VCL stands out with strong internal tailwinds — Improving margins from backward integration (Chrome mining complex) + New product introductions (DMSO, Chrome metal, Strontium Carbonate etc. which qualify for import substitution) + 15-20% expected growth in margin accretive Barium Chemicals segment + Capacity expansion for its existing products (Chrome Oxide Green).

All this combined with decent valuations makes VCL a compelling case for closer scrutiny.

Financials

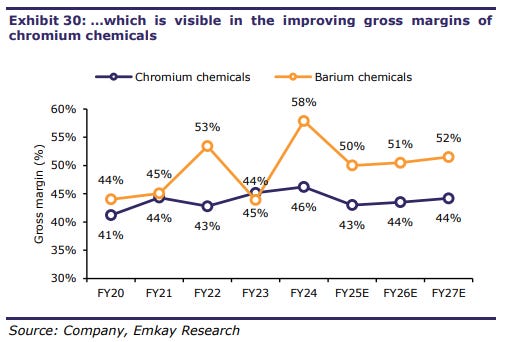

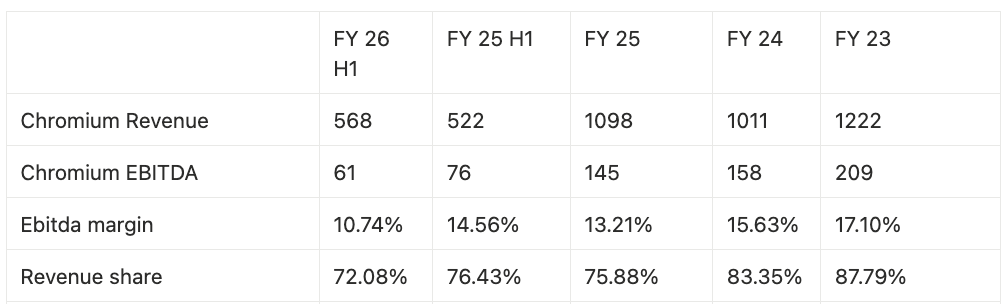

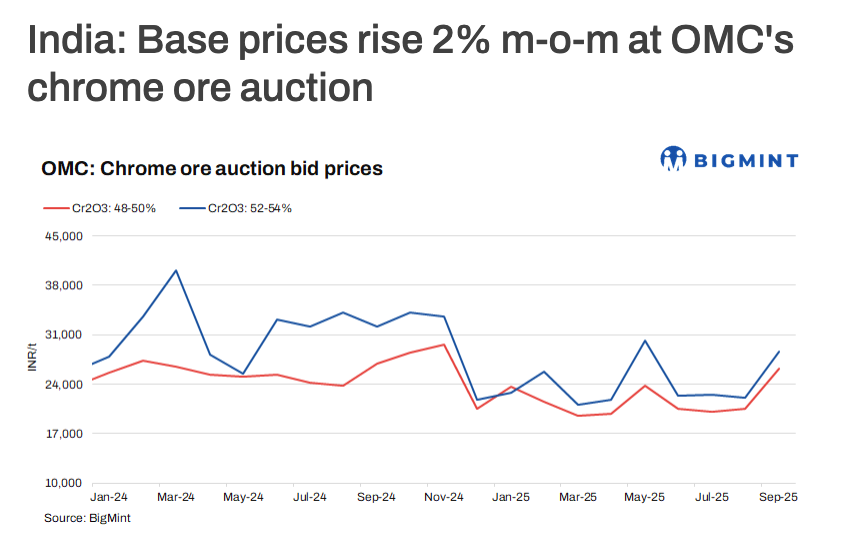

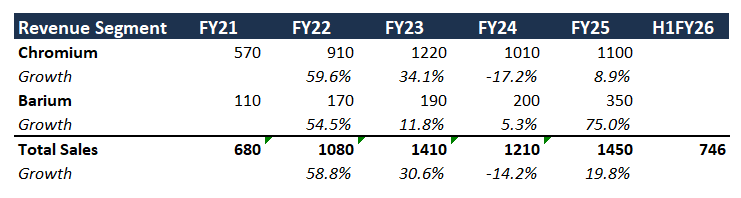

The Co’s revenue had grown at a fast clip except during FY24, when Chromium sales plunged 17% y-o-y, due to declining price realizations, softened export demand and increased chrome ore prices which the Co could only partially pass on.

