Thanks for the exhaustive long term profitability analysis of the company.

Can u plz throw some light on the contingent laibility of 148 Cr. That would be useful.

Regards,

Ranvir Dehal

Thanks for the exhaustive long term profitability analysis of the company.

Can u plz throw some light on the contingent laibility of 148 Cr. That would be useful.

Regards,

Ranvir Dehal

This is absolutely wonderful piece of work @Divyachawla ! Super Like!!

Thanks for sharing.

@Divyachawla - Outstanding in-depth work on both the luggage and agro-chemical industries. Saving the television industry for post-lunch. Please do post more often here on VP as well.

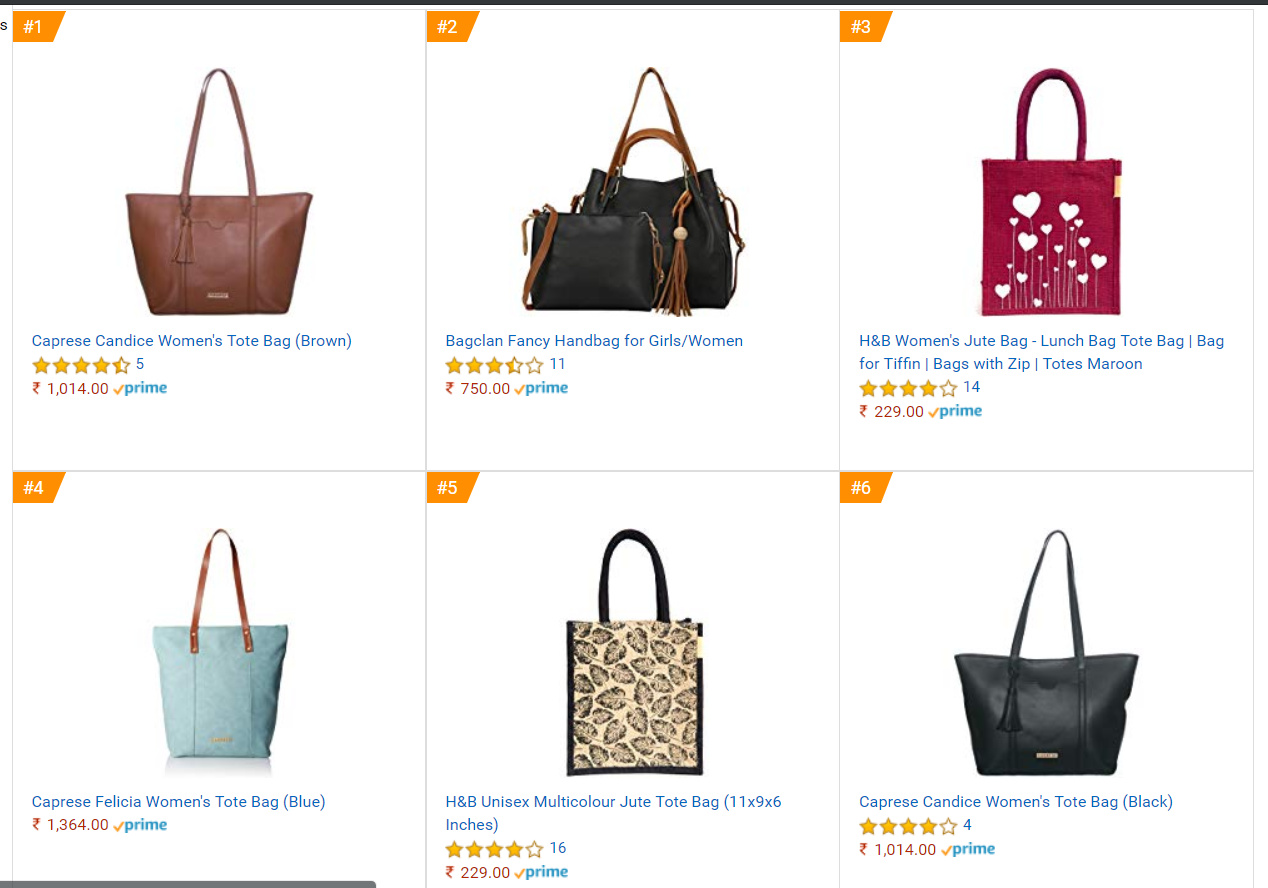

Caprese women handbags #1 best selling on Amazon… Fastest growing segment for VIP Industries.

