Hey

My point of using Walmart was to showcase historically that people paid up in excess in past for a business and then we had statements like 'If you had invested in Walmart 100 shares druing IPO you would have…" you can complete the rest . In other cases we thanked the stars we didnt invest in some solar business etc.

I am using it as an example and not comparing businesses.

Anyways.

Some of the inferences on the numbers you have made are misplaced.

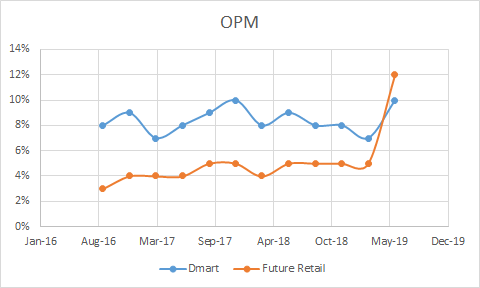

OPM:

Dmart has one of the best operating margins. Infact it has better margins than Walmart has ever had (not that we are comparing here). Walmart since IPO has never touched 8% I believe.

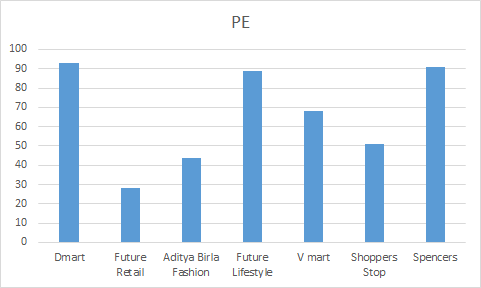

PE:

Not sure how have you calculated 110 PE. Screener says 93.xx. Not that 90 vs 110 has anything a lot different.

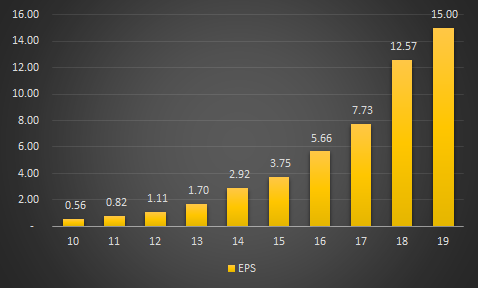

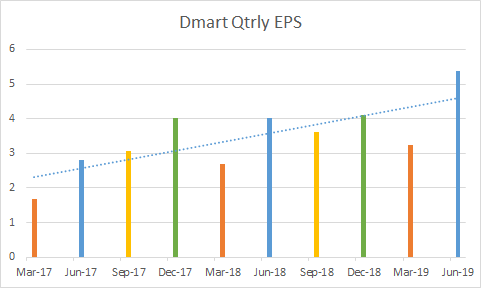

EPS:

Negative growth? There is not one quarter in the last one year in which EPS is lower than the quarter of the previous year’s.

FCF:

I see positive cash flows for Dmart in my calculations. I use the following formula

FCF = NOPLAT *(1- (NOPLAT Growth/ROIC))

More here VP CHINTAN BAITHAK GOA 2017 : Bheeshma Sanghani : INVESTMENT JOURNEY/PHILOSOPHY - #13 by deevee

Aside its negative for Future Retail for instance.

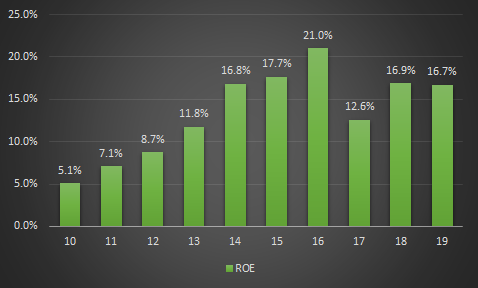

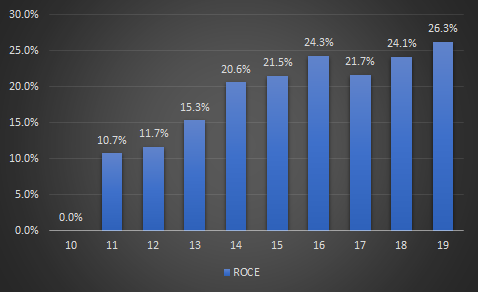

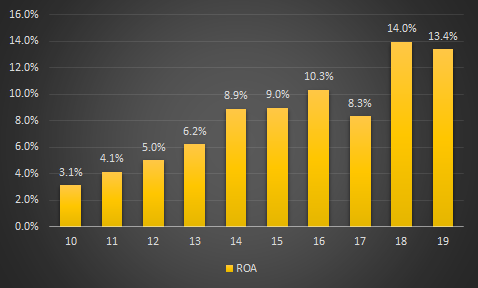

ROE ROCE ROA:

They seem quite appreciable infact.

Aside competition in India is not consistent on these metrics. Walmart though not comparable had 15 years of over 30% ROE. Also they had like over 30% ROE in their initial years.

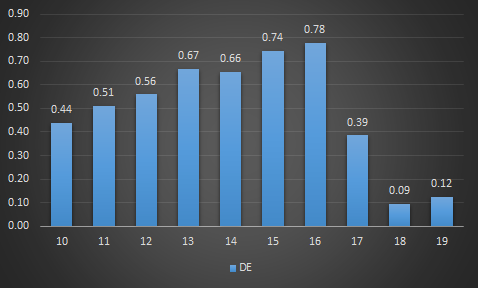

Debt:

Dmart is good here too. A Future Retail has 0.7 DE.

Rgds