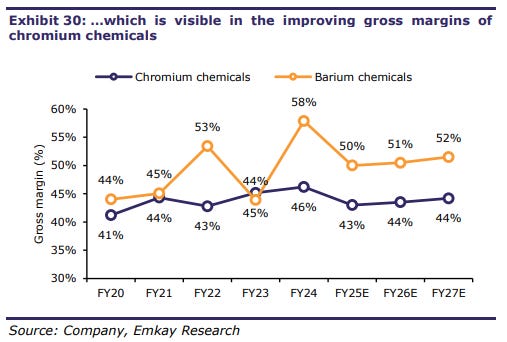

During the same time, the Barium segment’s share as a % of revenue increased as well. This trend is expected to increase and is positive for the company as the Barium segment boasts higher gross margins in comparison to the Chromium segment.

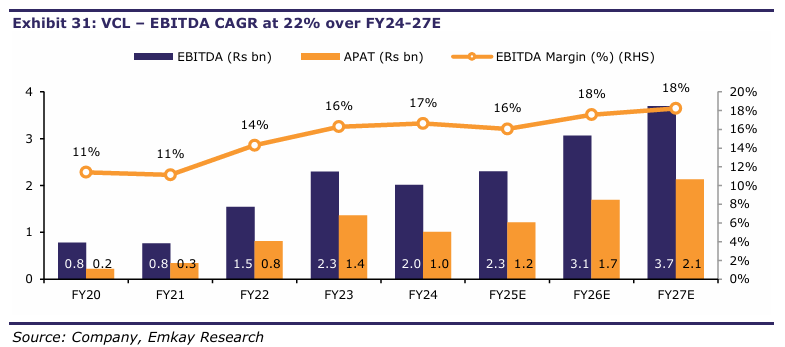

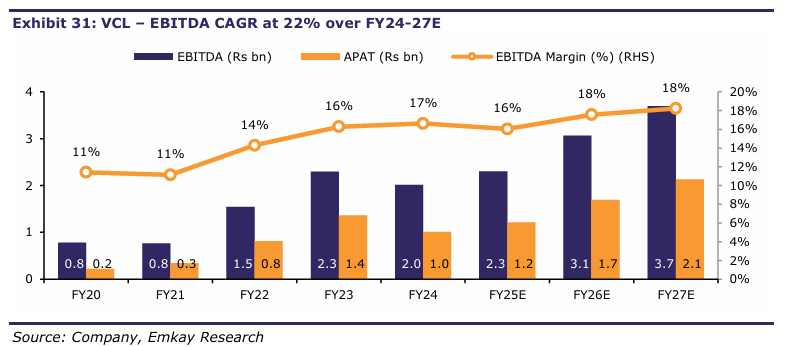

Historically, EBITDA margins have been steady around ~16%.

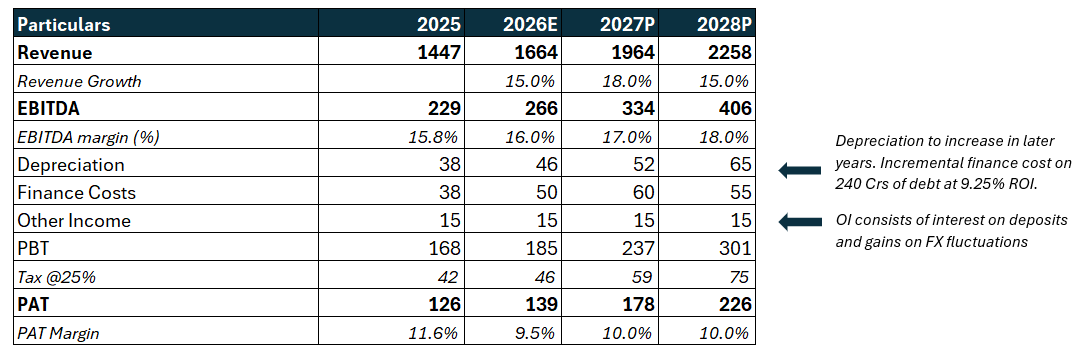

We don’t endorse the FY26 and FY27 estimates of 18% EBITDA margin provided by Emkay Research. As of H2 FY26, EBITDA margins were ~15.2%. For our forward projections, we will consider the EBITDA margins to increase at a more conservative pace.

