ELEVATOR PITCH

-

Technology-Disruption-Free Industry. Very rare these days to find something where one can think of qualifying as above. Here one can hazard without much of trepidation that it indeed seems so for mission-critical wire rope applications for the next 5-10+ years. Offerings from major Synthetic/Fibre Rope companies (often cited as a disruptors) like Cortland, Samson Rope, Southern Ropes and English Braids have been found to be strong, durable and safe mostly in some marine, smaller machinery, and personal haulage applications, and have probably served more to expand the market to newer applications. New technologies across reinforced thermoplastics however, are getting a fresh look-in.

-

Hard-to-get-in applications, but-once-in very hard to dislodge. Think of the last 10+years where Usha Martin was mired in all types of misdemeanours and did virtually nothing to protect its turf, it still retained 60% plus market share in India, and #5 position globally

-

Formidable Global Leadership Challenger. With excellent delivery (Italy Design Centre/Ranchi Production) on high value-added application requirements leading to sequence of wins this year, there is dwindling technology differentiator leadership from Global majors. At the same time unmatchable cost-leadership by Usha Martin (RM/labour/energy fronts) ensures product delivery capabilities at 50% of market prices for even high-end applications places it in a very advantageous position to quickly gain customer approval/confidence

-

Timely Capex/Focused on Value Migration. Usha Martin is focused on upping the value migration curve significantly in the coming years. 60% of new expansion is going into high-end steel wire ropes segment - Elevators, Cranes, Mining. Wire Ropes. Plastication investment includes Plasticated LRPC with significantly higher margin achieved at very little incremental capex. Exiting lower margin wires (VC HT Black), shifting to higher-grade wire segments (HT 200/220/230), and other such higher contribution-margin wires. UM has also been intent on expansionary scale-up via newer geographies since last 4 years. Recent wins in high-end mining segment in Australia, South Africa, South America, and most profitable markets like the US, high-end deep sea fishing segment in South America bolsters the drive significantly. By the time customers gain confidence on initial delivery and scale up orders, the new capacity will be ready.

-

Rare High RoE-High FCF Combination. Usha Martin is doing a Capex of 285 Cr completely out of Internal Accruals of FY22 (PAT + Depreciation ~300 Cr). This should suffice for next 2 years expansion requirement. Meanwhile Profitability in 2-3 years is probably headed to 2x current levels. One can easily project 5 years and visualise this rare high Return on Equity, high Free Cash Flow combination playing out? Caveat - as long as they continue to NOT falter on execution front, and continue to gain market share. For how long do we think this market share gain game can continue to play out - 5 years, 10 years, Or?

CURRENT MARKET/INDUSTRY TRENDS

- Record high order book being seen by Major players

- Strong demand in US and Latin America

- Russian trade being scaled back by European and US players

- Energy shortage, materials, labour and logistics shortage

See more from Bekaert 2022 H1 Results

BARRIERS TO ENTRY

-

High-end applications in Steel Wire Ropes are mission critical - there can be no compromise on quality - say elevators, cranes, mining etc., as it can lead to accidents, loss of human lives. Very strict technical criteria, strict adherence to replacement cycles. New Vendor approval cycles are > 3-5 years. Besides Sales Contracts have in-built product-liability claims which need $Million insurance covers. Customers are generally very wary of bringing in new vendors. Extract from a competitor below:

-

Exclusive Dealers/Company-Owned Distributor /Warehousing set-up is probably unique to Usha Martin in this industry. An under-appreciated key strength for UM. This has been built up incrementally over last 40-60 years and is very hard/costly to replicate for any new entrant or even larger incumbents. Huge number of SKU/Inventory Management for Replacement Market is another big entry barrier to being close to the customer, servicing them efficiently and cost-competitively

-

Unit cost is a fraction of total product cost (wire rope cost vs lift/crane cost, say). Once product is entrenched, customer has little incentive to switch

-

No new player has been able to emerge and establish itself in the market for past 5-6 decades. There have been many who tried (domestically and globally) but have not been able to make a dent, sustain operations, and/or challenge incumbents significantly

