Hi…currently Ashish Kacholia invested in Rainbow Child hospitals. You had gone through it during IPO period. It would be nice to know your current views on Rainbow from long term perspectives of 5 years

Rainbow seems a decent bet on specialized children healthcare under a first gen technocrat doctor who worked abroad in such facilities & has established the same primarily in souther india.

Scuttlebutt on hospital & doctor was very good from Hyderabad based network.

Shud give good returns over 5 year period.

1 Like

Assumption seems quite valid refurbished by recent BSE release on robust growth in business which is enclosed.

An asset light high ROCE CAGR business with big mkt share hence some moat . No wonder big FII CAPITAL bought in big 28% stake of anchor quota.

DREAM FOLKS BUSINESS UPDATE OCT 22.pdf (469.5 KB)

Dreamfolks_Anchor_SE_Intimation_Letter-COs.pdf (334.6 KB)

.

2 Likes

1 Like

Vivek sir, would be interesting to know the current composition of your PF. Which stocks/sectors have high allocation and in which sectors do you see opportunities?

2 Likes

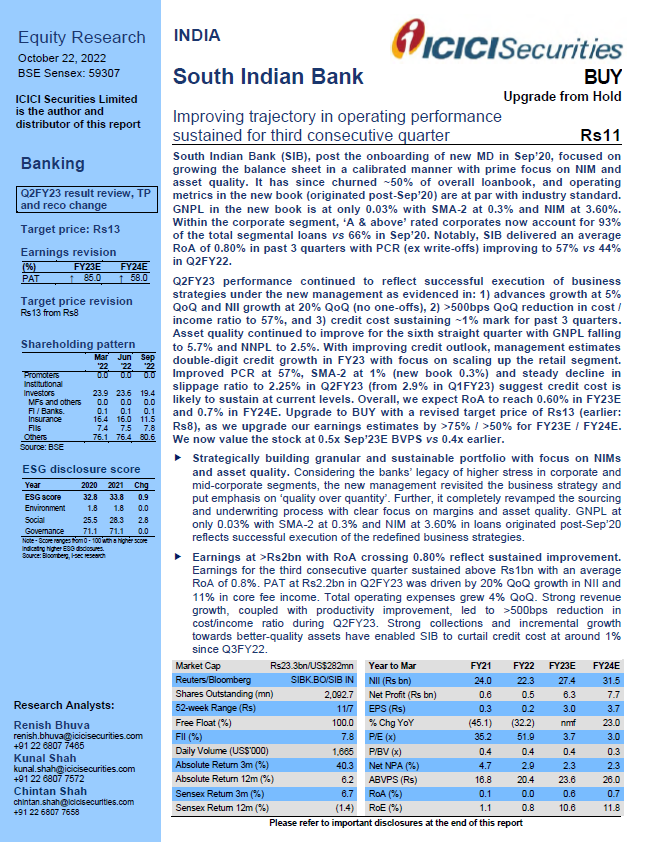

South Indian Bank remains one of the cheaper banks still available much below BV of RS 28 . A beautiful turnaround by MD Murali Sir IIM & Ex ICICI BANK

Casa at 34%

New book of 34000 with 0.03% gnpa.

Pcr at 72.79%

Reducing trend of gnpa and npa.

Bv at 0.50

Trading at less than 5 times.

Zero slippage for new book.

Management pedigree is excellent.

discl Invested

9 Likes

https://twitter.com/CNBCTV18News/status/1602178463992905728?s=08

SI BANK & KARANATAKA BANK ON TEAR. Good interviews with both their MDs

Both hv risen nicely.

discl- invested in both

6 Likes

Hi @Vivek_6954 , Did you assess the IPO for Uni parts? Did you find it interesting enough to invest as a part of post listing price moderation? Thanks in advance!

yes I liked Unipart ipo… Applied and holding the same. valn ok ROCE good n promoter quality too seems good

2 Likes

What’s your assessment on overall business growth this year?