https://www.amazon.in/gp/bestsellers/shoes/1983356031/ref=pd_zg_hrsr_shoes_1_3_last

I was evaluating Safari and VIP but it will go out of my watchlist now. I recall there was hue and cry when she was shifting to London with very high compensation. Now we know why she opted for London. It is her personal choice but shows it clearly where the priorities lie especially when there is no clear succession planning. Also, one must note that a VIP insider has become a fierce competitor in the form of Safari.

Yes its sad to know all this- priorities seem to be different. But as they say, Excellent business and Bad management will still reward stakeholders in the long term. With urbanization,increase in discretionary spend,migration from railways to aeroplanes, I feel a huge market potential ahead for VIP. Mr Sudip Ghose is a capable person and I am hopeful of him taking the business higher.

Carlton, Skybags,Caprese,Aristocrat all brands are growing with good margins; in branded luggage space, they have moat and differentiation. Safari stands no where if we do a scuttlebutt and figure out what variety VIP has vs Safari.

Invested in VIP, so views may be biased

good one from @dineshssairam

Nothing much in the article, if anyone can share the edelweiss report , please do,I was unable to find it. Thank you

EDELWEISS:

We recently met Mr. Dilip Piramal, Non-Executive Chairman, VIP Industries (VIP), who envisages strong industry tailwinds and prospects for the company. Key takeaways: 1) Market is shifting towards branded players with GST in place. 2) The backpack category is leading to shorter replacement cycles and robust sales growth. Management perceives institutional and export orders as additional growth avenues, and estimates overall sales would jump 20–30% per year for the next few years. VIP is doubling capex to expand capacity in India and Bangladesh to counter the rise in procurement cost from China. This, management believes, would boost margins structurally. We estimate CAGRs of 20% in sales and 25% in PAT over FY19–21E. Maintain ‘BUY’ with a target price of INR566 (40x Q1FY21E EPS).

Strong structural growth drivers in place

Management envisages favourable industry dynamics to support robust volume growth across brands and channels: 1) GST implementation has led to a shift in market share to branded players, especially in the entry segment. 2) The backpack category has been gaining momentum given shorter replacement cycle (two years), leading to 30%-plus growth for VIP. 3) Luggage sales in the hypermarket format have been growing 20–25%. Furthermore, with additional levers such as institutional and export orders, management expects sales to take off 20–30% per year.

Capacity scale-up to lift margin

VIP believes it is favourably placed vis-à-vis peers in the wake of capacity scale-up in Bangladesh from 0.17mn/month in November 2018 to 0.3mn/month in April 2019 given overall sales volume of 1mn/month. The company’s plan to increase the proportion of India-and-Bangladesh manufacturing in the overall supply mix should lever up margins. Furthermore, it recently raised prices, which were held back due to intense competition in the entry segment. Hence, management expects EBITDA margin to rebound to 11–12% in a quarter and to about 15% in a year or so.

Outlook and valuation: Profitable growth ahead; maintain ‘BUY’

We believe VIP is lodged in a strong position to cash in on industry tailwinds with sharpening focus on scaling up. With significant growth and margin expansion levers in place, we estimate CAGRs of 20% in sales and 25% in PAT over FY19–21. Maintain ‘BUY’ with a target price of INR566. At CMP, the stock trades at 36.4FY20E.

Q4FY19

PAT down 28% at Rs 25.3 crore against Rs 35 crore.

EBITDA down 27% at Rs 39.6 crore

Margin down 590 bps at 9.1 percent

Revenue up 20% at Rs 435 crore versus Rs 362.6 crore

Board has recommended a final dividend of Rs. 2.00 (Rupees Two only) per equity share of Rs. 2/- each for the year ended 31st March, 2019. 52nd Annual General Meeting of the Company on Tuesday, 30th July, 2019.

Appointment of Mr. Tushar Jani (DIN 00192621) as an Additional Director for a period of 5 years

Appointment of Mr. Ramesh Damani (DIN: 00304347) as an Additional Director for a period of 5 years

Very poor result. Do we know if there was any impact due to fire incident?