Debt funded Capex

As of Nov 2025, consolidated debt stood at ₹450 crore.

Source: Care Edge credit rating (Nov 2025)

However, the same is expected to increase as the company is undertaking a ₹320 crore capex for setting up a DMSO plant and a new chrome oxide green production line, funded through ₹240 crore term debt and ₹80 crore internal accruals.

Source: Care Edge credit rating (Nov 2025)

This action will impact the Co’s:

- Debt levels and finance costs

- Depreciation expenses

- Higher capex leading to lesser FCFs

Apart from non-fund-based limits (LCs, BGs etc.), the Co’s debt is divided into two parts — working capital and term loans. As per the Co’s most recent rating report, the average utilization of working capital limits stood at ~81% for 12 months ended August 2025. The limit being at 162 Crs.

Based on the same, we can infer the remaining term debt at ₹320 Cr. Add to the same ₹240 Cr of term debt owing to the new facility, total consolidated debt would stand at ₹560 Cr. Based on VCL’s current interest rate of 9.25% (from FY25 AR), the incremental debt would lead to an additional interest outflow of ₹22 Crs.

Depreciation expenses would not surge as much because the capex would be in the form of Capital Work-in-Progress (CWIP) in the first 1-2 years. CWIP means that it is not available for use ; it is still being constructed or installed. Therefore, no depreciation is charged on CWIP. Hence, depreciation would only meaningfully increase from FY28 onwards.

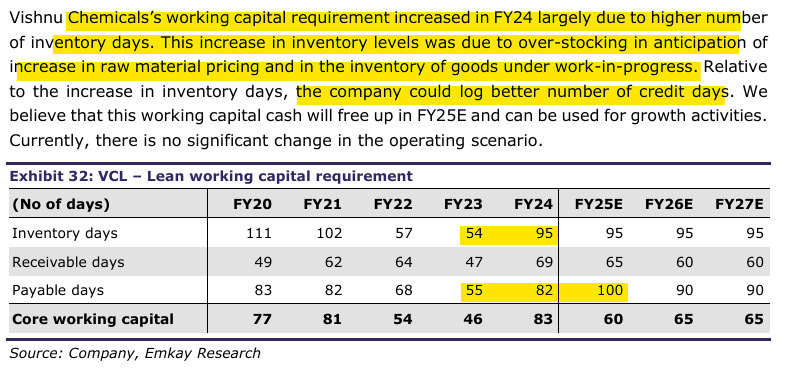

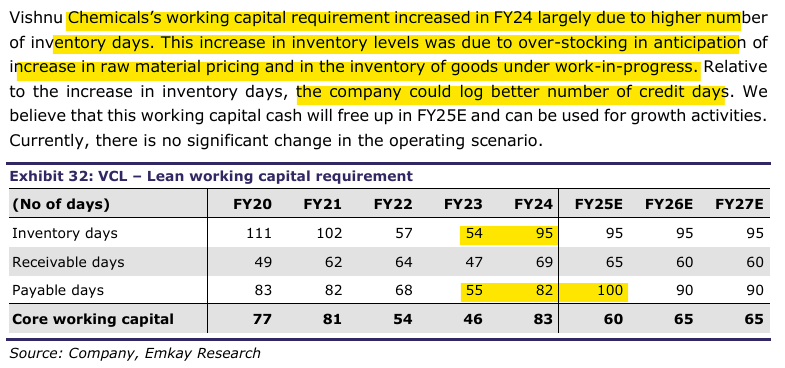

Working Capital

The commentary from Emkay Research is satisfactory. However, working capital intensity is likely to trend downward. Erstwhile, VCL imported 100% of its chrome ore requirements and maintained higher raw-material inventory to ensure uninterrupted production.

The acquisition of the chrome ore mine is aimed at mitigating the impact of chrome ore price volatility on profitability margins and moderate inventory holding levels.

Of the total reserves in the mine, ~4,00,000 tonnes are open-accessible, sufficient to meet VCL’s requirements for ~2.5–3 years. With further expansion, VCL estimates the life of the reserve at 30 years.