BUSINESS MODEL (how does UM make money/win in the marketplace)

- Customised applications design, long-gestation approval process for high-end applications (4+ years)

- Replacement Market contributes 70-75% Sales (cyclicality hedged)

- Unmatched distribution strength (India) and in most important export markets

- Low-volumes, large no of SKUs, high inventory-carrying costs (highly skilled folks/operations required to manage efficiently)

- High entry barriers

- Huge cost competitiveness (on RM, labour, energy costs, SKU management)

- Growth primarily from gaining market share from large incumbents for foreseeable future

- Ability (also seen to be seizing string of high-end opportunities) for product mix shift/steep value-migration curve - 2-3x normal EBITDA in near term

- Low Incremental Fixed Capital Intensity, Sizeable Free Cash Flow generator

INTERESTING VIEWPOINTS

-

US market opportunities (hitherto virgin for UM) has now opened up for Usha Martin with BBRG closing Canada factory and shifting/consolidating Ropes platform in US (time required to shift - 9-12 months?)

-

Russian Market Opening up - Earlier Russia was importing (from EU/US) lots of high-end ropes particularly for mining and crane ropes but now with sanctions in place they are unable to do so, and UM is reportedly getting lot of enquiries. Expected to yield good results in next 2-3 years as Russia is another big market

-

As Oil prices move from $70-$100 levels, it has been seen lot new investments and new opportunities start coming in both on-shore and off-shore oil rigs. Actual Investments take time to fructify but UM has seen lot of enquiries and pipeline growing significantly in last 6 months. If Oil sustains above $100, UM sees strong uptick in Oil & Gas segment business for 2years plus.

-

Emerging Service Segment: Large oil-field companies like Cypher, McDermott, Technip engage UM for lot of services (stocking, cutting to size) in Europe with significant markup. Much higher-margin segment and one-step closer to the end-customer. Same model is being rolled out in Singapore markets, and slowly in Middle East. Expanding Services market does not require heavy investment. Needs local people, skilled knowledgeable people who know the market/application. Currently at $14Mn annual sales, expected to go to $20Mn in annual Sales in next 2 years

-

Design Centre in Italy (completely ex- Redaelli, post Teufelberger-Redaeli merger) is responsible for major new breakthroughs in Mining and other areas. Setup reportedly commands Million (Euros) annual salaries. This team is central (critical) to winning new higher-end product segments (like recently won mining segment products) competing against Bridon-Bekaert (Kiswire typically is NOT the competition here)

-

Key members of erstwhile Technical Team led by Sumit Modak (had joined Bharat Wires) is back in UM and in charge leading the latest expansion and modernisation drive happening at the Ranchi plant. The revised Capex plans (285 Cr) now include significant replacement of older machinery reducing equipment count to 1/3rd previous. This provides huge savings on space, energy, labour & manufacturing costs/overheads, and reduces wastage - giving a huge fillip to company’s rapid expansion plans.

-

Shreya Jhawar (ex JP Morgan, Innosight, 8 years) joined the business in Mar 2022 and is based out of Singapore. She is looking after Innovation Strategy & Growth. Shows Management’s renewed commitment to driving UM business forward energetically

-

Wire Ropes OEM Sales is mostly Technical Sales. Major Competitors do not have local technical teams to support Distributors in emerging regions like Asia. Usha Martin has mostly company-owned exclusive distribution set-up which also house technical sales teams from the company in countries like Australia, Vietnam, Indonesia, Malaysia, Singapore, Middle East, UK and Netherlands. Distribution business in Germany is expected to be launched within FY23

- Replacement Market is served ex-stock (huge number of low-volume SKUs), which places UM in an advantageous position vis a vis other Korean, European and American Competitors who do not have exclusive distributors and operate via Independent distributors (despite high inventory-carrying costs). Logistics and cost competitiveness play a very important role in serving local markets efficiently.

