Margin expansion happening clearly. Rerating candidate for sure! imagine what will happen when new capacity kicks and volume growth happens ![]()

3 Likes

I think ED case which was reopened, and continuous selling from his brother will be a hurdle for rerating.

4 Likes

Hey Ishmohit, My queries-

- Why is the company including the ‘other income’ while calculating Ebitda? It has done the same for every quarter.

- Also, Is the company right in including ‘other income’ for caluclation of Ebidta/Ton?

2 Likes

Ishmohit, How do you read the fact there is no bulk/block deal here? Unless I am misreading, the selling goes straight to the public.

Just my two cents:-

- Open Market selling, yes shares are being sold openly in the market. Many times, there is no block deal.Plenty of time institutions also buy openly from the markets. However, this is not the real risk and is more to do with the voting nature of Mr. Market

2.Real risk lies in LRPC strands, and capacity addition by Jindal. Will be interesting to see if they can hold their margins or not. That is what I am looking at, given the management is guiding to increase VAP as a % mix.

+Another point to note is Bekaert which is the world market leader in steel wire ropes is headquartered out of Europe, Brussels. Might face a lot of challenges with procuring steel for manufacturing steel wire ropes, that can create a market vacuum for both Usha M and Bharat Wires to exploit.

Disc: Invested since 60s, not a reco to buy or sell.

15 Likes

I think we make a lot out of promoter selling… The thing to know here is that the promoter running the business is not selling his shares. Its being sold by his cousin who is saddled with his stake and is not running the business. He may have his reasons for selling, which we might not be aware of.

Stake sale by non managing promoters and even institutions sometimes is not such a bad thing. We have had some recent and not so recent experiences with big sales in stakes. In the past, there were two tranches of big sale by institutions in Laurus when price remained under pressure for a few days post this sale and then resumed its uptrend in response to earnings. Recent example was in case of HBL Power where Banyan tree which used to hold nearly 10% stake kept selling and as recently as a few days ago, there was clear cut supply at price of 80, before the order news came about. Once the positive news came about, stock went up swiftly and now seems to have settled at a higher level of 90 plus.

Usha martin chart has an interesting pattern currently. Its stock price broke out above 140 on 25 July with huge volumes thus breaking out of a cup and handle pattern. (neckline of the pattern is marked in blue dotted horizontal line. ) Once that happened, stock price went up to 157-158 and corrected, and is now doing a retest of the breakout zone by consolidating between 132-142, and a brief attempt was made a couple of days ago but stock again corrected from 150 levels to again hover in and around 140.

In fact today it has formed an interesting candlestick pattern called homing pigeon candlestick. It consists of two candlesticks wherein first candle is a dark bearish candlestick where stock price opens higher and by end of trading, closes well below that near the lows of the day. On the second day (today) stock price opens higher and suffers selling pressure and closes lower than the open, but higher than previous day’s close. The body (area between open and close) of second candle is completely within the body of first candle. Usually this is considered as a trend reversing candle stick (in this case, reversing from a short term correction, to possibly go up in next few trading sessions . Current example is not an example of classic homing pigeon, which usually occurs at fag end of a bearish trend. ) Proof of the pudding will remain in the eating. ![]() Next few days will tell us how things go from here. (PS… just noticed that we have another example of a classic homing pigeon candlestick on this very chart on 17 June. On 16, there was a big bearish candlestick at the fag end of a major correction. On next day we have a homing pigeon candlestick pattern which had a bottom perched exactly on 200 dema at 99-100, shown in green line. After that there was a very good rally from 100 to swing highs of 157.

Next few days will tell us how things go from here. (PS… just noticed that we have another example of a classic homing pigeon candlestick on this very chart on 17 June. On 16, there was a big bearish candlestick at the fag end of a major correction. On next day we have a homing pigeon candlestick pattern which had a bottom perched exactly on 200 dema at 99-100, shown in green line. After that there was a very good rally from 100 to swing highs of 157.

