1) balance sheet strength to incur capex on a consistentbasis

(2) comfortable utilization levels which can support higher-than-industry volume growth - A well Oiled Sales Machinery

EBITDA Improvement

EBITDA is a function of volume as well as the cost structure and pricing in the markets it is operating based on the demand-supply scenario

There are multiple variables that affect EBITDA of a cement company. These are volume, pricing and costs.

Volume is a function of the ability of the company to push volume in the market profitably, costs are driven by efficiency and commodity prices.

Efficiency is driven by the company itself, adding capabilities to produce at lower cost. Long term Investment in Waste Heat Recovery, Wagon Tippler, Storage Areas etc

Ratios

Debt Equity Ratio becomes an important Ratio in Cement (just like in any Commodity Cos)

At a Debt of 1500 EBITDA/Ton, it becomes unsustainable to run a Cement Plant.

Fully agree Dhiraj. Cement is entering into treacherous times.

almost 1 month of lockdown, then lack of labour and Raw Material and most importantly demand, and then the onset of monsoons.

Also need to factor in the sales prices will fall, and hence profitability will be hit.

It looks like there will be bad time for 4-6 months atleast.

It will be important to focus on companies with lower debt/ton so that companies dont end up getting into a debt cycle.

Highly leveraged companies in cement space will have a seriously bad time. Cement is Fixed Cost heavy

Dont focus on stocks which are trading at low per ton valuations. Look if they can survive without selling assets.

For eg a KCP may survive because of sale of other non core assets, but a Dalmia could have trouble for some more time.

MNC cement cos will survive given their robust Balance Sheet strength, but their cost cutting measures will not be nimble.

We will need quick thinker and jugaad mentality right now.

Costs of petcoke, a major input for cement and diesel, used for transportation of cement, will be lower given sharp fall in international crude oil prices. Lower raw material and freight costs may lower the cost of production by Rs 100-200 per tonne.

@ashwinidamani

I have gone through Dalmia Bharat Cement, now the fy20 TTM sales is equal to market Cap. it is quite impressive. South india is dominant market for Dalmia cement . Capacity addition o FY21 and 22. I need your guidelines …How do i approach cement stocks . Please guide

@ashwinidamani First of all thank you for such enlightening posts. It enabled me to learn much more about cement industry in detail.

I have one question. I think the presence of moisture is the main reason for deterioration, but nonetheless with life of cement not more than 3 months, present lockdown and untimely rains in many parts of the country, what do you think will happen to the already finished inventory ? Will it become completely obsolete ?

Another strategy can be to not grow at all during economic downcycles. Instead use profits to decrease debt, improve operations, perhaps debottleneck existing capacities. Later go on and acquire smaller companies (which might have already done the expansion work only for smart companies to come and takeover).

So as long as ur godowns are not full u can keep producing and storing cement.

Now Check how much inventory a typical Cement manufacturer has of Finished Goods. Not more than 20-30 days. That would be the sort of average inventory he stores. May be he has spare capacity for 1 month extra.

Cement which catches moisture is also sold, but at less than cost of production (stoned cement). Some guy need it for barricading, concretisation etc.

Yes plants can use this time to do maintenance and de-bottlenecking.