Can anyone please throw some light on how to comprehend the valuation of the company. I understand that the seasonality angle, the deleveraging part and the growth. I also had the opportunity to visit the plant and meet the management recently and found the management quite clear in where they aspire the company to be. I also have no doubt in their execution capabilities looking at their post GFC revival story. It’s just that I am not able to understand how to value a company with this current valuation. Assumption: With a topline growth of 25% growth and 12% ebitda margins. Would the company still be just to be valued at this valuation. Kindly share your thoughts.

some notes posted on twitter from plant visit:

https://x.com/abhishekcjain/status/1746581934707499344?s=20

Model the FY25 revenue + margin. Model the EBITDA. The PAT. The acquisitions.

Disc: Invested, biased, might sell out if i can find a better opportunity.

11 Likes

Margins mentioned are PAT margins or operation margins?

So Japan and UK are Into theoretical Recession, since Vaibhav Global Operates In UK on The Retail Side, and from my knowledge if economies Fall into recession Govt Increases Rate of Lending that leads To less money in Hands of People, Hence less spending By People, Specially on Fashion Items People cut more of their Spending , so can anyone guide me how much will this Impact Vaibhav Global. If not Then also, please explain Why you feel that vaibhav will be resilient to this??

1 Like

earlier management has said that due to such economic situation, people tend to move from brands to low cost value provider like Vaibhav.

3 Likes

As gold reaches top… I think vaibhav global products has huge potential even in India going forward as gold is touching all time high…

Please comment / correct if this is not correct assumption

4 Likes

It’s a really good approach. Gold price is going to go more high. But it will take 2-3 years more for Vaibhav global to get into India.

Vaibhav global is a jewelry business but it is unlike any other business. It has a fully vertical supply chain and produces and sources products and sells them in US,UK and Germany through digital media and TV. It follows the Zara model and has a strong focus on Gross margins being 60%+

Anyways

Let’s get to the thesis

Thesis

The management is really good and I remember them mentioning they take pride in meeting and succeeding their guidance every single time except post covid. The management has guided for 14-17% growth for the next FY25 with strong operating leverage I have assumed the higher side to see the best possible scenario, I would suggest taking the lower end too in a different model to know the full spectrum of possibilities. However, they acquired two new companies and are hopeful of getting 40-45 million(which is 17 million rn) If that happens, they can surely go past their guidance

EBITDA

EBITDA and sales are all there is to track here. EBITDA was 12% (ended up as 9.5% adding other incomes)

barring the losses of Germany. Germany is expected to break even H2FY25 and hence that drag will go away!

I have been conservative with the margins and only factored in 1.5% reduction of drag from Germany and no improvement in environment of UK and US and acquisition margins to stay the same(highly unlikely)

Management said 15-18% margins are possible in the long term so there is huge growth ahead!

Other income

Other incomes is 0.5% of revenue to factor a 1.5% increase in margins each year

Interest and depreciation shouldn’t move much except a new acquisition. But that should boost revenue as well!

Antithesis

-

Fragile state of western economy, especially the UK has caused a lot of problems before and the business is prone to deleverage as well!

-

Failure of expected break even of Germany will spoil the improvement of margin

Final thoughts

I think the business is really good and is quite unique. The ROCE is to improve which can increase the bandwidth of exit multiples

Moreover, the TAM of the business is really high as they haven’t penetrated much in their countries(for example US is 15 billion dollars and Vaibhav has 3% share)

And they are open to stating business in Japan and India after Germany is steady and profitable