-

Products for on-shore oil rigs (strong UM segment) and Mining (emerging UM segment) are like consumables with short replacement cycle of 2-6 months. Maritime Ropes (12-18 months), Products for Cranes (1-4 years), Elevators (3-8 years), Suspension Bridges (10-20 years) have longer replacement cycle though.

-

Larger Competitors (excluding Kiswire?) are huge, unwieldy, having grown mostly through acquisitions vs a rejuvenated, refocused Usha Martin. Imagine where UM did nothing for almost 10 years+, and still retains 60% plus market share in domestic market, and #5 globally

BULLISH VIEWPOINTS

-

In 2016-2019 timeframe, company was dealing with steel segment and corresponding high debt, there was little or no focus on wire ropes business. With steel business sold, insolvency avoided and largely net debt free balance sheet, company finally seems to be focusing on wire ropes division. The company always had technological strength in wire ropes products (Brunton Shaw, UK/ Global Design Centre in Italy) but finally there is intention to translate this into revenues and build a high quality business.

-

With steel sourcing advantage from India, distribution strength of the business in India and more importantly overseas, some macro economic tailwinds (higher oil & gas prices encouraging capex/exploration investment globally) - the company has a real chance to get into Top 2-3 globally in Wire Ropes business in the medium term if they can execute well.

-

Protected Market - especially in high-end critical applications. No new players in the last 5-6 decades. It’s the same set of players competing against each other, improving the life of the product, new product development, trying to move up the value chain

-

OEM Sales: Replacement Market Sales is 25% : 75% for most product segments. So there is a steady flow of 70-75% of regular business, even in tough years.

-

Opportunity Size is huge - if the company can get its act together, get European and US Subsidiaries start doing as well as Asian subsidiaries have started delivering. Many geographies/markets are still virgin for UM. North American Steel Ropes market segment has reportedly much higher 2-3x margins, that UM has only very recently bagged initial orders in. Europe another big market - is fragmented with large share of smaller players. Russian Market enquiries have started pouring in (due EU/US sanctions)

-

UM is doing capex of 285Cr funded through internal accruals. Larger investment is in wire ropes segment (increasing volumes and improving product-mix) and for improving facilities and modernisation of Ranchi plant. Wire ropes capacity would be expanded by 30-35K MT. The capex is expected to be completed by Q4 FY23 and revenues start coming from FY24. The company expects Asset Turns of 1.5-2x on this capex.

-

Competitive Advantage: Local availability of Steel, Cheaper Labour. Lower energy Costs. Significant portion of UK finished products is sourced from India (in the form of wire strands) giving significant advantage over cost structure of European competitors. From some reports UM enjoys significant cost advantages ~30-35% over larger competitors. In recent high-end value-added segment wins like Mining, cost advantages are significantly higher which can aid rapid scale-up once customer approval is in and confidence is built

-

Ability to Pass on Raw Material Price Volatility - Post the sale of its steel division, UM demonstrated strong operational performance over FY20-FY22 with no supply glitches despite no backward integration. It now procures key raw material from the open market. However, during the slump-sale, UM had entered into an agreement with TSLPL for the supply of 100,000TPA of wire rods from the Jamshedpur unit up to FY24. This ensures raw material availability for around 50% of the requirement. For the balance requirement, the company relies on other domestic players in its vicinity. As most of the production is order-based, UM has been able to pass on volatility in raw material prices, albeit with a lag, as reflected in its range-bound EBITDA per tonne.

-

Steep Value-Migration curve - systematically reducing share of commodity/off-the-shelf products; phasing out extremely low-margin products; shifting from low margin VC Wires, HT Black to higher 200/220/230 grade segments or grade 3 grade 4 products; introducing higher-margin plasticated LRPC. Significantly 60% of additional 30K MT Wire Ropes capacity (post expansion) will be towards higher-value-added Mining, Ports, Elevator and Oil Sector products. Margin expansion visibility is very high, especially on the back of recent high-end segment wins, that can potentially scale-up rapidly

- Mining segment - This is a highly specialised segment with reportedly very high contribution margins. UM has only scratched the surface - with earlier wins in Australia, South Africa, and recently in Latin America and the US with some of the global mining majors like BHP, Glencore, and Rio Tinto?. These early wins with few large names help in opening doors/winning orders from other miners.

