You are not exactly their target customer profile . See the presentation this quarter …they target middle aged housewives (45+)and old gals above 65 . People of that age even in our country watch a lot of TV .The Americans have much more pocket money to spend on exotic trinkets than us Indians . Also they can’t get these from street vendors or jewellery shops like one can in India .

They have successful track record for quite long time in this .

Some people will always watch TV in that age group .They are probably going for the website to cater to the below 60 section of their customers who are increasingly becoming net savvy .

6 Likes

Hello All,

I had asked a few questions to management. I got a reply from Mr. Prashantji Saraswat. The questions and answers are below.

- Sunilji reiterated in the last Concall that revenue will grow at 15% to 17% cagr over the medium term. Can I assume that revenue could grow at 15% at least over the next 5 years?

Yes, based on Sunilji’s guidance, you can reasonably expect mid-teens revenue growth over the next five years.

- Sunilji also said that once the customer acquisition is done, the leverage starts in the business. He pointed out that 200 bps of operating leverage is possible this year. Can we say that as we keep growing in Germany, UK & also organically in the US, our EBITDA margin can reach 12-15% levels like it did in 2021? Or that was just one off due to Covid & we as investors should accept the new reality of sub 10% EBITDA margin?

Double-digit EBITDA margins are achievable, especially once Germany becomes profitable. While we don’t give specific EBITDA guidance, margins of 14% to 15% are possible in the medium to long term as we scale in Germany, the UK, and the US. The elevated margins in 2021 were partly due to unique factors like COVID, but strong operating leverage supports long-term improvement.

- Can we assume that depreciation will not increase substantially? As we saw even the expansion in Germany did not need too much capex & our depreciation went to 100Cr levels. Can I assume that the depreciation even if we expand into other geographies will not grow beyond 100 Cr?

Depreciation won’t increase significantly. Our asset-light model means minimal capex, even with expansion. Depreciation might rise only if we pursue acquisitions or enter new geographies, but neither is on the horizon for now.

- Same with Debt . Because we are an asset light business, can we safely assume that debt will stay low & the interest cost will not exceed 15 Cr per annum?

Yes, our debt levels will stay low because of our cash-generative, asset-light model. Interest costs should also remain around current levels.

- The average revenue per item sold from tv channels is $39 but from the web is ~30. Why is it so? Does it mean gross margin is lower in the e sales?

The difference in ASP ($39 on TV vs. ~$30 on digital) reflects buying behaviour, not margins. In fact, our gross margins are slightly better on digital. While the cost of manufacturing remains constant across channels, digital sales tend to achieve higher gross margins due to customer behaviour driven targeted offers and campaigns which are more exclusive or tailored to their needs. However, a broader assortment of higher-margin products allows for better price realization compared to the time-sensitive, promotion-heavy nature of TV sales.

- Lab grown diamonds? Do we manufacture them? If yes, what do we think of the future of lab grown diamond jewellery? Can this also contribute to our margins & bottomline in the future significantly?

We don’t manufacture lab-grown diamonds, we source them. They are a small part of our business. While the category will grow, we don’t expect it to significantly impact our revenue or profit as prices are declining, and our core customers prefer fashion and gemstone jewellery.

- We are thinking of expanding to Japan. Why not India? I am seeing other fashion jewellers in India. They are doing absolutely fantastic. Even though their model is store based sales, I think there is a big gap in the TV & digital space in India. The Indian fashion jewellery market is booming.

Right now, we are not planning to enter the Indian market. While the market is growing, our focus is on geographies where we already operate and scale them further. Expanding into Japan aligns better with our strategy and business model, but that is not in our consideration in the foreseeable future.

Depending on the above, I did some rough back of the envelope modeling for the next 5 years. It seems even at 12% EBITDA margin, the returns could be handsome over the next 5 years from the current price. If the margins reach 15% & above, it’s bonus. Please do your own research & post it here for everyone’s benefit if you can.

Disc: Invested & biased.

26 Likes

thanks for sharing this.

I think the 200bps was guided for GMs.

Germany turning profitable, 2 acquisitions contributing, decreasing interest rates, improved sentiments in US with Trump back at the helm - I think all these factors will auger well for VGL. In general, I feel management has been conservative now particularly after getting hurt with high guidance on back of COVID high base.

2 Likes

Thanks for sharing Parth. I agree with all the above. The only risks are it’s a highly competitive industry. Undercutting & high inventory turnover is the game. Also, tariffs might hurt a bit. Let’s see how the story unfolds.

Disc: Invested & definitely biased.

Well-known investor Nalanda India Fund sold 27,00,000 shares. This is the reason for correction! Reducing stake since few qtrs.

1 Like

Achieving highest-ever monthly sales from India.

source: Company’s Twitter account

1 Like

Could you please quote the source? The management had said that India is not a focus market for them in the last few concalls.

So this should be export from India. They manufacture in India and export. So it should be highest exports from India.

1 Like

H2 should see significant operating leverage play out for Vaibhav Global Limited if one has followed management commentary closely.

If they are able to grow revenues by 10-15% YoY in H2 (INR depreciation should help additionally) in line with their growth in H1, then there should be significant operating leverage in H2 from two line items - employee costs and content & broadcasting costs.

Let’s look at the nos in more detail:

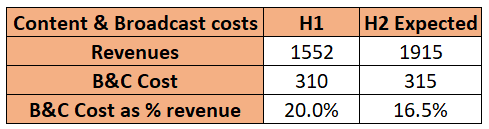

Content and broadcasting costs: Management guidance is that in FY25 this line item will represent 18% of FY25 revenues. Assuming FY25 revenues to be INR 3465 Cr (14% YoY growth; They have constantly guided for mid teens growth), the total B&C cost for the year should be around INR 624Cr. Now H1 B&C expenses were INR 310Cr (you can find this in results’ notes to accounts). Which implies H2 B&C expenses will be in the range of INR 315Cr. Now B&C costs remaining almost flat between H1 and H2 while revenues in H2 increase significantly over H1 (VGL is an H2 heavy business due to the festive season in Q3), can cause significant operating leverage between the two halves. As much as 3.5% difference in EBITDAM as shown below

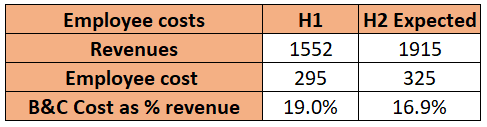

Now let’s look at another line item for leverage - employee costs: Employee costs in H1 were INR 295Cr. Let’s generously assume that employee costs will increase by 10% in H2 over H1 (temporary staffing to handle Q3 bump etc.), then we have an employee cost of INR 325Cr in H2 on much higher revenues. For this line item as well, there should be significant operating leverage in H2 vs H1. Potentially as much as 2.1% EBITDAM as shown below

Thus, if VGL delivers 14% YoY growth in H2, then there is a possibility of as much as 5.6% operating leverage in H2 vs H1. H1 EBITDAM was 8.7% (including other income). Hence H2 EBITDAM can be as high as 14.3%.

But this is obviously the best case scenario assuming a very good YoY revenue growth coupled with realization of the entire theoretical operating leverage without any slippages and with no other cost item escalations. Its unlikely that everything plays out quite like this in H2. So let’s model different growth and operating leverage scenarios and see how EBITDA and PAT could move in H2 under various scenarios.

Let’s assume 3 FY25 revenue growth scenarios - 10%, 12% and 14% and 7 levels of operating leverage in H2 vs H1 ranging from 250-550 bps.

H2 EBITDA can vary from INR 201 Cr to INR 272 Cr depending on which scenario plays out. Mind you even the lowest case scenario is a 30% YoY EBITDA growth on H2 FY24.

Similarly modelling PAT assuming 60Cr depreciation + interest in H2 FY25 and a 30% tax rate.

H2 PAT can range from INR 99Cr to INR 148Cr. Mind you even the lowest case PAT is a 45% YoY growth from H2FY24 PAT levels.

Of course businesses are not done on Excel sheets like this. There can be many uncertain outcomes which cannot be modelled. However I believe in varying revenue growth and operating leverage figures by such a wide margin, we should be able to catch most of the real life scenarios playing out. Therefore, the bottomline conclusion for me is that even in a pessimistic scenario, the business seems to be on course to deliver robust PAT growth in H2 YoY.

Its also evident that operating leverage should continue to play out over the next several years here as long as revenue grows in double digits. Management is guiding for mid teens revenue growth over the medium term. As an investor, there is no option but to trust management guidance to an extent. But its prudent to overlay uncertainties on top of the guidance. So I will not model anything more than double digit revenue growth for the medium term till the business shows 6-8 Qs of straight mid teens revenue growth execution.

The stock has broken down from its support levels of 267. But in a bear market (Yes, in a span of 3 weeks we are in one), looking at technical levels is futile. Buying has to happen on fundamental number based conviction.

Disc: Invested. Please do your own due diligence and don’t blindly trust my analysis. I could very well be wrong.

36 Likes

Good results. Revenue growth of 10%, EBITDA growth of 18% and PAT growth of 35%. Leverage played out quite well in employee costs and C&B costs but was countered partially by a QoQ decrease in gross margins.

5 Likes

Good nos. considering the election event during the quarter…

2 Likes

Not the numbers that would make market go crazy on this yet. PAT growth seems higher because last year they had exceptional item and higher tax expense. It has to show sight of mid teens margins in some quarter especially seasonally strong one.

4 Likes

Why wud they revise the FY25 revenue guidance downward?

1 Like

Vaibhav Global Lowers FY25 Revenue Outlook

Management now projects a 12% revenue growth for FY25, citing weak consumer sentiment in the UK and Europe. From FY26 onward, they expect growth to return to the low teens, with a stronger focus on operating efficiency.

Note: The company had previously guided for 14%–17% growth in FY25.

3 Likes

Right. However, even if we assume a tax rate of 27% (a reasonable median average) for this quarter, the profit has increased by ₹20 crore on a QoQ basis. There is some visible upside, and Vijay Kedia Ji has been invested for a long time, even before 2022, with his stake increasing marginally.

P.S. - Not recommendation to buy/sell. My views can be biased, Invested.

2 Likes

after COVID, they have hardly been meeting their own guidance numbers.

Hi nirvana - If the growth rate is 12% around isnt it that it can reduce the probability of pe expansion? & Also it can limit the upside if you can share your thoughts on this

Q2 what are you thoughts after listening to conference call

Thanks

As I have mentioned above, 10% revenue growth is enough for them to deliver handsome operating leverage. PE multiple is not in our hands, but sustained 25-30% PAT growth over several quarters should mean a 30x+ PE should sustain IMO. The real question is about their ability to deliver this double digit revenue growth via volume growth and not ASP increases.

A few thoughts on Q3 results and concall commentary

-

Drop in revenue guidance for FY25 and FY26 after holding on to mid teens guidance till Q2 concall, was a bit of a bummer. Wasn’t expecting a change in guidance in the span of 1Q. However, even if they achieve this guidance, there is enough scope of leverage to play out. Management mentioned in the call today that operating losses from IW + Germany amounted to 250 bps in 9M FY25. From FY26, most of this delta should flow straight to EBITDA as both operations have broken even.

-

Reduction in gross margins in Q3 was another surprise. Without the drop in gross margins, this would have been a 13% EBITDAM quarter and we would be having a completely different conversion with all kinds of bullish takes flowing in from all corners. The fact that gross margins dropped 200 bps due to higher sales of LGD and other high-value items needs to be tracked closely for future quarters. This low a gross margin print last happened in FY23 when inflation was running rampant and people were buying high value jewellery as an inflation hedge. If this drop in GMs is transient then there are no issues, but if this is structural then some of the operating leverage gains in EBITDAM will be reversed due to lower GMs. Hope VGL can optimise the LGD supply chain and squeeze back the lost gross margin in subsequent quarters. On gross margins they have time and again proven their mettle so its possible that they claw back gross margins on LGD as a category.

-

Management is guiding for double digit volume growth. I feel that’s overambitious guidance - their history suggests this happens rarely. However, with INR depreciation and slight ASP increases, even a 6% YoY volume growth can enable a 12-13% revenue growth. Their volume growth print this Q was only 1.7%. This was the first full Q with MS and IW in the base. Management said the muted volume growth was due to a spike in high value sales items due to consumer demand pull. Have to see how this plays out over the next few quarters. Higher sales volumes of lower value items will drive volumes as well as higher gross margins

I was expecting Q3 FY25 to be the moving quarter where finally the company was able to deliver 11-12% revenue growth and 12.5-13% EBITDA margins. But those numbers now seem to have gotten pushed out by a couple of quarters more. The broad investor skepticism around VGL is understandable. Since Covid they have struggled to meet their guidance a few times and due to a heavy investment cycle over the last 3Ys (Germany entry + MS/IW acquisitions + better channel positioning in USA) their return ratios have been depressed for a while.

However its absolutely evident that if double digit revenue growth happens on a sustained basis then operating leverage will keep playing out here. So volume led topline growth is the most important thing to track here. Q4 should be very good on a YoY basis. I will be very surprised if 100% YoY PAT growth in Q4 does not happen because of the low base.

Disc: I had a very aggressive position size here anticipating the start of the turnaround from this Q. Have moderated position size post results. Remain invested as I believe the thesis can still play out as envisaged. May exit or increase position size without informing. Please do your own due diligence.

30 Likes