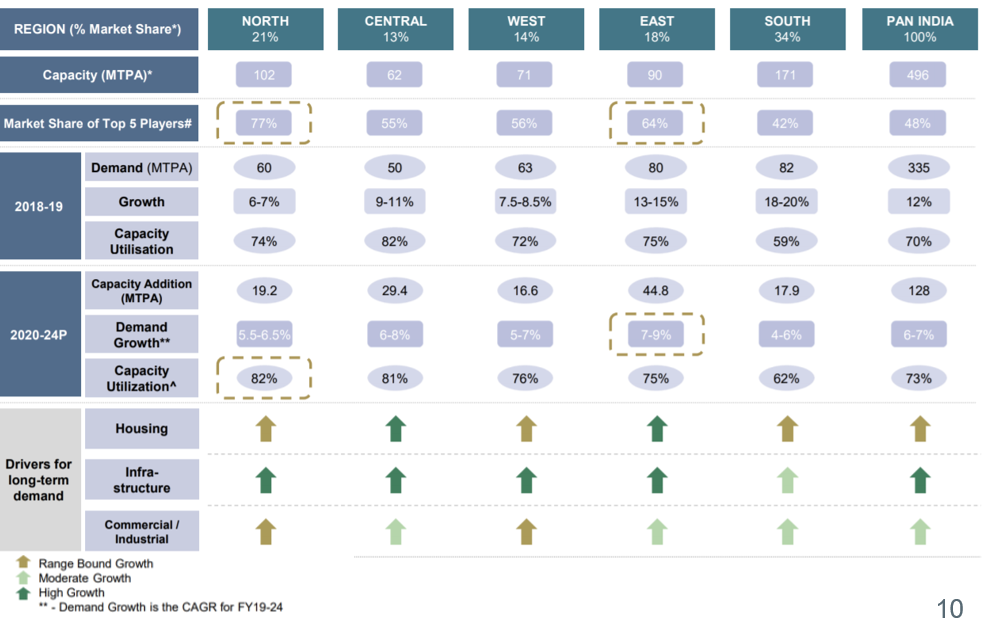

Got this from Shree Cement’s Investors’ presentation and found it useful in understanding the region wise demand-supply dynamics. Will be glad be know views.

Regards

Got this from Shree Cement’s Investors’ presentation and found it useful in understanding the region wise demand-supply dynamics. Will be glad be know views.

Regards

Find enclosed my working on calculation of ACC return since listing. It may provide good insight of growth over the years and wealth creation by the company.

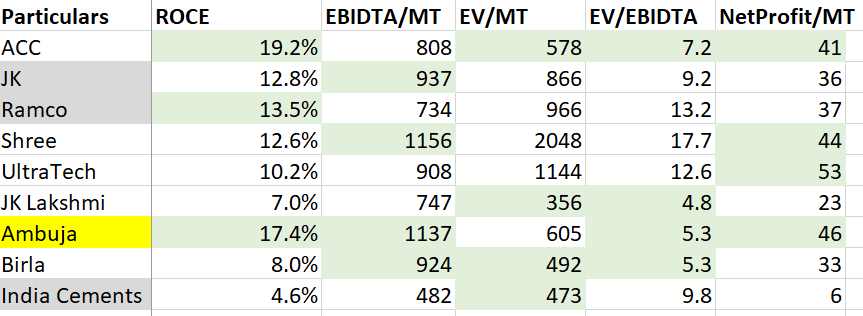

Just going by pure metrics, Ambuja looks best of the lot. It is Pan-India operator, with strong presence in North and West. Next few years can be interesting.

Disc: Not invested in any stocks discussed

Regards

SJ

Hi Ashwini,

Star cement in the annual report has repeatedly mentioned proximity to Limestone quarries as a key component of their margins. Considering the positive outlook for Rural demand in the east, is this enough of a Moat for a small player like Star?

Or can biggies like Shree, Ultra tech simply reduce prices to dilute the margins of Star

Shree Digvijay FY20 Annual Report key takeaways:

Declared dividend 15% after 33 Years.

Reduced debt 40 Cr and now the company is debt free along with a cash balance of 70 Cr.

We were also impacted, our operations were closed from 25th March, 2020, as per the lock down directives.

The growth was recorded mainly due to higher market realisation, raw material cost optimization, reduction in overall fuel cost and sustainable plant operations.

The Capital investment on energy conservation equipment is 10.97 Cr.

EBITDA / Ton increased to 1049 from 296 in FY19.

EV / EBITDA stands at 2.18 times.

Cement industry is highly energy intensive and 29% of its total expenditure consists of power and fuel costs.

hello sir,

could you please specify, this data is of which year?

For JK, Ramco and India Cements March results were not out so TTM (Dec 19) and for the others its TTM (March 20).

