Water lies at the heart of VBL’s business. But surprisingly, the question of water availability has not been discussed adequately in any of the analyst concalls since the company listed in November 2016. The DRHP lists concentrate, sugar and packing material as VBL’s principal raw materials. Of course, the Annual Report devotes lot of pages exclusively to Water, but all of it in the context of ESG. In general, the importance of water in the overall scheme of things appears to be grossly underplayed. Perhaps, water constitutes only a small portion of VBL’s overall costs, and hence lack of attention to it by the overall investor community. But my concern is more with the availability of water itself, than the cost of it.

VBL gets its water from two main sources – supply arrangements with local authorities like municipalities where the plants are located (about 30 %), and groundwater from own borewells (about 70 %). Recycled water is not used. The company has long-term agreements with local authorities for supply of water for its plants. These supplies are given subject to the company meeting the certain conditions including for the recharge of water. VBL claims its water recharge is best in class across the world, and its recharge numbers are well above the statutory obligations at each of its manufacturing location. Despite this, water supply is not a right and nothing stops the local authorities from denying water in a year of scarcity.

The bigger source of water is through borewells. The Central Ground Water Authority (CGWA) - constituted under Ministry of Jal Shakti, Govt of India regulates this. Their main job is to monitor and maintain the groundwater resources and prevent over-exploitation of the ground water. CGWA & the respective State Ground Water Authority (SGWA) regulate extraction of water from borewells, check adherence to guidelines, levy charges and grant permissions. The CGWA classifies geographies in different categories such as Safe / Semi critical / Critical and Over-exploited - with regulations becoming progressively stringent for each higher level. VBL’s 2023 Annual Report says 26 of the company’s 33 plants are in Safe / Semi-Critical zones. The remaining 7 contributed 16 % of the total production in CY2023. Thus, there is a regulatory limitation on how much water the company can draw from its own borewells. In the past, some of the company’s greenfield expansion has actually been driven by inability to draw more water at existing locations.

The permissions to extract water are granted for 3 years at a time and then renewed. This is largely a routine cyclical activity, though nothing can be taken for granted. The DRHP – filed in 2016 - says permissions for groundwater extraction at 8-odd plants were pending with the authorities.

In response to a questionnaire sent to the company, the management declined to provide an updated status of the same. A request to share the overall cost of water was also declined, but it said the pricing varies significantly from State to State, with charges ranging from Rs. 0.026 to 0.26 per liter.