If the cup and handle pattern plays out, target of pattern could be around 180.

disc: invested since a long time as disclosed before.

13 Likes

Thanks @hitesh2710 @Worldlywiseinvestors

Good to hear your perspective. I do understand the reason for sale but the fact this is being sold for more than 2 years now in increments (from roughly 10% to now at little over 4%), I was just curious to understand why open market sale and not some kind of bulk deal given that business seems to be headed in the right direction.

Thanks again for sharing your thoughts.

3 Likes

Usha martin cup and handle breakout happened briefly and then stock price came down, so effectively this short term pattern has not played out. Longer term no change in views, as it remains a fundamental pick of mine. I would keep watch on range at bottom of cup around 125-127, and the 30 WMA which is around 126.

Overall it has been a laggard in a strong market. But sometimes in long term holdings these are the kinds of situations we have to learn to bear.

18 Likes

Usha Martin came out with stable Q2 numbers.

Impressive growth in revenue - 8% QoQ and ~ 38% YoY.

Net profit growth - -3.5% QoQ and ~36% YoY

H1’23 EPS increased by 29% to Rs. 3.25 compared to H1’22.

Company invested about 45 Cr. during 1st half of the financial year to create capacity by way of purchasing the land, machines and equipment.

2 Likes

Usha Martin results have been steady in a seasonally weak quarter due to monsoon (esp in Indian business). Comparing q on q does not work well in this business.

The really enthusing part of the results is strong growth in volumes and topline growth while maintaining margins in the range of 14-15% inspite of some headwinds like volatility in steel prices and uncertain global conditions.

Q2 FY 23 topline improved to 825 cr vs q2 fy 22 topline of 608 cr, a growth of 30%.

PBT improved in q2 fy 23 to 96 cr vs 70 cr for q2 fy 23.

q1 fy 23 EPS is at 2.6 and H1 FY 23 EPS is at 5.3 per share.

Balance sheet remains steady and return ratios continue to show improvement.

presentation and press release attached.

usha martin q2 fy 23 presentation.pdf (2.7 MB)

usha martin q2 fy 23 press release.pdf (308.8 KB)

12 Likes

The biggest overhang on share price is due to pledged shares by promoters I think, even though the results are good 53 percent pledge is too much risky I guess .kindly guide if I am wrong.

Usha Martin posted its Q2FY23 nos. today and it has been a solid quarter with significant volume growth. Q2 usually is a weaker quarter domestically due to monsoons and internationally this quarter has had multiple issues like significant currency fluctuations/steel price movement and the rest. What is very heartening is how the margins have remained consistently around 15% during the complete steel cycle (despite the possible inventory write offs) thereby showing the business strength due to its ability to pass on RM price movements. There are some interesting observations one can make from how the Usha Martin story has shaped over the years:

a) Not all backward integration makes sense: Usha Martin tried to get into commodity steel manufacturing to support its inhouse consumption. What this did was following:

-

Made the business cyclical and the margins variable with the steel cycle and hence taking away any predictability of margins. Also since backward integration was leveraged a bad steel cycle resulted in huge value destruction.

-

It forced Usha Martin to get into more commodity products like auto wires and the core business of rope making did less and less of value addition and competing with global companies and became more and more of an inhouse consumer of steel.

b) Owner interest vs Earnings Consistency & Predictability: The goal of a business is to maximize net owner earnings during the course of its existence. Consider the case if Usha Martin had continued with its steel business. There is no doubt during the recent steel cycle upswing and even during other time periods backward integration would have saved significant costs assuming financial leverage was managed properly. Over the longer period having steel plant would have increased owner earnings (look at tata steel long products before the acquisition of Neelachal Ispat). The markets on the other hand value consistency & predictability of earnings & ROEs over the ebbs & flows of earnings even though they might in totality be higher/better.

As a transient shareholder playing the growth and valuation game in this case my interests might not really be with the owners of the business looking to maximize the earnings over its existence.