A lot of consolidation

At support

Let’s see how it goes

I think earnings will catch up a bit for valuation comfort before prices go

But it’s anyone’s guess

11 Likes

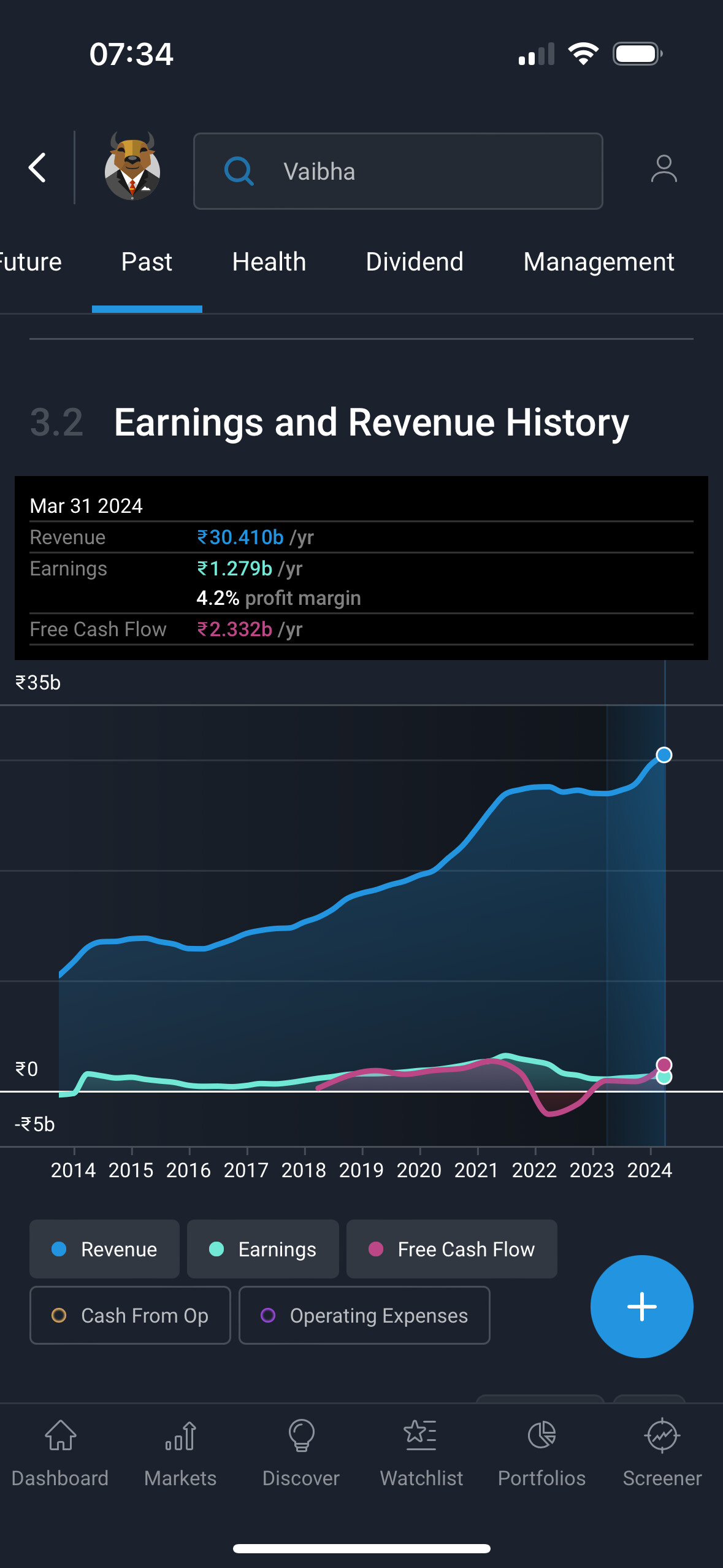

Going by numbers shown in screener.in, here is what I see:

10 year Compounded Sales Growth: 9 %

10 year Compounded Profit Growth: -1 % (negative)

10 year Stock Price CAGR: 6 %

10 year is a good time to evaluate a business.

Considering Sales and profit numbers, Why are we (including me) hoping this company can turn around ? Or is this pure potential business on the cusp of capturing newer geography or newer segments of business ? Geography-wise yes, I know VGL has plans to get into Japan, India. But what potential if it is not able to perform in US and UK markets ? Newer segments, yes, they are trying to get percentage of non-jewellery business significantly, but again, I doubt if it is anything game changer. I would love to get it wrong, but does not look so at the outset.

