This is my first post in valuepickr.i have learnt a lot from this forum but one thing which I lack is how to value a stock.How I know whether I am getting a share at discount or not or when is the right time to sell.I request all stalwart of this forum to please guide in this regard.

You can learn it from here,

In the Valuepkr blog lots of resources are there. All the Best.

This article from Prof Bakshi is a good one https://fundooprofessor.wordpress.com/2011/04/24/vantage_point/ but note that you need to read up on some accounting and valuation books ideally. http://www.amazon.in/Damodaran-Valuation-Security-Investment-Corporate/dp/0471751219 Is a good book although there are others as well e.g by Penman

2 Likes

Hi, here is a link on how to select stocks for long-term which you may find useful.

http://www.tradebrains.in/how-to-select-a-stock-to-invest-in-indian-stock-market/

1 Like

Dear Mr,Kritesh,

thanks for the link…it will give a basic good idea for beginners…

Valuation of a stock requires serious learning efforts and lots of practice. Look at the post below for a link to textbook on valuation.

5 Likes

THIS IS VARY SIMPLE

Thoughts on Valuation by Michael Mauboussin

it is old PDF 1997 but still worth reading

thanks

ashit

2 Likes

Thanks for this article

With the recent run up in Shakti pump how can one say is it the right time to enter or not?apart from dcf model can we value a business on the basis of sales,ebitda,book value?

DCF model valuation and the other methods that you mentioned are completely different in the sense that DCF is a way of finding the absolute value of the company while the others are relative valuation models. Any absolute valuation model is much better because it would not involve bias of market perceived valuations in accounting for the value of the business. Relative valuations are mostly volatile and move along with market perceptions. In expensive markets you see higher relative values being assigned while in cheaper markets you see lower relative valuation for any given company

1 Like

hi all,

can i fetch the historical PE levels from screener.in or from any other website? Please do let me know

1 Like

Hello,

You can use “ratestar.in” to know the historical PE/PB.

You can also get “Historical PE 3Years” and “Historical PE 5Years” from screener.

3 Likes

HELO SIR

I am new in the investing. i search for pe ratio of v2 retail. in screener it is 19. in moeningstar it is 21 and in some other side it is 41. and the eps of last year is 9 and the price is around 260. please guide me thanks

Hello VKP,

I think the reason for the differential PE Ratios is due to exceptional loss which the company incurred during the financial year ending 2017 - 2018. If you look at the Qtrly results filed (Link below), you will find that a sum of 26.61 Cr was incurred as exceptional loss - Some of sites prefer to use normalised EPS and others prefer reported EPS and hence the difference

https://www.bseindia.com/xml-data/corpfiling/AttachHis/229be50d-a191-4745-a918-c022174e056d.pdf

hello sir

I somewhere read that we should invest in those company where the ROE is higher than cost of capital. here i confused in cost of capital. please define and give the example of cost of capital…

thanks.

1 Like

Cost of capital is a theoretical concept with little practical utility for outside investors like you and me. To choose companies, it is better to use tangible return metrics like ROE, ROIC, Margins, Growth Rate etc. and valuation.

2 Likes

I would say RoCE / RoIC should be higher than the Cost of Capital (Or RoE should be higher than the Cost of Equity), as RoE alone can be artificially inflated by the use of excessive Debt. Besides, Debt itself is a form of Capital, so it makes no sense to exclude it from a calculation of Cost of Capital.

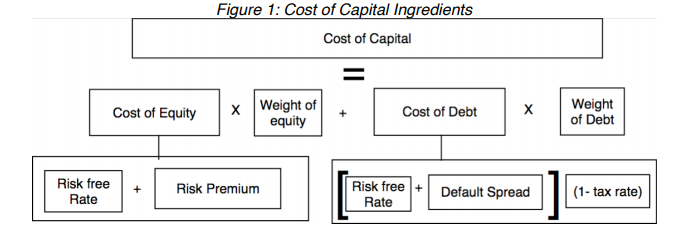

Cost of Capital

Anyway, the Cost of Capital for a company is quite simply the total implied interest on the means of financing it is currently using.