The result can be looked at from various angles. The topline growth points to the fact that this industry is growing at a rapid pace. They have ended the year with an average ROE of 27% which is a fabulous ending. Those are all positive developments for the overall sector.

The cons are obviously the erosion in margins due to input costs. However, over 10-12 period, VIP has an average net margin of 6% with an average ROE of 22-23%, which makes the industry so lucrative to be in. For the quarter ended March 2019 the margins are in the region of 6% with gross margins are at 44%.

The reason why the earnings number has shrunk so much is because of operating leverage which is quite high in the luggage sector and O/L works both ways. However, the topline growth has remained intact and even exceeded historical standards whereas margins are a function of various temporary aspects and are more likely to revert in the near term than not.

VIP has also embarked on a brand refocus program as leaders typically do to shore up and protect margins. If the topline growth continues and margins just stop shrinking as they are likely to do, one can easily visualize an increase in earnings power.

I think these are very good results overall.

However the VIP chart seems pretty weak with falling momentum

Best

Bheeshma

Not Sure I understood their income statement. How come revenue lines are almost same in the standalone and consolidated reporting but cost items differ significantly. Am I right in assuming that VIP is hoarding 7cr (in Q4) of additional profit in one of its subsidiaries where sales are negligible?

@bheeshma also if sales growth is good enough why would O/L work in the reverse direction? Is it not simply high material costs that is impacting profitability? There is 7% movement in gross margin yoy.

VIP has a Bangladesh subsidiary to manufacture soft luggage that adds to its bottom line. You can read more about it in the published interviews of its KMPs.

The degrowth in gross margins is greater than the growth in sales due to input costs, hence you see a disproportionate contraction of earnings. VIP has an operating leverage of 4-5x and any contraction of gross margins will certainly impact earnings growth

Sure thanks! Don’t you think this biz model of buying from China and selling here in own brand name is unsustainable. Folks used to think the same about Macromax till Chinese arrived themselves and killed the brand forever. I am pretty sure that Chinese counterparts will die for this kind of RoE @30%. They generally target 10-15% as base case wherever they enter given their low CoC. India has always been price sensitive market and they could also build sales organisation overtime like they have done for cell phones. I don’t think VIP or Safari are going to die but up for significant margin challenges and moderation in return ratios.

Your thoughts presenting here are very assuring. I always await your reply on VIP and Safari.

An interesting thing to me is that they have now Tushar Jani who is the the founder of Blue Dart and seems to be the man of logistics and would understand that industry very well.

Second is Ramesh Damani who is associated with D’mart and an expert in securities market. Imagine VIP going into all the D’mart stores across country with their Aristocrat brand for the TG, apart from their already present exclusive stores.

It will be interesting to see the value that they will be bringing to VIP industries. I am sure something worthwhile is in store.

I will be eagerly waiting for results of Safari Industries also.

Disclosure: I exited both VIP and Safari sometime back after their last quarter results and eagerly waiting for re-entering.

The impact of Anti dumping duty on the Chinese imports is quite visible on the margins.

It is not only luggage industry you can see the margin pressure on Footwear industry as well.

I think it would take some time to get the margins stabilized.Also I think getting back the previous peak margins is going to be tough.

Margins will be contained by a lot of factors such as :-

Imports from china is costlier now so the alternative sources are bit costly… Such as imports from Bangladesh or in-house manufacturing.

There would be some discount war as the industry has 3 big players now… Americans tourister, Safari and VIP, Also FastTrack is racing up. E-commerce players are also coming with their own brands, And they are (in)famous for cashburn . With so much players and the game of market share would lead to lot of discounting .

If I have to make an investment thesis, I would take the margins as 200 to 300 bps down from the peaks.And come out with a valuation comfort accordingly.

Lot of things to keep on watch :-

How VIP is able to keep the margins up. What if govt imposes duty on Bangladesh imports tomorrow. Do they have in-house manufacturing or domestic sourcing where they can keep the margins.?

How they would fight against the other players specially with the ecom players.

The product diversification, Atleast VIP is leading the race here.

Also the offline retailers would also come with their brands, so how VIP fights that game where It has to partner with its competitors.