-

UM has booked more than 200T for mining ropes in America and South America this year. Expected to go upto 500 T/month within 2-3 years. The company is also looking to enter Russian market through a distributor.

-

On technical front for new customer projects, UM has either matched or exceeded life expectancy requirements. Plastication increases the life of the ropes, UM has capability to offer plastication for upto 78mm ropes currently. Capability for 127mm is expected to be on-stream soon enabling UM to offer improved lifespan for full range of products.

-

Port Crane Ropes - UM is the largest player with 87-90% market share from crane ropes in all major ports in India. Middle East and most of GCC countries UM has between 80-90% market share. Major ports in South East Asia including Singapore, Indonesia, Vietnam etc. UM enjoys significant share.

-

This segment is a success story for the company and company claims 80% win rate against players like BBRG, Kiswire. The competitive advantage stems from distribution and service (training, supervision, technical services in installation, maintenance) model and inventory that company holds in this segment and consequently ability to deliver products ex-stock. UM is making concerted efforts for entry in Europe, South America and US Markets for Crane Ropes as it sees a big opportunity.

-

Elevator Ropes - All the major elevator players Kone, Schindler, Otis are company’s customers. Company has received approval from Fujitsu for elevator ropes and supplies are expected to commence in the near term.

-

Fishing Ropes - UM secured a big win recently in the South American Market for deep sea fishing applications, where margins are high. Spain, Portugal and India are other markets Big markets for the company.

-

Well diversified customer segment spread. No one sector cyclicality is particularly damaging for the company. Besides replacement cycle demand spread out over 1-2-4-8-10 years plus (for different products) weighs in. The replacement cycles for various segment is as follows - crane ropes (1-4 years), oil & gas ropes (6-12 months), maritime ropes (12-18 months), mining ropes (2-4 months)., elevator ropes (3-8 years),

Following WireCo AR15 exhibit provides more details

BEARISH VIEWPOINTS

-

Overall Market is growing at sub 5% rates. So UM to do justice to its guidance of growing at least 15-20% CAGR for next 2-3 years, can only grow by taking away market share from Competitors (entering/penetrating hitherto virgin segments like Mining and newer geographies like US, LatAm, Russia)

-

With commissioning of JSW plant LRPC segment margin pressures may be imminent. Management feels UM has a good cost structure and will be able to maintain margins. Plasticated LRPC contribution will also help shore up margins

-

Volatility in Steel Prices and Freight Rates over last 7-8 quarters. UM has been able to maintain margins despite above volatility. Most contracts for EU and US have been converted to FOB pricing basis and price increase pass-through is enabled

-

UK and Thailand subsidiaries not doing well. Both subsidiaries are expected to start showing good turnaround in FY23. Thailand subsidiary will see an investment of $4-6 Mn in the next 2-3 year for wire ropes and fine chords segment to make these more sustainable. Steel purchase is able to be sourced through Tata Steel Thailand and other local steel companies at competitive prices

-

53.02% of promoter shareholding is currently pledged. Given the cleaned up balance sheet and strong cash flows, this should get cleared up pretty soon (?).

-

Though Rajeev Jhawar (MD) group has been increasing shareholding gradually, Promoter shareholding has seen gradual steady declines from 53.52% in Jun 2020 to 49.04% by Jun 2022. Bulk of the selling is seen from Prashant Jhawar controlled entities like Peterhouse Investments. Interestingly, it’s been consistently around ~10 Cr Sales every 3 months. One view is that these sales are necessitated to fund hard cash requirements of myriad business entities of Prashant Jhawar group including the London base, and likely to continue.