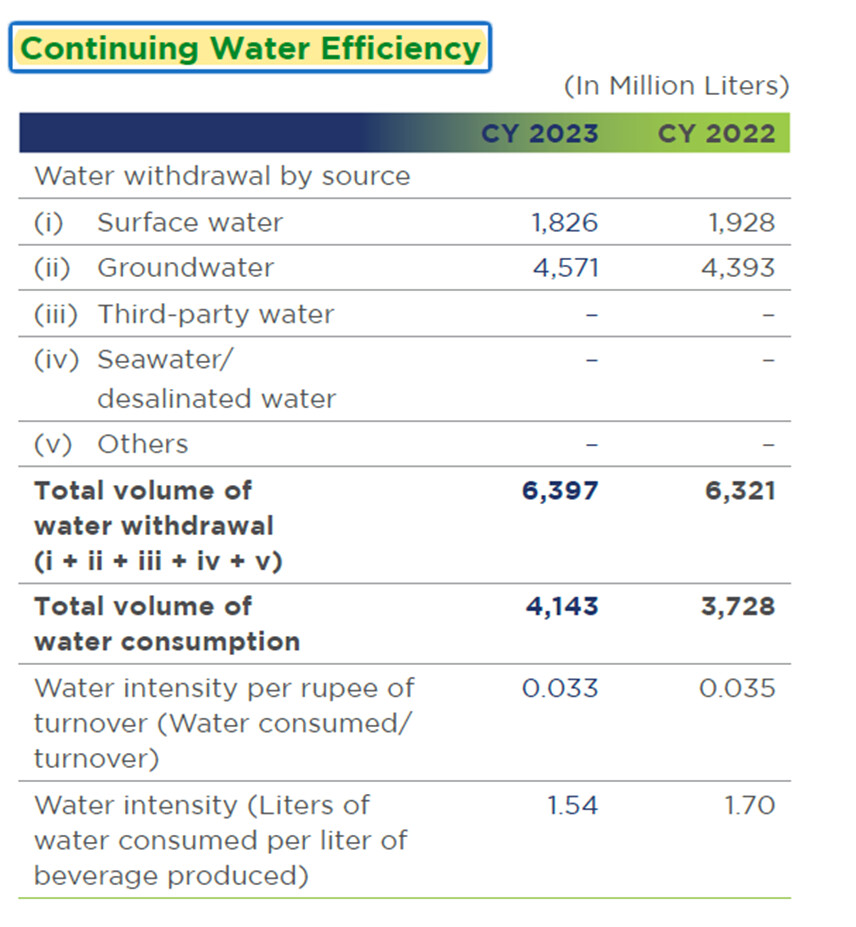

It should be noted that the company has not faced any material disruption in water supply historically. Additionally, with over 34 beverage manufacturing plants in India, it can make water available from other nearby locations to safeguard operational continuity, says the company. The DRHP said at least 21 of its manufacturing plants were in “Safe” zones. It is also heartening to see the company’s water usage has improved consistently, from 1.94 liters of water consumed per liter of beverage produced in 2019, to 1.70 in 2022 and 1.54 in 2023. The added focus on dairy based products and juices as compared to pure carbonated soft drinks will reduce water intensity of the business in the long run. Geographical dispersion – both within India and overseas – also reduces the long-term water availability risk for the business.

In the current year, the IMD has predicted normal to excess rainfall for the country. The IMD, as well as other international weather bodies are predicting an enhanced possibility of La Nina and a positive IOD (Indian Ocean Dipole) event developing later this year, both of which will be good for Indian monsoon. If this materializes, the depleted water table levels due to last year’s El Nino will get replenished alleviating water risk for the country in the immediate future. Nevertheless, water is going to be a more and more precious resource in the years to come. This will be a factor to watch for Varun Beverages.

(Disc.: Invested)

RJ Corp successsion plan

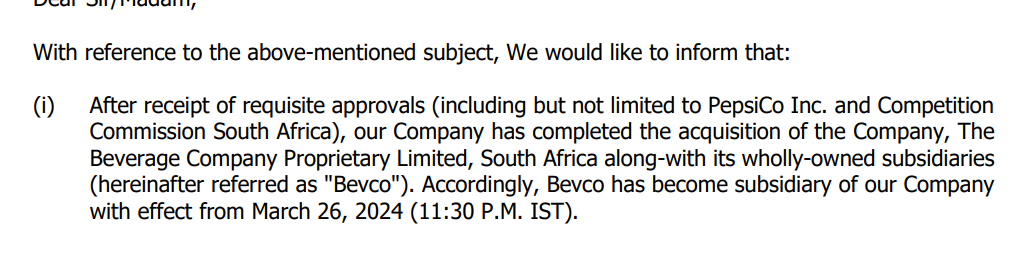

As Bevco became subsidy on 26th March , 2024 , will its earning will be part of March quarter consolidated earning ?

Yes, but only six days earnings (26-31 March, both days inclusive) will be consolidated in the March quarter results, so the effect will be minimal. Full quarter earnings will come in from 1st April.

Pabrai has adovocated for CCI in multiple forum in last few months. One thing , business with so many emerging economy including its main market in Turkkiye is vulnerable of significant forex risk. Infact both S&P and Fitch current rating for CCI highlights this risk.Interested to know Mohnish’s view on this risk. Infact Varun Bevrages also encountered it in its Africa business or for that matter Airtel is facing with Nigeria market.

