I would say RoCE / RoIC should be higher than the Cost of Capital (Or RoE should be higher than the Cost of Equity), as RoE alone can be artificially inflated by the use of excessive Debt. Besides, Debt itself is a form of Capital, so it makes no sense to exclude it from a calculation of Cost of Capital.

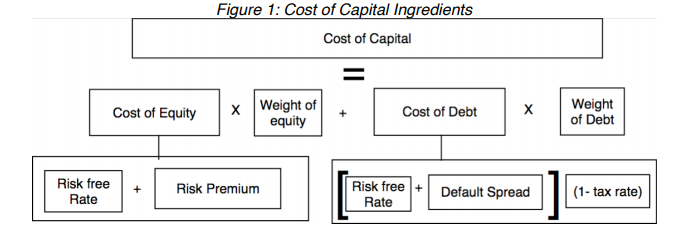

Cost of Capital

Anyway, the Cost of Capital for a company is quite simply the total implied interest on the means of financing it is currently using.

Imagine that a company is running entirely on Debt (It’s not possible – just imagine it). A bank charges them 12% Rate of Interest on the entire Debt. How much should the company earn by way of returns if it employs the Debt into Assets/Business? Clearly, the RoCE should be more than 12%, or the business will go bankrupt.

Debt is fairly straightforward. Most businesses are funded by Equity i.e. Money taken from investors in exchange for a stake in the company. Here, the “interest” isn’t charged every month or year, but it comes in the form of expected dividends + capital appreciation for the investors who lent the Equity capital.

So, the ‘Cost of Capital’ for a company is the Cost of Debt (Interest on Debt) and the Cost of Equity (Minimum Dividends/Capital Appreciation expected by investors) put together in the respective proportion:

(Source)

Cost of Debt

- The Cost of Debt is calculated based on the company’s Credit Rating and the relevant implied market interest rate (Corporate Bond Trading Data can come in handy). Say, if a company is Rated AAA in India, its Cost of Debt is likely to be in the 8.20%-8.50% range, because most Debt instruments issued in India by AAA-rated firms trade in that range.

- If the company itself has issued Debt in the market and it is being actively traded, then you can just take that yield directly.

- If none of this is available, you can simply look at how much the company pays by way of interest on its outstanding Debt and take that instead.

Cost of Equity

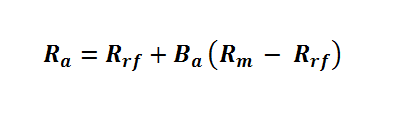

There are several ways to calculate this “Equity interest” or how much the investors in the company expect from an investment in the company .The most famous method is the Capital Asset Pricing Model. The formula goes like this:

Where Ra = Cost of Equity, Rrf = Risk-free Rate, Ba = Beta and Rm = Market Returns.

- In India, the ‘Risk-free Rate’ is the long-term yield on Government bonds. I usually consider the 30-year yield, which is about 7.77% now (Source)

- ‘Beta’ is the comparison of how volatile the stock is compared to the market. Although this involves more calculations, you can easily get this figure from simple google searches. If you are taking this route, consider the ET website, which shows 3-year Beta (Ex: Reliance Industries’ 3-year Beta is 0.96)

- ‘Market Returns’ refers to the returns earned in the broad market indices over the long term (In India, NIFTY or SENSEX). In India, this figure should be closer to 12-13% (NIFTY and SENSEX). I personally use 13% just to be on the safer side.

Cost of Capital Calculation Example: Reliance Industries

Cost of Capital - Reliance Industries.xlsx (39.0 KB)

Economic Value Added

The excess Returns on Capital Employed over Cost of Capital is usually termed as ‘Economic Value Added’. Here’s a recreation of the EVA analysis shown in Pidilite Industries’ latest Annual Report: