Dec is the best quarter for them, I think investors will wait for one more quarter to see growth is real, last year after a good Dec qtr, next two three quarters were not so good.

3 Likes

Next quarter can be good seeing US economy booming, germany economy might get bump up with elections due there and UK economy seems to be getting better. I also expect decent growth in bottom line as base is low, UK & Germany operations breaking even.

Disc: Biased and invested

2 Likes

If we see the revenue trend for Q3, Q4 and Q1…it is Q3>Q4>Q1. This has happened for 3 yrs as can be seen from screener. Further, the mgmt’s comment in Q3 call was…“Looking ahead, we remain mindful of macroeconomic trends, particularly the muted consumer sentiments in UK and Europe”…Germany continues to be in recession and when would it come out is difficult to predict. My sense is the business continues to face competitive headwinds and growth could be slow and small. Valuations seems to be reasonable, but not very very cheap, so margin of safety is not too high.

Disc: Invested

3 Likes

Vijay Kedia Is A Marquee Investor In This Company: All You Need To Know About Its KYC Rating

Not sure if this is how your introduce a company - that Vijay Kedia has invested

1 Like

What is impact of tarrifs on company ? Anyone has some knowledge about it?

1 Like

I was searching whether the management has addressed this question. In the Q2FY25 earnings call, the management said that they are not worried about tariffs since the company is the lowest cost producer. You can read the exact statement below from the company. We would have to wait for a couple of quarters to see how does the company actually perform as these tariffs are implemented.

We believe that we are the lowest cost producer and the tariffs would impact equally everybody. So, we don’t foresee us getting impacted any adverse. In fact, with our gross margin of 62% plus our cost will be lower than other competitors because their gross margins are lower. So, it will be at advantage if at all the tariff across the board comes into picture.

In fact they were asked a similar question in the earnings call for Q2FY19. And you can read their response below, it was pretty much the same.

This may be seen as a threat by other retailers, but we look it as an opportunity, because if the tariffs will go up the cost will increase for all retailers. For us our gross margins are much higher than anyone else so for us the impact will be lower than anybody else. And secondly, we are pretty agile in terms of sourcing the product from China or Thailand or Indonesia or India. We have our own operations in all these four countries whereas other retailers do not have their own operation they depend on vendors. So, for them to be agile will not be as easy as it is for us. So, competitively it will be better for us.

5 Likes

VAIBHAV GLOBAL (Market Cap- 3700cr) - Opportunity for some vs Opportunity cost for some !!!

Let’s put it straight, while market conditions may not be highly lucrative right now, the opportunity remains decent for long-term. This business is not suited for short-term, YOY analysis due to the inherent volatility in profitability. However, over a 3–4 year period, profitability swings.( Same like Hatsun Agro over long period profitability grows expanding regions, gaining little market share etc.. )

Little Brief on Evolution and Market Focus

The company’s evolution since 2008—from B2B to B2C. Expanding first into the US, then the UK, and now Germany, the focus has been on markets with high per capita income and next is Japan. Majority of the revenues comes from TV as of now but moving towards digital 50% over coming years is a necessary step for future growth.

Main Trigger - Germany Profitability going forward

The losses from Germany are now behind them, with operations there reaching break-even. This could directly add ₹25 crore to PBT next year, improving the outlook (base case PAT: ₹180-200 crore FY26). RISK: Remains slowdown in US consumer spending and tariff impacts on India and other economies, which is a real concern for the business.

Slowdown and How will Vaibhav overcome this?

Difficult to overcome macro consumer slowdown, there will be pain. If anybody thinks it’s not there, they are in for a ride here. But some little factors like below:

1] High gross margins and

2] Low price point i,e 30$ ASP**

3] Zero Debt

In this, competitors may find more difficult to navigate than for Vaibhav, just a thought. Anyways, these are the times, best of the management are tested, some bounce back very strong some don’t. That’s the part of probabilistic investing !!!

To Conclude, In uncertain times, strong companies often emerge more resilient. If one can have conviction in the business and management, aligning on asset allocation will help navigate the volatility. Without that conviction, however, it’s best to avoid random bets thinking of short term and QOQ analysis

- For Management to comment its very difficult for them to predict consumer demand for YoY !! So Only Patience and Long term horizon will help. (Global slowdown is the risk, How long term is the question, you want hold this business, you need to assess yourself.)

Hope it adds little perspective. I can be wrong, so DYOD.

6 Likes

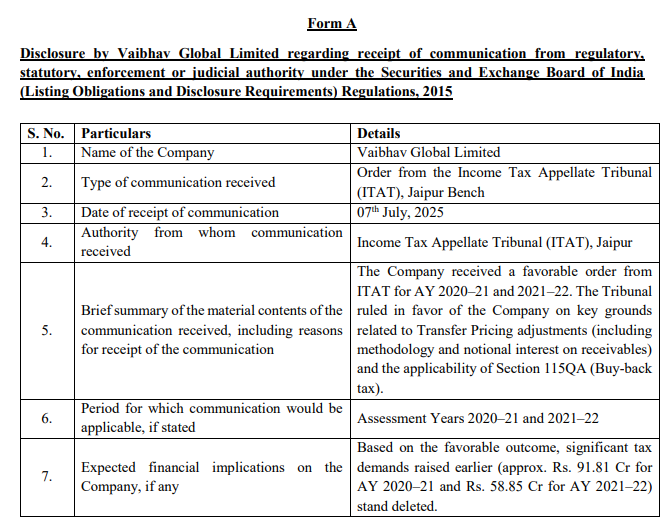

The IT Tribunal ruled in favor of company. As a result of this favorable outcome, significant tax demands raised earlier, approximately Rs. 91.81 crore for AY 2020-21 and Rs. 58.85 crore for AY 2021-22, have been deleted.

8 Likes

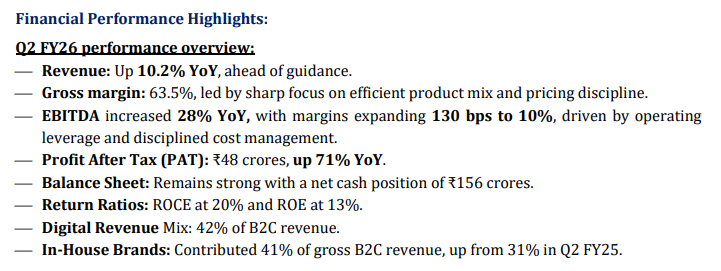

- Good results by vaibhav global. Revenue grew by ~8%, PBT by 22%. Largely due to margin improvement. Company pre-shipped inventory ahead of the tariff rollout, ensuring smooth operations in coming months.

- UK showing healthy growth of 12% YOY and 1.5 QOQ. Also, rest of the world 7.3% YOY and 22.5% QOQ

- Europe (excl. UK) has shown biggest improvement with EBIT margins turned YOY from (15%) to 15%. In my view, large part of this is due to Forex gain as EUR appreciated by 7% this quarter, further Germany was in losses in Q1 but achieved EBITDA breakeven in July.

- Management has lowered revenue guidance from 8-12% to 7-9% due to tariff

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/6eee97b4-d48d-4508-be09-178d62cff20d.pdf

7 Likes