Also we keep hearing from Management that their priority is about High margins. Here again we see OPM numbers for last 2 fy as 7% and 9%. Maximum OPM number is seen during FY2021 at 15%.

Again am I reading something different ? What margins Management is referring to ? If the subscription costs are very high, which company cannot control, then what is the point ?

Also, with these sales and profit numbers, how come we see 10 year Return on Equity as 19% ?

4 Likes

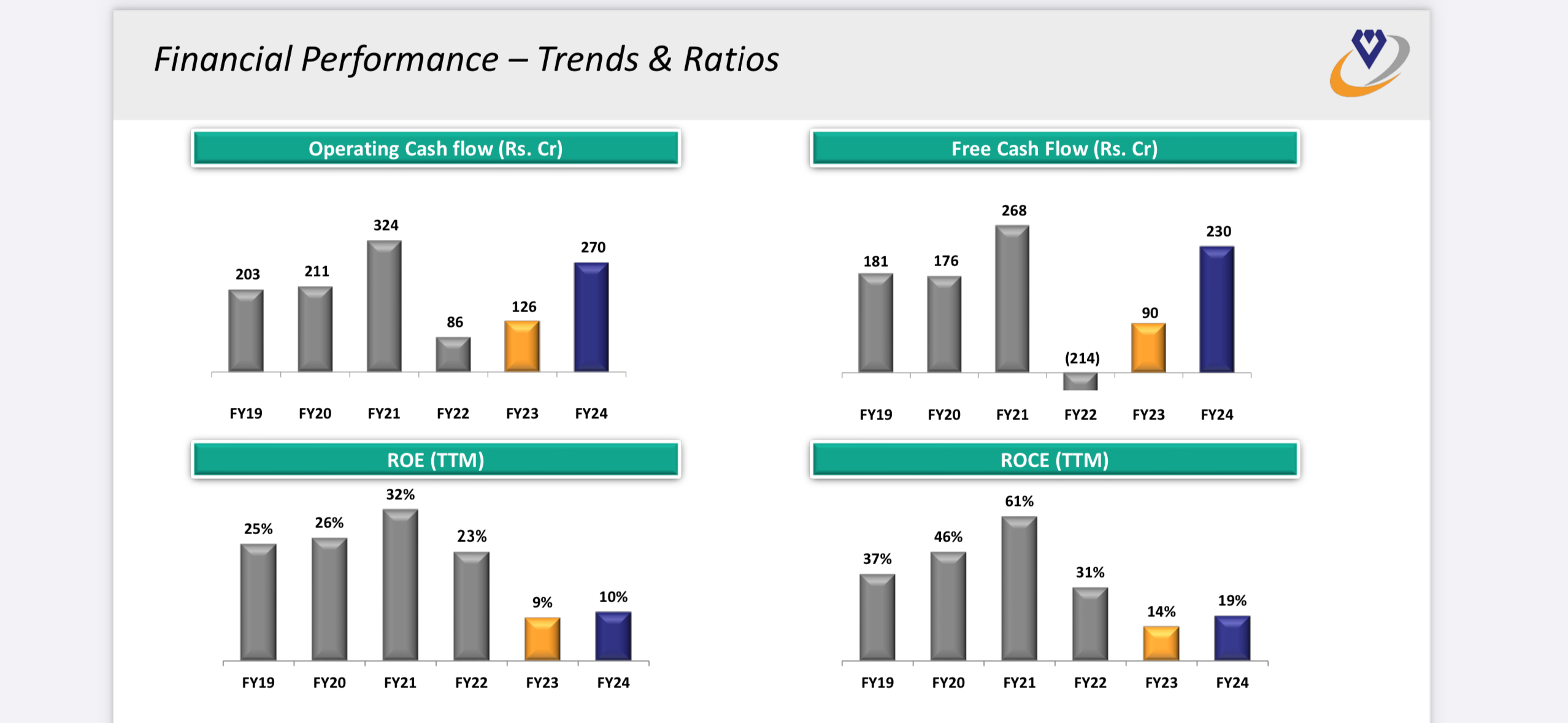

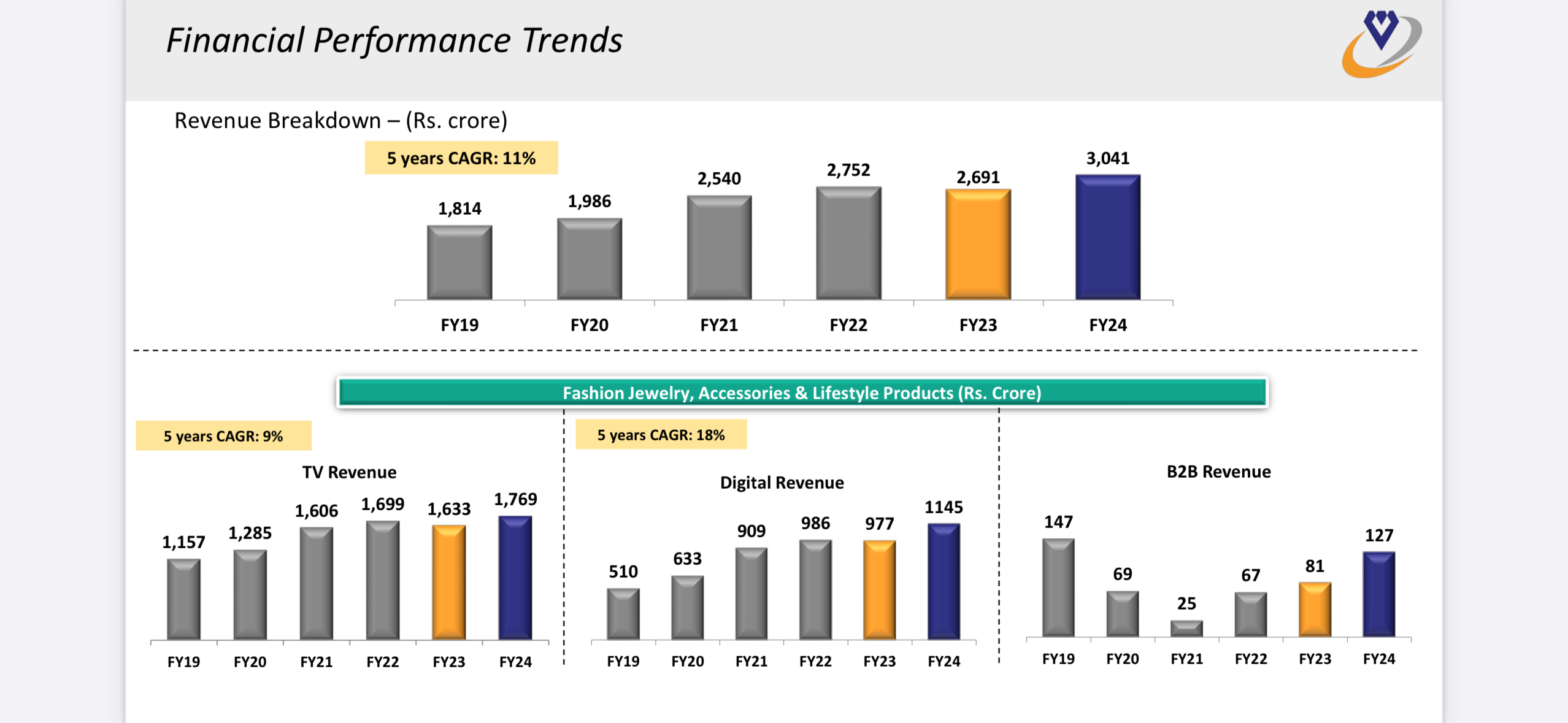

I think the profitability since 2021 is skewed because of higher CAPEX and acquisitions in Germany and UK. If you ignore those, the underlying core business of UK and US are actually growing in revenue and profits. Once the new acquisitions become fully scaled in a few years’ time, I think the margins will go back to what they were earlier (around 10% free cash flow margin)

