Vishnu Chemicals is India’s leader in Chrome based chemicals industry. The company is the seller of following products:

Barium Carbonate, out of these, is a recent addition by acquisition (100% shareholding) of a company called Solvay Vishnu.

Before this, there major products have been Sodium Dichromate and Basic Chromium Sulphate.

These chromium compounds are majorly used in leather tanning industry, paints, pigments and as dye stuff, photographic films, Electroplating (chrome plated water taps, and other bathroom accessories), and as an oxidizing agent.

The leather industry in India should grow at the rate of 24% for the next 5 years. (Source: http://www.makeinindia.gov.in/sector/leather/)

Given this growth rate, and the distribution network of Vishnu, it can be a good opportunity.

Now, we deep dived into various factors of the company.

- Operating Efficiency

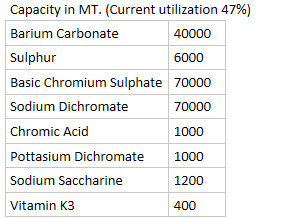

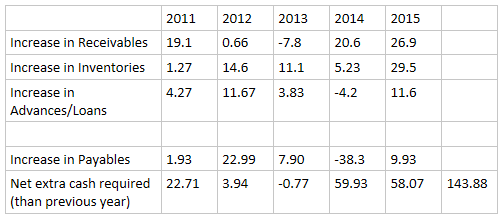

As seen in the above table, the net working capital of the company has increased by 144 Cr in the last 5 years. However, the OCF of last 5 years has been 146 Crs. Hence, they are able to meet the WC requirements by OCF. Although no cash is generated for investment purposes, there current utilization is only 47% and they do not need CAPEX investments till they double the sales.

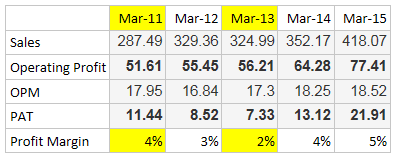

As seen here, sales have been growing consistently and the OPM is also increasing. In the last 2 quarters of FY16, operating margin has improved to 18.9% than 16.3% last year. One of the reason, which we envisaged, was buying of Solvay, which provideed around 6000 MT of sulphur annually (major raw material). The other can be because of sales of Barium Carbonate (need to check).

The real operating leverage will be seen in PAT, because there is no further investment required. So, a greater chunk of operating profit will translate to PAT, giving higher growth rate for PAT than sales.

- Financial Health

The company’s total debt is around 177 Crs. Interest coverage ratio to operating profit lies at 2.30, and hence we do feel that company is not into any financial risk.

- Growth Drivers

The company has mentioned in the annual report that they plan to double their sales (from 2015 levels) by 2017. That is total sales of 1000Cr by end of FY17. The company has set up a subsidiary in hong kong, and is also targeting to enter China market.

Also, incremental receivables/sales ratio shows that company is trying hard to increase sales (Not a good sign). But, we believe that this is because they are trying to enter new markets where they are not present.

The second growth driver is the expected growth in the leather industry market, which is 25% as per Make in India website.

The third growth driver will com from the sale of Barium Carbonate chemical, whose major application is in the tiles industry, which is also poised for growth.

While we do not believe that the aggressive target is un-achievable, we believe that they can atleast reach this target by FY18 end. Given the operating leverage they have in hand, EPS can actually grow at double the sales growth.

Concerns:

-

Incremental receivables ratio is increasing, however, this might not pave as entry to new market, hampering sales.

-

There have been a petition by Vishnu Chemicals to put import duty on chrome based chemicals, which was rejected. What has been the rationale behind that? Is there a threat to Vishnu by overseas companies? The link to the petition is below:

http://dgsafeguards.gov.in/newversion/FINAL%20findings%20%20sodium%20dichromate%201.pdf

- Working Capital incremental has been tremendous in the last 2 years, if this continue, and WC loans are required to sustain growth, it can affect the EPS growth rate.

Disc: Not invested

Akash & Nikhil