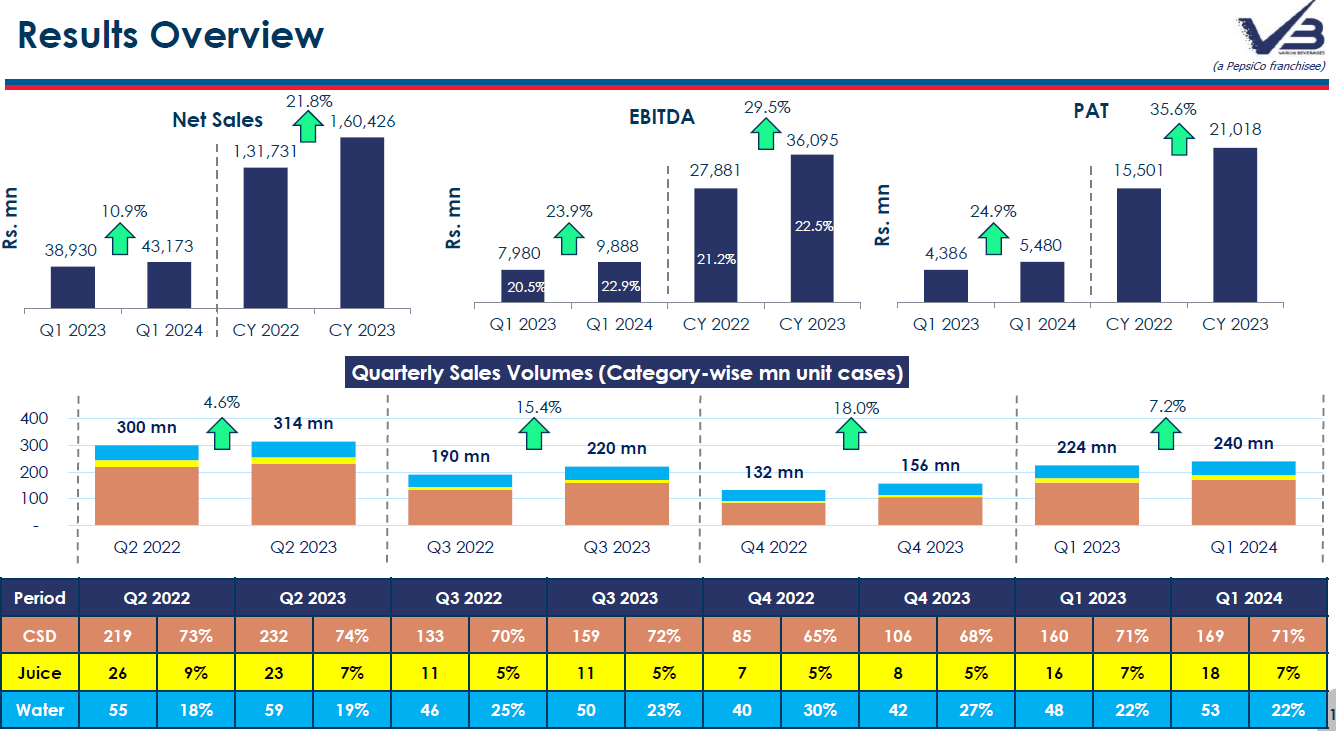

Q1 2024 results: Good YOY growth

- Consolidated sales volume grew by 7.2% to 240.2 million cases in Q1 CY2024 from 224.1 million cases in Q1 CY2023.

- PAT increased by 24.9% to Rs. 5,479.8 million in Q1 CY2024 from Rs. 4,385.7 million in Q1 CY2023 driven by volume growth, increase in net realization and improved profit margins.

- Gross margins improved by 385 bps to 56.3% from 52.4% during Q1 CY2024 primarily due to reduced PET prices as well as the focus on reducing sugar content and light-weighting of packaging. Approx. 46% of our consolidated sales volumes come from Low sugar / No sugar products.

- EBITDA increased by 23.9% to Rs. 9,887.6 million YoY and EBITDA margin improved by 240 bps to 22.9% in Q1 CY2024, led by higher gross margins and increased realization.

Next two summer quarters to follow ![]()

Concall Notes - May 2024

Financial Performance:

- Consolidated sales revenue grew by 10.9% to Rs. 43,173 million in Q1 CY2024.

- Consolidated net realization per case increased by 3.5% to Rs. 179.7.

- Gross margins improved significantly by 385 basis points to 56.3%.

- EBITDA increased by 23.9% to Rs. 9,887.6 million.

- PAT grew by 24.9% to Rs. 5,479.8 million.

Operational Highlights:

- Three new greenfield facilities were commenced in Supa, Maharashtra; Gorakhpur, Uttar Pradesh; and Khordha, Odisha.

- Sustainability efforts include reducing sugar content and lightweighting packaging material.