Regards

Shobhit Jaju

The prices seem to be holding up in June, but that can be attributed to lack of supply due to lockdown. They seem to suggest a 10-12% impact on demand for FY21. I think it will take another quarter atleast to get a better sense of pricing and demand situation for FY21. Link to report: PL Cement June 2020

Regards

SJ

Shree Digvijay Cement at current price of Rs.58 is trading at Mcap of 815 Cr. It has debt free BS and 74 Cr of Cash & Cash equivalents. Hence, at EV of 741 Cr its trading at $91, almost at replacement cost.

1.07 Million tons capacity trading almost at replacement cost with BS size of only 400 Cr.

For FY20 its EBITDA/ton of 1027 which is gold standard in the industry and limestone lease already an overhang, I feel stock is extremely overpriced especially when you have larger players with growth visibility trading much cheaper!

Other views welcomed

Disclosure: Not invested

Has anyone attended Shree Digvijay AGM today and can post the takeaways?

Would be very-2 helpful.

Thanks & Regards

SOME LATEST REPORTS ON CEMENT SECTOR

Hi Aashav, the $91 dollar calculation isn’t absolutely correct. The company will incur a CapEx to increase it’s capacity by 75% to 100% in a year or two funded mostly via internal accruals.

Also, recently the company has announced that they have incorporated a subsidiary Digvijay Logistics, which means that they will soon get the license to operate the Jetty that they have to handle third party logistics and will also help them import coal and other raw materials which will aid the margin.

Above mentioned plans will change the valuation of the company especially for a strategic buyer. Also now since a couple of quarter they are able to maintain an EBITDA of Rs.1100+ per tonnes which is exceptionally for such a small plant.

Considering this I think there is still an upside of 75% to 100% from the current market price of 47.

Disclosure: Invested.

Hello, where have the co. officially informed about the CAPEX? I am not aware of any communications from their end.

Any meaningful capex for a cement co. would be 1 Mn ton and that would cost around 500-700 Cr. But co. has around 75 Cr of cash & equivalents. How can they fund entire capex from internal accruals?

Hi Aashav, the chairperson of the company had communicated that in the annual general meeting.

As you rightly mentioned that even a million tonne plant would take about 750 crores but he company has basic infrastructure ready in place, they will not need to shell out the entire 750 crores.

The chairperson said that they would not shy to take debt to incur the CapEx but largely the requirement will be met by internal accruals.

Disclosure: Invested.

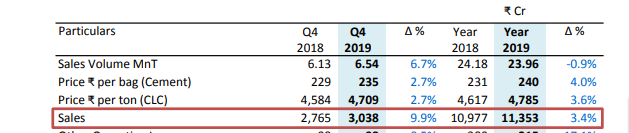

I was going through the recent quarterly results of Ambuja Cement but couldn’t figure out how did they arrived at the net sales value with the realization & sales volume. The sales value is not equivalent to the product of realization & sales volume

Can anyone help me figure out how is the above sales value derived from realization & sales volume

For Shree Digvijay cement : Why ESOP is at Rs 16. What is rationale behind pricing ESOP.f39fe2b4-d157-4889-a5d6-289be32aa372.pdf (550.2 KB)

Cement stocks can be a favorable if one can play cyclical rightly. Given the government’s focus on infrastructure spending and affordable housing, the

cement sector’s long-term growth potential continues to remain healthy. Demand revival is imminent, especially during the festive season and the January-March peak construction period.

The second quarter is traditionally a weak one for the cement sector, with lower demand as construction activity slows down on account of the monsoons.

Demand was low during July and August 2022, showing some sign of revival in September, 2022. Pick-up in retail demand was on the back of pent-up demand accumulation during the monsoons, pre-Diwali construction and repair work gaining momentum, and pre-election tailwinds. Institutional demand was led by increased construction activity after the receding monsoons.

Any downside post Q2 can be taken as calculative opportunity if correction is solely due to lower Q2 demand.

Link to You Tube Video - Cement Sector Deep Dive! Industry analysis, EBIDTA/ton driver (most imp metric), Top 4 cos evolution - YouTube (Cement Sector Teach-In)

Hi, This is Harshit Toshniwal here. I was working as equity investment analyst for last 7 years, with Premji Invest, Jefferies and ICICI Securities.

Building sector knowledge has a long shelf life as investor, and with that belief, I have taken some time for myself to dedicate it on developing wider understanding across more sectors/stocks. While I build my own understanding, I am also motivated to put up sector teaching videos alongside.

I am starting with cement sector analysis. It is a long video, but covers in depth on -

• Overview of demand drivers and manufacturing process

• Regional demand-supply dynamics of cement

• Variables that drive IRR of cement capacity expansion

• Deep dive into the most important metric, “EBIDTA per ton” - Understanding its sensitivity

• Evolution and analysis of top 4 players (Ultratech, Shree, ACC & Ambuja), How Adani’s entry impacts sector?

• What is the crucial metric to track, that drives stock prices.

Link to You Tube Video - Cement Sector Deep Dive! Industry analysis, EBIDTA/ton driver (most imp metric), Top 4 cos evolution - YouTube

Feel free to share it with anyone you might think it can be of use. Looking forward to your responses and feedback for improvement.