Requesting you to please verify its cashflow. Cashflow from Operation has mutiplied more than 3X in same 10 years period.Its an internet company ,large amount spend on Softwear and Broadcasting Right acquisition .Same comes back as depriciation line item in Screener P&L and in FY24 its around 93 cr and increasing rapidly YoY basis.This line item is increasing as management is keen to build new studio , want to reach more home on TV-Home basis , investment in germany , upgrading channel position on various TV network, investment on OTA home reach. Having said that, Operating Margin surely has got weak over the years though Gross Margin consistently kept above 60% but content creation/broadcasting charges,freight charges and Packaging charges is increasing at rapid rate.

3 Likes

Vaibhav Global Q1 FY25 Concall notes (posting only key takeaways from my POV)

-

Maintains guidance for 14-17% revenue growth in FY25. The range is due to uncertainties due to US elections, else they’d have been confident guiding for 17%

-

Content and broadcasting cost was 20% of topline in Q1, expects to finish the year at 18% of topline. This is a 1.5% YoY growth for the line item. Investments here being made for ramping up their newly acquired online businesses of Ideal World and Mindful Souls as well as the new territory of Germany. They have also spent some amount in improving TV positioning in USA. This line item as % topline has increased from 12.5% in FY20 to around 18% in FY25E. One hopes that a lot of this is leverage and the ratio was settle below 15% once the new businesses reach steady-state. Looks like they are targeting higher growth (mid teens guidance for medium term) via higher investments in content and broadcasting with some leverage.

-

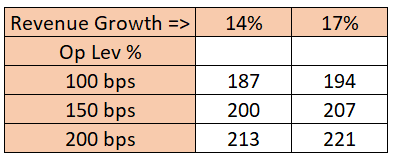

Overall expect to deliver 150-200bps of operating leverage in FY25. Expects 200bps GM expansion due to better product mix, 100bps expansion from employee costs line item and possibly another 50bps from other line items such as travel expenses and freight. There will be a 150bps negative leverage due to B&C costs as discussed above, so net/net there’s a possibility of 150-200bps EBITDAM expansion YoY

If management indeed is able to deliver 15% revenue growth and 200bps EBITDAM improvement over the year, PAT here can comfortably cross 200Cr. Here’s how I see PAT playing out for various combinations of growth and leverage. I have assumed 20cr Other Income and 25% tax rate.

Depending on which scenario plays out, there could be a 50-75% YoY PAT growth and the stock is likely trading between 24-29x FY25 PAT. If the upper end of the PAT assumptions plays out, I won’t be surprised to see the stock trading at 8000Cr MCap.

Chart wise, 273 seems like a strong support zone. I don’t expect the stock to test that support unless there is panic about a US recession. From what I know, recessionary conditions on ground normally top out well before a recession officially shows up in GDP nos. So the worst in terms of consumer sentiment for the business may actually be behind them and that seems to be what management is also indicating. However, Western economies aren’t in the best of health and adverse risks remain which need to be monitored.

Disc: Invested.

32 Likes

Thanks for detailed and valuable note. Would love to hear your view, which is much appreciated, on the below point:

Expected max. PE 30x of FY25 PAT: How market cap might be ~8K Cr. for a max profit of ~220 Cr.?

2 Likes

The 24-29x PE is on current MCap if you consider the FY25 PAT range of 187-221Cr. At FY25 exit, market may value this at 35-36x PE on 220Cr earnings leading to an ~8000Cr MCap. Alternatively, on Price to sales, the stock has traded at 2.2x median multiples over the last 5Ys. On an FY25 expected revenue of ~3500Cr, a 2.2x multiple is again close to 8000Cr MCap.

