Shifting the presentation here from Experience Sharing for better & more focused feedback/inputs/criticisms on it.

Investment Journey.pptx (102.2 KB)

Best

Bheeshma

Shifting the presentation here from Experience Sharing for better & more focused feedback/inputs/criticisms on it.

Investment Journey.pptx (102.2 KB)

Best

Bheeshma

Excellent presentation and considering you are in to investing from March 2015 only gives a big hope for me.

Thank you Bheeshma

Its never too late or too early to start. I wish i had started in my 20s. I guess some things happen when they are supposed to. My take is that i will have to work that much harder now to make up for the lost time and learn vicariously more from others

Very nice presentation Bheeshma. I have followed your posts with interest - the quantum growth in your investment skills has been phenomenal. I haven’t been much into Technicals but I am coming around to a realisation that it serves it purpose.

My only quibble with your post would be:

In all cases – I sell if prices decrease by 15% from my purchase price ( and I re-evaluate buying thesis )

15% is too low a floor. If you have convinction, you should be willing to settle for a lot more.

Bheeshma,

Excellent presentation. For some one starting investing just two years back, it is amazing to see that you have already developed your own style and thought process. Very impressive.

Just curious - are you a full time investor? The reason to ask this question - it takes significant amount of time to develop a level of maturity. When I see your posts across threads they don’t appear from some one who has been in the business only for 2 years!

Wow such rapid strides. How did you manage that in 2 years. I have been trying for 3 years but still it’s so difficult for me

I tend to buy stocks when they come out of strong base patterns even if i am convinced about the long term business prospects. After all long term is a chain of short terms and i could be just plain wrong about the whole company.

A > than 15% downmove in a stock price indicates to me that i was wrong about the base and now is not the time to enter the stock & it will be available cheaper at a later date. These things i have repeatedly experienced and 15% is somewhat of a mental trigger that goes off in my head.

However, I do agree with you that there are some gifted investors whose thesis for buying a company is so sound & correct that they dont need to worry about notions like base patterns and the like. Unfortunately, i am not one of them

Best

Bheeshma

Sir great presentation and u have a very unique way of investing ,I am very impressed and amazed by how fast u acquired these skills

How much annual return did u get from this investing model

Hi @newrb

No i am not a full time investor. I have a salaried 9 to 6 job. However if you read peter lynch and pat dorsey a couple of times you can quickly become good. I also like to read Prof Sanjay Bakshis blog repeatedly. His article the Vantage Point is a piece of art. Rakesh Jhujhunwala is also liberal with his knowledge and i make it a point to read & listen to everything on him and by him.

On VP - I read all the posts without fail esp when people with a good track record are making them. The little things they say in their posts are often the most important. Lately i have been reading @dd1474 posts on the care thread

Overall, my learning curve has been steep after joining VP.

Best

Bheeshma

Bheeshma:

It would be helpful if VP Goa team could give a sense on their Age and time in investing (full or partime) and it is a key determinant to understand the evolution of their investment style.

Pls ignore if not relevant.

R

Samir

Very Nice Presentation Bheeshma. Your sell logic- whenever stock price moves below 15% of buying price is good idea.

Non ignorables - is important. In stock market, what should not be done is more important to avoid major losses.

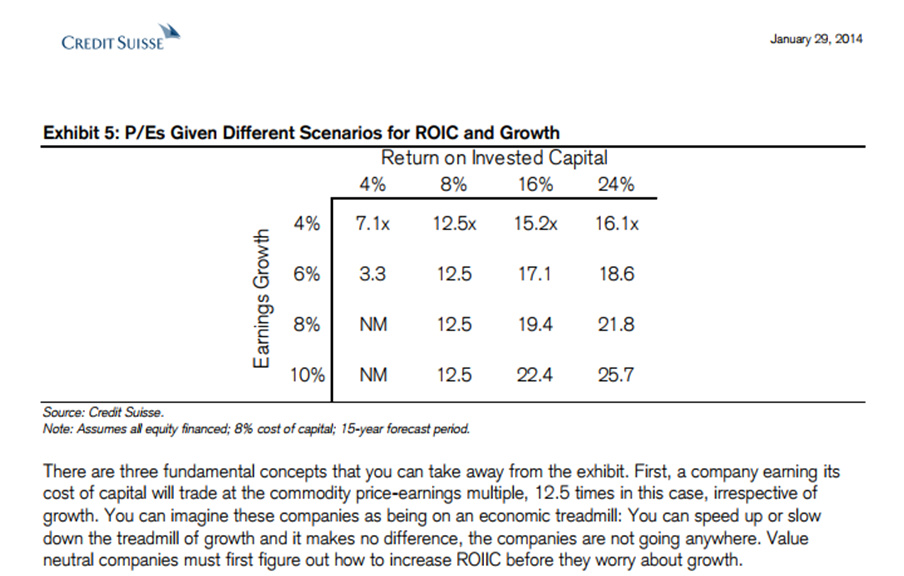

Sharing a new learning for me - credit to M.Mauboussin. The irrelevance of growth if the company doesn’t earn a return on capital exceeding its cost for the same. I have observed people getting excited (me being a prime example) with earnings growth, However, growth adds value ONLY if it earns more than its cost. I am now more cautious about earnings growth and as a result more probing about its roots. Its certainly an important realization for me and reading Mauboussin has been a meaningful stepping stone in the right direction.