In conclusion do look at companies going for backward integration and see if they are getting into commodities/commoditized products and unless this backward integration helps in increasing margins of the core product question the margin consistency and predictability.

30 Likes

I was reading this wonderful analysis on Usha Martin done by @Donald sir. Pardon my ignorance but I am struggling to add up the following:

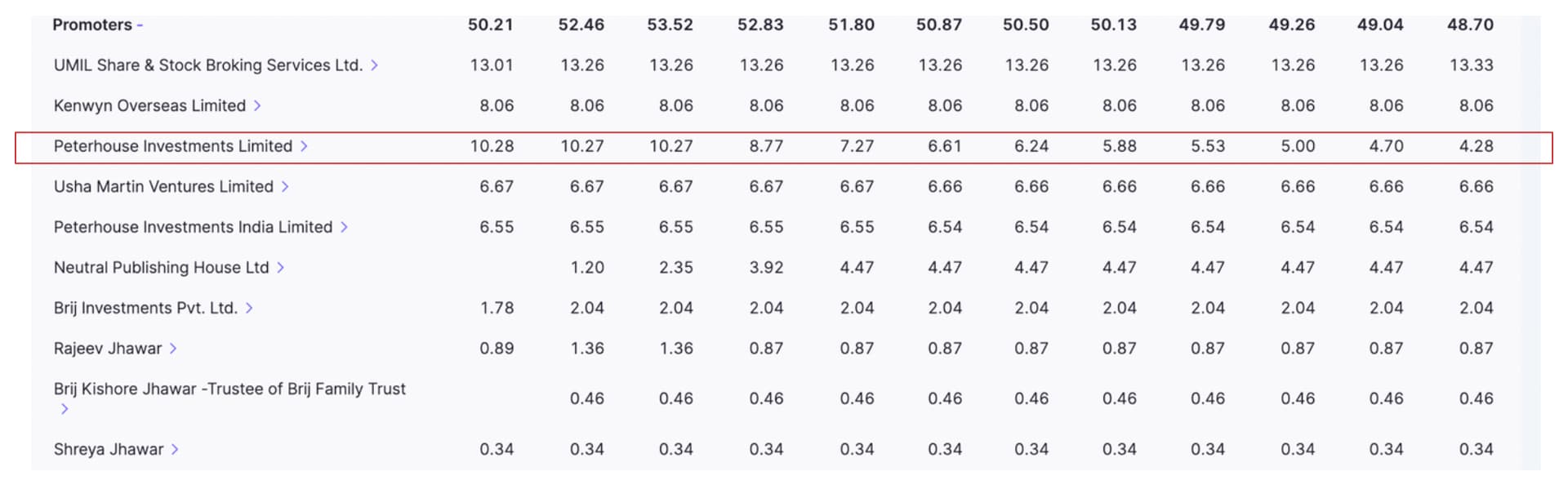

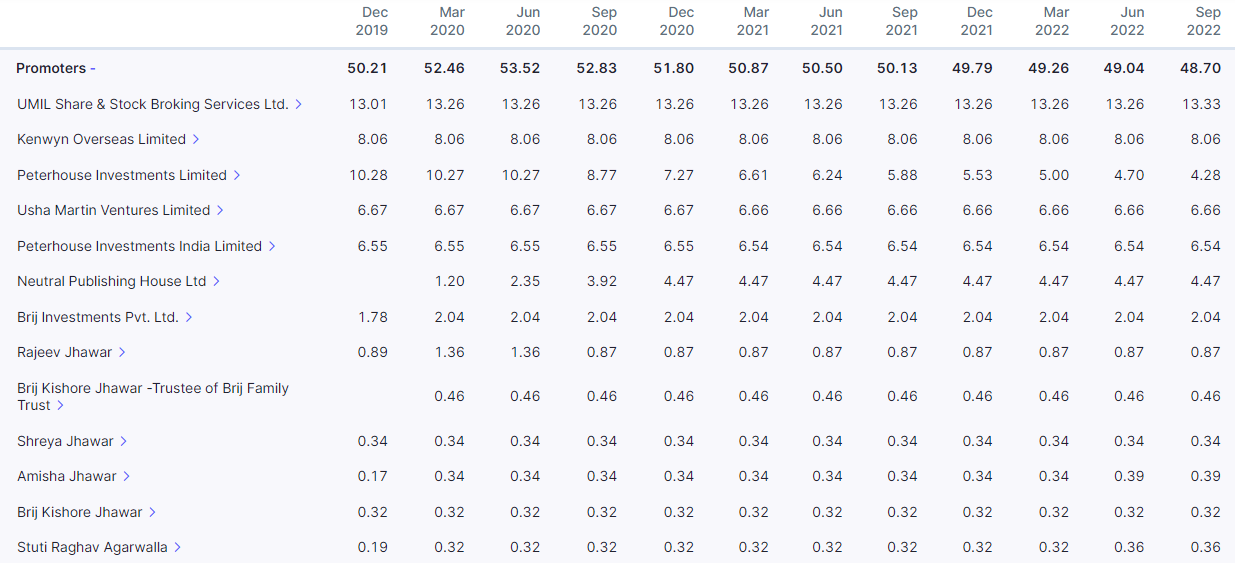

This is what I get from the screener (This perhaps doesn’t reflect the recent selling) from the top promoter holdings.

Just trying to do some maths to see how long the supply overhang would continue.

Not sure you are following this thread …This is known from long…Promoters are two brothers and one wants to exit from the business and he is actively selling on open market.

10 Likes

Promoter sold 200000 shares today as per screener feed. They have been selling for a long time (BSE disclosures). Any clue why?

As @Ajay_Kumar_Kommaraju has mentioned, this is a well-known fact about the company. Promoter holding has declined from 53.52% in Jun 2020 to 49.04% in Jun 2022.

Most of this is from Prashant Jhawar (CEO) controlled entities like Peterhouse Investments.

One view is that these sales are necessitated to service hard cash requirements of a plethora of business entities under Prashant Jhawar, including his London base, and it is likely to continue.

On the other side, Rajeev Jhawar (MD) lead consortium has increased its shares slowly in the company.

Edit [30-Dec-2022]: Included screenshot from Screener showing the decline of shareholding from Peterhouse Investments Limited

Source: Usha Martin Stock Story and Screener

Disclaimer: Not Invested

2 Likes