Imagine that a company is running entirely on Debt (It’s not possible – just imagine it). A bank charges them 12% Rate of Interest on the entire Debt. How much should the company earn by way of returns if it employs the Debt into Assets/Business? Clearly, the RoCE should be more than 12%, or the business will go bankrupt.

Debt is fairly straightforward. Most businesses are funded by Equity i.e. Money taken from investors in exchange for a stake in the company. Here, the “interest” isn’t charged every month or year, but it comes in the form of expected dividends + capital appreciation for the investors who lent the Equity capital.

So, the ‘Cost of Capital’ for a company is the Cost of Debt (Interest on Debt) and the Cost of Equity (Minimum Dividends/Capital Appreciation expected by investors) put together in the respective proportion:

(Source)

Cost of Debt

- The Cost of Debt is calculated based on the company’s Credit Rating and the relevant implied market interest rate (Corporate Bond Trading Data can come in handy). Say, if a company is Rated AAA in India, its Cost of Debt is likely to be in the 8.20%-8.50% range, because most Debt instruments issued in India by AAA-rated firms trade in that range.

- If the company itself has issued Debt in the market and it is being actively traded, then you can just take that yield directly.

- If none of this is available, you can simply look at how much the company pays by way of interest on its outstanding Debt and take that instead.

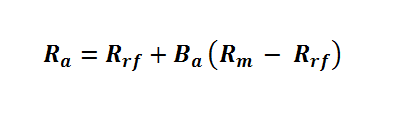

Cost of Equity

There are several ways to calculate this “Equity interest” or how much the investors in the company expect from an investment in the company .The most famous method is the Capital Asset Pricing Model. The formula goes like this:

Where Ra = Cost of Equity, Rrf = Risk-free Rate, Ba = Beta and Rm = Market Returns.

- In India, the ‘Risk-free Rate’ is the long-term yield on Government bonds. I usually consider the 30-year yield, which is about 7.77% now (Source)

- ‘Beta’ is the comparison of how volatile the stock is compared to the market. Although this involves more calculations, you can easily get this figure from simple google searches. If you are taking this route, consider the ET website, which shows 3-year Beta (Ex: Reliance Industries’ 3-year Beta is 0.96)

- ‘Market Returns’ refers to the returns earned in the broad market indices over the long term (In India, NIFTY or SENSEX). In India, this figure should be closer to 12-13% (NIFTY and SENSEX). I personally use 13% just to be on the safer side.

Cost of Capital Calculation Example: Reliance Industries

Cost of Capital - Reliance Industries.xlsx (39.0 KB)

Economic Value Added

The excess Returns on Capital Employed over Cost of Capital is usually termed as ‘Economic Value Added’. Here’s a recreation of the EVA analysis shown in Pidilite Industries’ latest Annual Report:

15 Likes

Thanks @dineshssairam for explaining how to calculate cost of capital with such detail. Very helpful for novices like me.

I tried to calculate the cost of capital for Astral Polytechnik using the above approach. Can you please let me know if this is the right way.

Cost of debt:

Astral has AA- credit rating.

From their latest annual report they have

a) 84 crs term loan in Indian currency at interest rate 7-10%(Im considering 9% in my calculation)

b)35 crs Buyers credit @ interest rate 0.25 - 3% (Im considering 3% in my calculation)

c) 58 crs loans in foreign currency @ interest rate 2-4%(Im considering 4% in my calculation)

A weighted average of the above gives the cost of debt to be 6.2%

Cost of Equity:

Risk free rate = 7.7%

3 yr Beta for Astral = 0.75%

Rm= 13%

Cost of Equity = Rf+ Beta(Rm- Rf)

With above values, cost of equity is 11.7%

From screener,

Equity capital employed =1170Cr

Debt capital employed = 231 cr (as of Q2 2019)

Total capital employed= 1401 Cr

weighted average of cost of capital = 10.78 %

Their return on capital employed is 24%

That gives an EVA of (24 - 10.78)= 13.22

When one compares this with cost of capital of pidilite industries,it is lower as pidilite doesn’t have any debt capital. Probably it is good for companies to have some debt capital if they want to lower the cost of capital. Would like to know your views. Thanks.

3 Likes