- Entered into an Exclusive Snacks Appointment Agreement to manufacture and package Cheetos in Morocco by May 2025.

- Successfully completed the strategic acquisition of the Beverage Company (BevCo) in South Africa.

- Expecting the DRC greenfield plant to start production in the next quarter.

Future Growth Initiatives:

- Focused on three growth engines: South Africa, new territory of DRC, and snack food production in Morocco.

- Expecting favorable operating and financial leverage in CY25.

- Debt levels are well within norms, with a Debt-to-EBITDA ratio around 1 - 1.25.

Challenges and Opportunities:

- Delay in the Holi festival impacted the seasonality cycle in the first quarter.

- Market expansion plans in South Africa and DRC to capture growth opportunities.

- Continuous efforts to reduce sugar content and enhance sustainability practices.

Market Expansion:

- South Africa market potential is close to 1 billion cases with significant room for growth.

- DRC market has a population of over 100 million, aiming to capture a sizable market share.

- Focus on enhancing production capabilities and making new acquisitions to strengthen global presence.

Debt Management:

- Debt levels expected to stay consistent with Debt-to-Equity ratio around 0.5 - 0.7.

- Amortizing debt for BevCo acquisition and CAPEX in the next couple of months.

- Long-term strategy to maintain leverage ratios and enhance financial efficiency.

Industry Trends:

- Quick commerce and e-commerce channels still not prominent in the segment.

- Continuous focus on product innovation and market penetration to drive growth.

- Positive outlook on future growth potential driven by new projects and strategic acquisitions.

Source:Screener notes

Disc: Invested

JFM CY24 results show a strong improvement in margins with OPM and net margins at all time high and a big jump in gross margin over the last year. Sales growth was lower than the recent past at 11 % but with large capex and inorganic growth initiatives coming online, growth can be expected to pick up in the coming quarters. Meanwhile, the management defined “3 growth engines” in the concall, all of which pointed to international markets. Some highlights from the concall:

- Three Growth Engines:

- South Africa’s combined territory with Lesotho, Eswatini, Namibia, Botswana, Mozambique and Madagascar.

- Entry into new territory of DRC where PepsiCo is not present at all as of now, the commercial production here from our new state-of-the-art greenfield plant is expected to start from the next quarter.

- Entry into snack food production by May 2025 in Morocco.

-

In JFM CY24, volume growth was 7.2 % and net realization per case growth of 3.5 %. International markets command a higher realization per case. Volume growth internationally is 21.9 % led by Zimbabwe and Morocco.

-

DRC: Greenfield plant in DRC is expected to start by the next quarter. DRC is more than 100 million population and warm climate. We have put 2 large lines and our capacity is about 35 million cases

-

Morocco: Company has entered into an exclusive agreement to manufacture and package Cheetos into Morocco, by May 2025. In terms of return on capital, food business is as good or better than the beverage business because the capex is much lower.

-

South Africa: BevCo has 5 plants. South Africa is close to 1 billion case market, with one of the highest per capita consumption rates of about 250 servings per person. However, PepsiCo’s market share is very meagre at 1.8 %. This presents us with a huge upside for growth

-

Low sugar: 46 % of consolidated sales volumes come from low sugar or no sugar products. South Africa will significantly add up to this achievement, with approximately 90 % of the portfolio being comprised of low or no sugar products in that country. Another country following suit is Morocco. (This is very heartening to note, given that screws are gradually tightening around high sugar products in India - see this and this, for example)

-

Debt: Last year same quarter, the average cost of borrowing was 7.7 %, which this year is 8 %. Most of the capex is already done, now the focus is on repaying the debt. In the past, any time for the last 3-4 years, you must have noticed that our Debt-to-EBITDA is around 1 - 1.25 and Debt to Equity is 0.5 - 0.7. After the season ends in 1 or 2 months, these ratios will be at the same level. By the end of the year 2024, it will be our endeavor to reach the 31st December 2023 debt position.

-

Capex: We measure depreciation as a percentage of revenue and in the long run it has been coming down. Since most of the capex is already done, in the next few quarters EBITDA coming from the 3 new plants in India (Odisha, UP, Maharashtra) and from 5 plants of South Africa should start contributing and DRC should also start contributing.