Best

Bheeshma

Hi

True! I have tried and used this for sometime now.

Valuation Formulas.pdf (172.4 KB)

Had made notes on this. Sharing.

p.s. do look at his tweets he has shared a photo of his ‘Valuation Shelf’ of his books. ![]()

Regards

Deepak

Hi Deepak

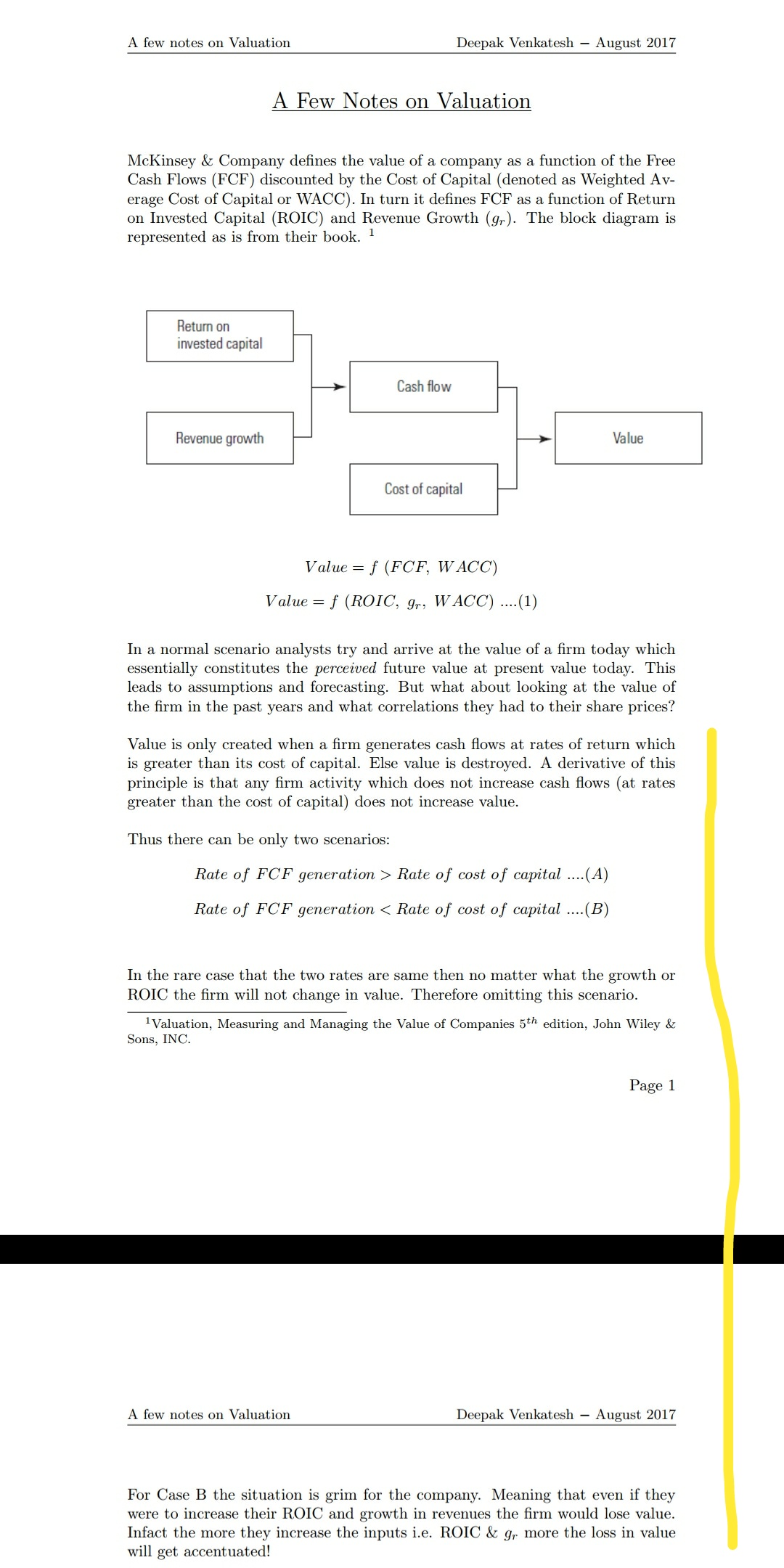

Your notes are very well written and carefully expressed capturing the essentials. I especially liked the part where you have written that value is much more sensitive to positive changes in the ROC than growth. This presents many opportunities as one doesnt track ROC with the same fervor as one tracks growth in earnings or sales - leading to ignored companies that have good ROCs but growth has stagnated for one reason or the other. These companies are often available at reasonable valuations even in a bull market and valuations seem to display immunity from the vagaries of the marketplace despite lack of growth.

Your notes are well worth the read. Thanks for sharing them.

Best

Bheeshma

The Credit Suisse guys have got some really smart people with very actionable advice.

I had found a very interesting report on Moats back in 2015. Here is the updated version of the same.