Whatever we have done in the last one and half years is starting to bear fruits and if you see our results of Q4 last year and Q1 and Q2 of this year. We are consistently growing our loan book. We’ve been also improving our net income margins (NIM) and liability have been doing well. Also, our current account savings accounts (CASA) has improved. So, overall it has been a satisfactory year till now. I guess the trajectory will continue.

Any targets for credit and deposit growth?

I am expecting the asset growth to be around 10-12 percent double-digit growth compared to 4 percent growth we registered in March 2022. For CASA, we would want around 34-35 percent compared to 35 percent growth in our Q2 results. Given the tight liquidity situation and the fact that CASA and deposit growth has been little muted for the banking system as a whole,

I would be happy to end the next quarter with 34-35 percent growth and end the year with 36 percent growth.

Where do you want to see NIMs by end of year?

As far as NIM (net interest margin) is concerned, currently we are at 2.98 percent which has grown from 2.6 percent and I would want to end the year at 3.2 percent. Currently, our net non-performing asset (NNPA) is about 2.6 percent as of Q2 end. I would like to be as close to 2 percent by March 2023.

Provision coverage ratio (PCR) including write-offs currently we are at about 72 percent and I would want to be at 75 percent by March 2023. And excluding write offs, I am at about 57 percent and would want to be at around 62 percent by March 2023.

SIB has been attempting to morph into a pan India bank…

Right from the time I had taken charge of this bank, I never had Kerala as my market. We’ve got nine out of 18 regions based out of Kerala and three from Tamil Nadu and we are well entranced in southern India. Equally we are well represented in the north also. We have regional offices in Gujarat, Maharashtra, Delhi, Kolkata, Andhra Pradesh, Telangana, Tamil Nadu, Kerala and other places. I am well presented across the country with dense branches in the southern part of India.

My simple rule is quality is what I am chasing. If I get quality transactions across the country, place doesn’t really matter. So I am looking for good quality onboarding of asset cases and wherever it comes from, we’ll be happy to onboard there.

South has been a stronghold for SIB for years…

In our journey of diversifying our portfolio, the south is growing quite well for us and the rest of India and Kerala is growing well for us.

You must look at Kerala with the context that the state went through successful years of flood and was hit by the pandemic, like the rest of the country. The state is predominantly small and medium enterprises (SME) so these continuous mishaps have put the condition of some of the business models into question, and we are cautiously growing our books in Kerala and the rest of the country more so in Kerala as we look at the state’s recent past.

Is the worst of NPA is behind us?

When I took over as the MD and CEO of South Indian Bank, I had two issues in hand; clean-up the legacy books either by going in for recovery or update or settlement and bring down the gross non-performing assets (GNPA) and continuously improve the PCR.

The other side is to grow the overall book by onboarding quality assets. So these are the two main objectives in different tracks and I am happy to say that in both these tracks we have made substantial progress.

As far as cleaning up the legacy book is concerned, I’ve almost churned 50-55 percent of my total asset book with new sourcing or existing good quality cases continuing to avail limit from us and that journey will continue. We will continue to churn the book with good quality cases and that has already started showing in my new provisioning being substantially lower than provisioning I generally used to provide in every quarter. So, as of Q2 end, I have added Rs 33,000 crore of new book and my delinquency was very low, GNPA was 0.2 percent.

What is the outlook on asset quality?

Of course it is too early to talk with certainty that our portfolio will continue to hold that high quality but, in my experience, if something goes wrong, it will show up. I am pretty confident that my new book will show good results and I will continue to churn out my old books with more and more upgradation and recovery happening.

As far as upgraded recovery is concerned, for the year ended March 2022, we upgraded and recovered Rs 1500 crore and hoping to replicate similar performance this year. That is why I am saying that my GNPA, which is currently at about 5.8 percent, and I would want to bring it closer to 5 percent and NNPA which is currently at 2.6 percent and I would want to bring it closer to 2 percent.

We’ll continue to monitor the new book by doing a tight review of the portfolio.

What are you expecting for the banking sector from the Union Budget?