-

The total number of plants with backward integration facilities now is 13 (not sure what this comprises of - is it PET bottles, caps, water or something else)

-

One analyst noted that Campa Cola in FY24 has done around Rs. 400 crore sales.

(Disc.: Invested)

Great Summary with pertinent points. Here is some info on what backward integration means for their plants.

" the company has set up backward integration facilities for production of preforms, crowns, corrugated boxes, plastic crates and shrink-wrap films** in certain of the companys production facilities to ensure operational efficiencies and quality standards"

Great summary. As per my analysis,

“With a Price to Book ratio of 30, at the current price, the yield is around 1.35%. To justify this, earnings need to grow at a rate of at least 18% per year for the next 10 years.”.

Disc: Invested.

Commercial production of carbonated soft drinks and packaged drinking

water at its production facility at Kinshasa, Democratic Republic of Congo has been started as stated by company

Fy25 Q1 results are out

Net profit at up 25.5% ₹1252.6 cr vs ₹994 cr (YoY)

Revenue up 28.3% at ₹7,197 cr vs ₹5,611 cr (YoY)

EBITDA up 31.8% at ₹1,991 cr vs ₹1,511 cr (YoY)

Margin at 27.7% vs 27% (YoY)

Cons. sales volume growth 28.1% YoY / India 22.9%

Stock split announced: 5Rs FV will split to 2Rs FV

Interim dividend of 25% of the face value, i.e., Rs. 1.25 per share

Ravi Jaipuria, Chairman, Varun Beverages Limited said,

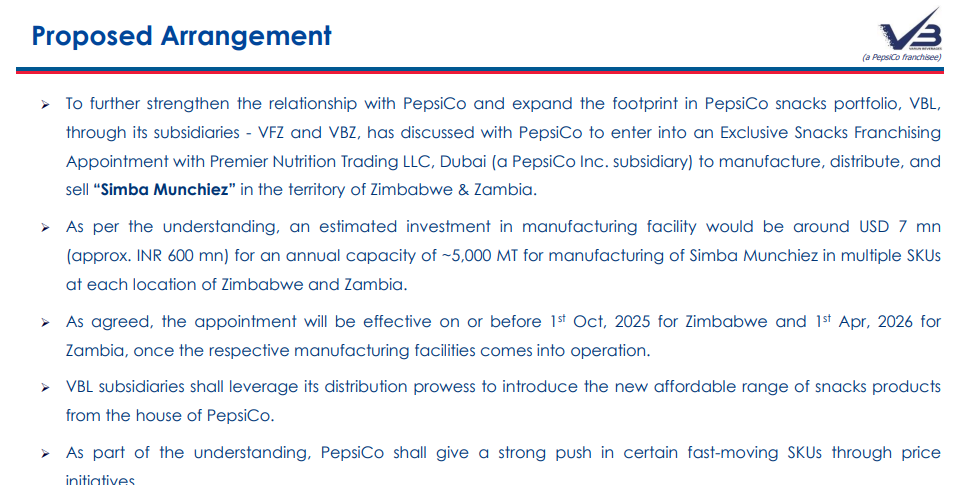

“We are pleased to report robust performance for the second quarter of CY2024, achieving a consolidated sales volume growth of 28.1%, which includes volumes from BevCo. The impressive volume growth of 22.9% in India primarily contributed to this outstanding performance, supported by our expanded capacities, enhanced distribution network, and a strong summer season. Meanwhile, our international markets remained relatively flat, moreover it was a seasonally weak quarter for African market. We are excited to announce further expansion in our partnership with PepsiCo, having entered into an Exclusive Snacks Franchising Appointment to manufacture, distribute, and sell “Simba Munchiez” in Zimbabwe by October 2025 and in Zambia by April 2026. This follows our recent announcement to manufacture and package Cheetos in Morocco by May 2025.

With strong performance in a key quarter, we are on track to deliver healthy double-digit growth in this

calendar year."

Varun Beverages Limited’s Q2 & H1 CY2024 Analysis: Key takeaways!!

Business Outlook:

Varun Beverages (VBL) reported strong performance in Q2 CY2024, with consolidated sales volume growth of 28.1% and revenue growth of 28.3% YoY. The Indian market grew by 22.9%, while international markets remained flat. The company is optimistic about maintaining double-digit growth for the full calendar year, driven by expanding capacities, an enhanced distribution network, and a strong summer season.