Take a look at this guys.

Measuring the Moat [2016 updated]

Hi @ciri

Mr Mauboussins thoughts on many things have been very useful. The most important takeaway for me however has been his thoughts on identifying market expectations. Al rappaport his guide is also excellent. Expectations Investing - thr book co-authored by them is a very good read.

Mr Mauboussin uses his expectations investing framework to measure the moat of a co. From his works, i gather that the stock price of a co reverts to its long term earnings growth. If a co is successfull in creating a competitive advantage and then strenghtening it - then the stock price reflects it. The implied growth rate in the stock price is his quantitative measure of a moat is what his study says.

For several years HUL was trading at its implied growth rate of 10%. Recently, however the implied growth rate has improved significantly and it has so far sustained. Maybe a moat has been strenghtened there.

Hi all,

As i have invested i have learnt along the way. Some of my earlier investments were in cos which despite posting good numbers and good return ratios drifted down in terms of stock price and as a result i lost money. Some of such notable cos were Shankara, Tiger Logistics etc

Anyways, painful memories aside , i realized that one way to differentiate cos is look at how they manage working capital. More specifically, is the cash from operations (before working capital changes) enough to cover working capital needs?

While this may sound obvious , i think that any method that helps to separate cos that one should avoid deserves special attention

Money locked away in working capital needs to be funded and i have began to appreciate the impact this plays on the overall valuations of a business.

If you find yourself invested in such a co then there is only one way its going to end.

Looking at the working capital cycle and estimating working capital needs of a business is as fundamental as it gets. I have looked at the operating cycles of many businesses now and its quite revealing in terms of giving a sense of how difficult or easy the business is to run & operate.

So i am sharing a sheet that helps one to estimate working capital needs and relate it to the operating cash flow ( before WC changes ). Cos like Shankara , Tiger Logistics and countless others just cant generate enough. Ambika Cotton for e.g even in tough times has generated enough to be able to chug along while Indocount is not able to. Dmart and Future retail same story.

Vmart for long ( that is the co analyzed in the sheet attached ), was not able to generate enough.

However, it improved its cycle drastically and in 2017-2018 with an operating cycle of 55 days, it made enough cash to be able to cover its working capital and turned debt free.

| VMART | Mar-08 | Mar-09 | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| WC Days | 123 | 115 | 140 | 103 | 93 | 87 | 79 | 75 | 67 | 55 | 55 |

OC.xlsx (13.5 KB)

The cells marked in blue you will have to copy paste data from screener or any other source.

Items I and J are the numbers to look at. I is the WC required and J is Operating Cash flow ( before WC changes). The actual WC capital required by a business cant be picked from the balance sheet as the receivables contain a profit component and for cos with significant gross margins, the WC is overstated if picked directly from the balance sheet. It has to be estimated

Do let me know your views on the same. Any inputs appreciated

Best

Bheeshma

@bheeshma

I have read few of your post. Remember 1 post in dmart. You go deep into inventory turnover, working capital, usage of debt etc which is no doubt great, but I am not yet competent enough to understand or comment. I restrict myself to P&L, Yearly, quarterly, PE, 52 week low/high, RoCE, RoE and of course cyclicity, future road map, tailwind if any, competition etc… The qualitative part.

Therefore, I would not comment on your current post, rather would like to know more on your logic of selling when 15%down from buy price. Refer your presentation. This is indeed very surprising… If you buy quality growing companies, one should average down rather than selling isn’t it? 15 % is just too close. Also I prefer trailing stop loss of 20-30% for low conviction bets only. Ex Maruti if falls, I will average down. But let’s say yes bank falls by 20% from High, I exit.

Would like to have your views on this. Thanks.

Hi @homemaker

Welcome to Valuepickr

The logic of 15% is based on my average buy price. I average down 2 or 3 times for cos where I have a good feel about and where I am sure about the true worth. If after that the co still drops I feel that the market knows something I don’t and I get rid of the position without applying too much brain.

Since I have a concentrated portfolio and invest in growth cos I run the risk of denting my portfolio if I have incorrectly become more optimistic than necessary. When you are investing in cos where most of the value is going to come from future growth and actual growth is below your expectations the value of your share drops dramatically.

I also like to have specific rules and let these take the decisions for me. When it comes to my portfolio i like to have quantitative rules. That’s why i like the Ben Graham style, he had specific rules.

I am a believer in the efficient market theory and over a long period the price reflects things that you may not know but others do. I am comfortable with 50% falls provided I am willing to average down after assessing no loss in earning power and the price stays less than 15% below my average buy price.

Best

Bheeshma

Exactly. I was partially thinking along the same lines. While I enthusiastically set out in October to build my portfolio, I thought I will do it once and run it in auto pilot. But I think portfolio building itself takes time may be 12 months. Even after averaging down 2—3 times, still the price falls by 15%, is a clear sign market is telling I am wrong. Please exit.

Also by exiting, not only we preserve capital but gives flexibility to look for better options.

Averaging down is like giving your conviction a few more chances and time. It can’t go on for ever and hope based.

Let me thank you, for reinforcing the vague concept which was honestly irritating me for quite some time