I think anyone interested in a company well covered needs atleast to read the full thread, especially when its started by one of the top contributors. That will not only answer most questions, but give you much more detailed insights into the company.

The question you raised has been answered very early on in the thread and in the stock story part. If guys are working hard to put up details on the company on VP, one has to alteast make the effort to read the thread completely.

Whenever I try to read about a company, after brief cursory look at annual reports, and details of the company, first thing I try to do is to look out if there is any thread on the company on VP and try to go through it. And its easy to make out who is more knowledgeable about the company by reading the thread. We can direct our queries to that person directly on thread (more preferred method) or indirectly through other means if answers are not forthcoming.

The best way to lose riding a multibagger is to get lost in unnecessary, irrelevant details.

Early on in the journey of a multibagger, there will be many grey areas and negatives. Our job as investors is to figure out what is important and ignorable and what is not. Taking the example of Page Inds, when stock price was around 3000-5000, a lot of investors were asking about promoters selling small chunks of shares off and on, and were unduly worried about that aspect. Since then Page inds has been one of the most consistent compounders in our market.

33 Likes

A massive fire has broken out today in the Ranchi plant of Usha Martin.

Per the article cited above, SP (Rural) Naushad Alam confirmed the incident saying that a preliminary probe suggested a ‘short circuit’ as the cause.

Also found a tweet with a live video apparently showing the fire blazing.

Thanks - Arnab Roy

Disclosure - Not Invested

5 Likes

Do we know - what is the quantum of impact due to fire. Rachi supposed to be the largest plan for Usha Martin?