Strategic Initiatives:

- Expansion into snack foods: VBL has entered exclusive franchising agreements with PepsiCo to manufacture, distribute, and sell “Simba Munchiez” in Zimbabwe and Zambia, and Cheetos in Morocco.

- African expansion: The company has commenced commercial production of carbonated soft drinks and packaged drinking water at its greenfield facility in the Democratic Republic of Congo (DRC).

- Capacity expansion: VBL has added 9 new plants in H1 2024, including 5 in South Africa, 3 in India, and 1 in DRC.

- Portfolio diversification: The company is focusing on low sugar and no sugar products, which now constitute about 46% of consolidated sales volume.

Trends and Themes:

- Shift towards healthier beverages: Increasing focus on low sugar and no sugar products.

- Expansion in African markets: VBL is capitalizing on the underpenetrated African markets, especially in countries like DRC and South Africa.

- Diversification into snack foods: Complementing existing beverage distribution with snack food manufacturing and distribution.

Industry Tailwinds:

- Growing consuming class and young population in India.

- High per capita consumption of soft drinks in African markets.

- Increasing demand for healthier beverage options.

Industry Headwinds:

- Currency fluctuations in some African markets, particularly Zimbabwe.

- Seasonal variations affecting demand, especially in African markets.

- Regulatory challenges, such as sugar taxes in some countries.

Analyst Concerns and Management Response:

-

Concern: Impact of less out-of-home travel on water business.

Response: Management acknowledged some impact but emphasized that they are not aggressively pushing water sales. -

Concern: Sustainability of double-digit growth in India given high base and seasonality.

Response: Management expressed confidence in maintaining double-digit growth, citing stability in South India and potential growth from new territories. -

Concern: Working capital days increase.

Response: Management explained this was due to strategic purchasing of PET chips and expects normalization in the coming months.

Competitive Landscape:

VBL maintains a strong partnership with PepsiCo and is gaining market share in various territories. In Zimbabwe, the company reported a 71% market share, 35% in Zambia, and about 30% in Morocco (including water). In South Africa, the market share is currently low but growing.

Guidance and Outlook:

The management consistently expressed confidence in achieving double-digit growth for the full calendar year 2024, both in India and on a consolidated basis.

Capital Allocation Strategy:

VBL is investing heavily in capacity expansion, with a planned capex of Rs. 3,600 crore for CY2024 and about Rs. 2,600 crore for CY2025. The company is also focusing on strategic acquisitions, such as BevCo in South Africa, to expand its market presence.

Opportunities & Risks:

Opportunities:

- Expansion in underpenetrated African markets.

- Diversification into snack foods.

- Growing demand for healthier beverage options.

Risks:

- Currency fluctuations in international markets.

- Regulatory challenges, such as sugar taxes.

- Seasonal variations affecting demand.

Regulatory Environment:

The company is adapting to regulatory changes, such as the requirement to use 30% recycled PET content from April 2025. VBL is preparing for this through a joint venture plant and has already started trials with recycled PET.

Customer Sentiment:

Customer sentiment appears positive, with strong volume growth in India and stable performance in international markets. The shift towards healthier options indicates changing consumer preferences, which VBL is addressing through its product portfolio.

Top 3 Takeaways:

- Strong Q2 performance with 28.1% volume growth and 28.3% revenue growth, driven by robust Indian market performance.

- Strategic expansion into African markets and diversification into snack foods through PepsiCo franchising agreements.

- Continued focus on healthier beverage options, with low sugar and no sugar products now constituting 46% of consolidated sales volume.

In spite of posting best ever sales, volume and margins growth, with South Africa’s Bevco positive guidance, Bagging the food/snack business from Pepsi, Interim dividend and stock split…You name it they have it. Still Why is the stock falling?

Any views…please.

Price is at ATH, been in an uptrend for 20 months, tripled in that period, doubled in the last 1 year, now trading at P/B of 21 and P/E of 76, with a market cap of 1.8 lakh crores, and the price has corrected 16%. Nothing surprising.

Have a position, in good profit, so take my view with a pinch of salt.

I agree, this is a logical explanation. but what is the right valuation then considering we don’t have comparable business in listed domain? Is it just that everyone is correcting VBL too is?