-

Prashant Jhawar shareholding is currently around 17% of shares outstanding, out of which 13% is pledged which cannot be sold (until revocation of pledge). The balance of 4% shares when sold, should get easily absorbed by the market, as has been the case so far

-

Enforcement Directorate (ED) case - The company is facing an ED case of 190 crores. The case is an old case related to iron ore export which the company had won in the High Court. But ED reopened the case in 2019 and attached assets of Rs.190 crores. Management is of the view that it has a very strong case. Even in the worst-case scenario, if the company loses the case, paying Rs.190 crores is not a challenge for the company at current cash flow levels .

-

16 Dec 2021 Supreme Court pulled up ED (on a petition filed by Usha Martin) on indiscriminate use of the PMLA Money Laundering Act and granted interim protection form arrest for petitioner and stay on earlier HC Summons. The remarks by SC are quite scathing and makes for an interesting read (an optimistic perception would point to bolstering Usha Martin case).

-

Central Bureau of Investigation (CBI) Bribery case - Usha Martin is facing a CBI case in which NMP Sinha a (recently) retired CBI officer was arrested accepting Rs.25 lakhs (allegedly provided by Usha Martin) from a middleman. Mr Sinha it is quoted in the reports as the same person (posted under the Economic offences wing of CBI as SP) who was earlier handling the Usha Martin cheating case against its mining arm. The CBI has made the company MD Mr Rajiv Jhawar accused, but the company has strongly denied the charges.

-

Should the ED case get dismissed in Usha Martin favour, the bribery case could automatically get shelved? ED and CBI cases are major overhangs on the stock. If & when these do get resolved in Usha Martin favour, UM could see higher participation from Institutional Investors

-

Backgrounder for feud within Usha Martin founding family here, here, and here

VALUATION MODEL

PAT without Exceptional income: ~260 cr

Market Cap- 4500 cr

Enterprise Value ~4800cr with Debt of ~300cr.

On a TTM basis, Usha Martin is available at ~17x PE given current market cap of Rs. 4500 Cr. Despite Covid introduced uncertainities there has been a marked improvement in performance metrics of the company in last three years.

Guided by management commentary in recent AGM and estimating a 20% growth (mgmt. guidance 20%) in topline and estimating a 16% OPM, FY23 Sales/EBITDA/PAT could be be ~3200/510/300 Cr giving one year forward estimate ~15x.

The breakout year for Usha Marin could be FY24 with the large planned capex coming onstream by Q4 FY23, and company scaling up on opportunities in high-margin value-added segments in newer geographies like US, Russia, LatAm, and Europe.

CORPORATE GOVERNANCE SCAN

[to be completed]

RED FLAGS/FORENSIC SCAN

[to be completed]

DISCLOSURE(s) of UM STOCK STORY CONTRIBUTORS

Rupesh Tatiya - Invested

Yachna Bhatia - Invested

Donald Francis - Invested

Anant Jain - Invested

USHA MARTIN BACKGROUNDER

Usha Martin Ltd is primarily engaged in manufacture and sale of steel wires, strands, wire ropes, cords, related accessories, etc. It is also involved in sale of other products such as wire drawing and allied machines.[1]

MAIN PRODUCTS/SEGMENTS

There are 3 segments in which company operates - Wire Ropes, LRPC and Wires.

WIRES & STRANDS

Wire and Strands is small segment with high competitive intensity. In FY22, this segment contributed about 13% of the standalone revenue. In terms of volumes, company sold 39K MT of volumes in this segment in FY22 on consolidated basis.

There are many competitors in this segment - basically steel manufacturing forward integrating into wires. There are companies like Tata Wiron on one end and D P Wires etc. on the other end.

The company is trying to get out of segments which has low contribution margins and get into better contribution margin segments. Most of the products are sold into auto industry which has contribution margins of 7-8K/MT and company hopes to take this number up in near term.

LRPC

LRPC is second largest segment of the company and this also has moderately high competitive intensity. In FY22, this segment contributed 27% of the revenue on standalone basis. The volumes sold on consolidated basis in FY22 were 65K MT.