As a banker, there are three-four things about which I’ll be happy if things move in the positive direction in these areas.

One is in the area of legal remedy for NPA cases. We are able to see traction and closure of cases through the Insolvency and Bankruptcy Code (IBC) but still there is good scope to say that it is a major boom for cleaning NPAs in the banking system.

Therefore, a little more proactive and solution oriented legal system instead of promoters delaying the resolution of payments and the cases getting prolonged for 5-6 years.

Earlier resolution of the cases would be better for the capital requirement of the banks as they can proceed with their business as usual.

Secondly, as the worst of the pandemic is behind us, it is now time to start looking at the banking sector with little more profitable goals. If you are going to offer by way of convenience at a cheaper cost or free, banks will have to spend more capital in setting up digital banking mechanisms for medium and small sized banks, therefore, at the end of the day there are stakeholders putting money and therefore we need to ensure that they get adequate returns.

Hence, we should let the banks decide the pricing as per the riskiness of the customers and market expectations instead of applying the same for every customer.

Third thing we would want to see is inflation moderation at around 4-6 percent as looked by the central bank alongside economic growth to happen. Also, looking at the liquidity situation, there is a need to pass on the increased interest rates through deposits to retail depositors and due to this the banking sector as a whole will see some change in NIM.

If the central bank can bring in some kind of streamlining and balance in hiking the interest rates and working on liquidity to take care of inflation and growth.

Till now, RBI has done a commendable job and going forward, I am sure that RBI would be sensitive to the fact that liquidity is short in the market and more pressure will come on the bank. Now everything cannot be passed on to the customers.

What are the major challenges for CBDC roll out?

It’s only been a few days since the trial has started and the involved users are cautiously adapting it. I am sure that the initiative is in the right direction and there would be some initial issues.

One of the things I kept hearing from the market is that the concern among the users is that the transaction is being monitored or not by the banks involved in the process.

We need to closely check the initiatives and make sure everything moves in the right direction.

JINIT PARMAR is a correspondent based out of Mumbai covering banks, banking trends and more. #banks #bankingtrends #RBI

T

5 Likes

How exactly are Dreamfolks making money please?

Was not clear from the few documents that i read. Yet to read Drhp though.

So if one entry costs - say 100 - how is revenue split?

Assuming the person used their complimentary card access.

Now if another person used direct app to book and enter, how will that 100 split?

Service_provider, dreamfolks, airport(?), card issuers are the players i can think of. Wondering how much will each get - roughly.

Thanks

1 Like

Plz go through the above.

IPOs though have lost their mojo as they came at high valuations in bullish time earning high fees for LMs & Promoters and HNI funding getting stopped.

Bear market IPOs make best returns. Lets wait for them.

Hi

Are you still tracking Brand Concept ? Recent nos have been good and expected to remain so post covid pent up demand and travel. Q3 nos should again be good. Lew licnse of other brand also being obtained.

Mangement quality seems decent WITH CEO Abhinav Kumar having worked WORKING IN MANY MNC cos .

//www.marketscreener.com/quote/stock/BRAND-CONCEPTS-LIMITED-40135714/news/Brand-Concepts-Limited-Enters-Long-Term-Contract-of-Licensing-with-ABG-Group-42632181/

Discl_ invested tracking qty

1 Like

https://twitter.com/ETNOWlive/status/1608001063449415681

Twl running .

Opp size n order book is good. iNDIAN RAILWAYS on big growth path under able minister n modi govt

3 Likes

A must watch video.

Only optimists make money in investing.

10 Likes

A good interview

1 Like

Seems it’s good time to enter considering price, EBITDA, cash flow…

1 Like

The-Singing-Sun-Note-by-Sunil-Singhania may 23.pdf (118.9 KB)

A good read. India remains a bright spot for investing & FIIs are coming back.

7 Likes

Must watch interview of Ugro MD Shachindranath. Seems one can bet upon him & UGRO.

Discl- Invested recently. not a sebi regd analyst.

4 Likes

1 Like