The expected MCap is completely speculative from my side, it depends on market conditions prevailing at the time and many other factors. We can just track earnings and hope to project them with some accuracy.

12 Likes

Vaibhav Global Q1 FY25 Earnings Analysis: Key takeaways!!

Business Outlook:

- Revenue grew 15% YoY to Rs. 756 crores, driven by digital growth and recent acquisitions

- Gross margin expanded significantly to 66.1% from 61.2% last year

- EBITDA margin contracted to 8.7% from 10% due to higher marketing and broadcasting costs

- Management reiterated FY25 revenue growth guidance of 14-17% with operating leverage

- Mid-teens revenue growth projected for future periods with continued operating leverage

Strategic Initiatives:

- Focusing on “4R Strategy” - Widening Reach, New Customer Registration, Customer Retention, and Repeat Purchases

- Investing in digital marketing and better TV channel positions to drive growth

- Integrating recent acquisitions Ideal World and Mindful Souls

- Leveraging VGL’s supply chain to improve profitability of acquired businesses

- Exited low-margin apparel manufacturing business

Trends and Themes:

- Shift towards digital channels - now 40% of revenue and 45% of volume

- Budget Pay EMI option contributing 38% of B2C revenue

- Expanding customer base - unique customers up 37% YoY to 636,000

- Focus on sustainability - using renewable energy, rainwater harvesting

Industry Tailwinds:

- Growth in online retail industry, especially in the US

- Recovery expected in UK and German economies as interest rates moderate

Industry Headwinds:

- Cautious consumer sentiment in UK due to economic uncertainty

- Overall jewelry market seeing negative growth in US

- Election cycle in US may impact viewership

Analyst Concerns and Management Response:

- Rising content and broadcasting costs (20% of revenue in Q1)

Management: Expects to moderate to 18% for full year, sees operating leverage ahead - Slow growth in core US/UK markets

Management: Expects improvement as macro conditions stabilize, mid-teens growth sustainable

Competitive Landscape:

The company positions itself as vertically integrated with quick turnaround times

Guidance and Outlook:

- FY25 revenue growth of 14-17% with operating leverage

- 200 bps gross margin expansion expected YoY

- Germany to be profitable at operating level by H2 FY25

- Mid-teens revenue growth expected in future periods

Capital Allocation Strategy:

- Declared interim dividend of Rs 1.5 per share (90% payout)

- Focused on organic growth and integrating recent acquisitions

- No immediate plans for further geographic expansion

Opportunities & Risks:

Opportunities:

- Further digital penetration and customer migration from TV to digital

- Geographic expansion (e.g. Japan in 3+ years)

- Margin improvement as acquisitions integrate

Risks:

- Macro uncertainties in key markets

- Rising customer acquisition costs

- Integration challenges with acquisitions

Customer Sentiment:

- Strong in US, cautious in UK, improving in Germany

- Overall retention rate of 40%, repeat purchases of 24 pieces per annum

Top 3 Takeaways:

- Digital growth and acquisition integration driving revenue, but near-term margin pressure

- Management confident in mid-teens growth sustainability with operating leverage

- Focus on customer acquisition and retention through omnichannel strategy

7 Likes

Consumer sentiment and GDP growth (in US at least) has actually been robust going by news reports so why is VGL unable to capitalise on that sentiment? If mgmt couldn’t deliver results in such a robust macro economic scenario where GDP grew despite all time high rates, how will the mgmt deliver results when Fed starts cutting rates or a recession hits US ? Price might be right to enter at this point but can’t trust the mgmt which doesn’t deliver results in good times too! That might be indicative of a flawed business model.

6 Likes

Can someone explain me how is US consumer different from Indian consumer, like I never see TV channels like Naaptol … Also what is the cost of having channel in US ?

Their website might have some organic traffic but do we know the ration of website vs tv-channel traffic. Like what traffic will remain on Website if no users sees TV channel?

So starting of operating leverage