Most of the large steel players are also present in this segment and are expanding capacity. The company has decided to be cautious in spending capex in this segment. Capacity is being expanded to 75K MT in FY23 and further to 85K MT by FY24. No further investments are envisaged.

This is a cyclical segment with large contribution coming from Infrastructure segment (most bridges use LRPC, metro projects). In an upcycle, all the companies make very good margins (18-20%+) and these margins go down to 10% in an downcycle. To mitigate this company has included in the latest expansion 10,000 MT of plasticated LRPC which fetches higher margins.

WIRE ROPES

Wire Ropes is the largest segment by revenue and profitability and the most interesting segment in the company. In FY22, wire ropes contributed 53% of the standalone revenue and majority of the revenue in overseas subsidiaries comes from wire ropes. Company sold 85K MT of wire ropes in FY22 on consolidated basis.

The company has strong competitive positioning in this segment.

The company has 50% market share in domestic market in wire ropes. The major competitor in domestic market is Bharat Wire Ropes (Two plants - capacity of 12K + 66K MT) which went through debt restructuring recently.

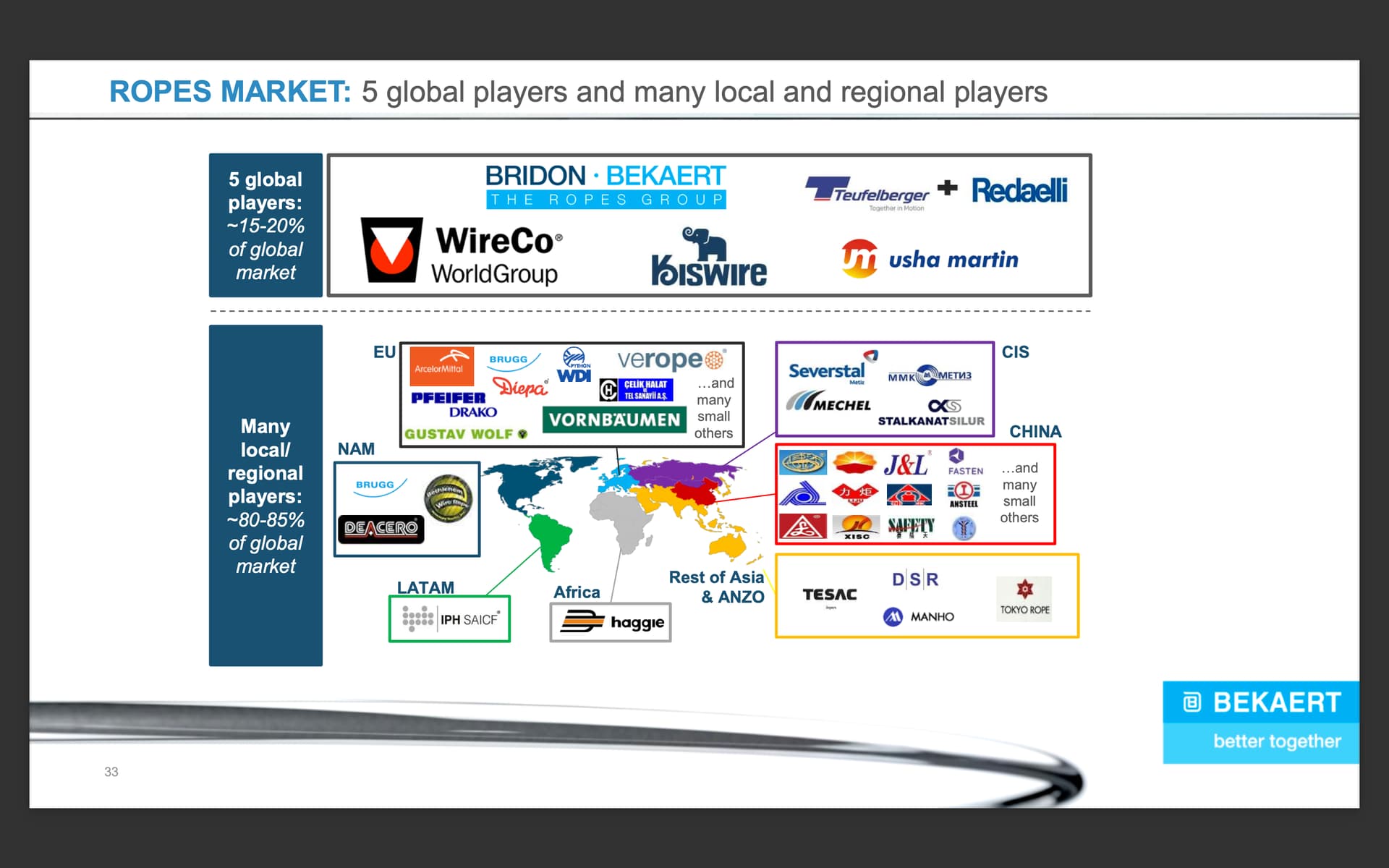

The company has ~5% market share in wire ropes globally. The global market has 5-6 global players and many regional players. The largest player globally is BBRG.

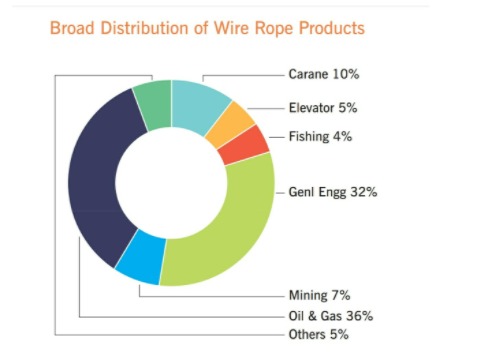

Following slide from 2019 Bekaert Capital Markets Day presentation captures the landscape quite well -

This segment is largely insulated from steel cycle and margins vary in a narrow band. The products are value added products that go into critical applications and has long approval cycle and inertia from customer side to change suppliers.

Following chart captures the volume wise data for 3 segments for last 10 years -

MANUFACTURING

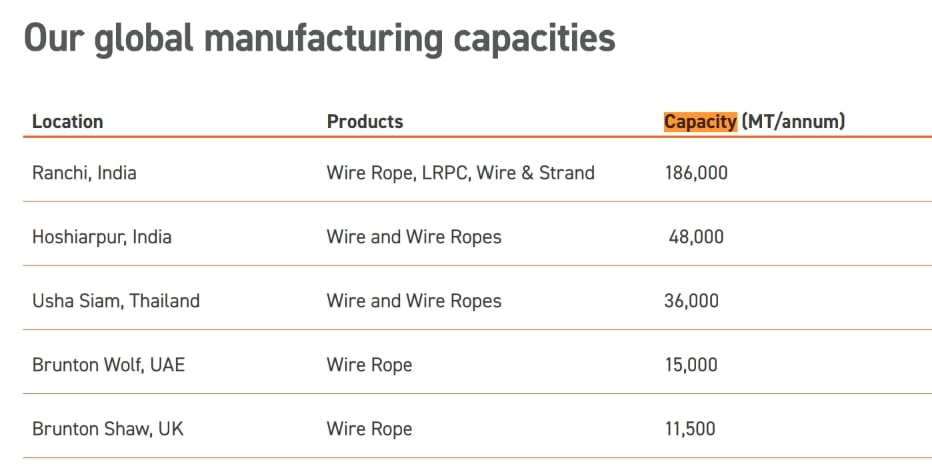

Manufacturing Capacities of the company is captured in the following image -

The company has manufacturing capacities of ~5500 TPM in India and with the capex it is expected to go upto 8000 TPM.

MAIN MARKETS

End industry segmentation was captured in older annual reports and it is provided below.

Ports segment is the highest contributor to Sales. Share of Oil & Gas segment has gone down to ~20% of sales and is expected to rise again. Fisheries, Elevators, Construction and Mining contribute ~5-7% Sales. Mining and Crane Ropes segment share should reflect increasing share given recent strong wins.

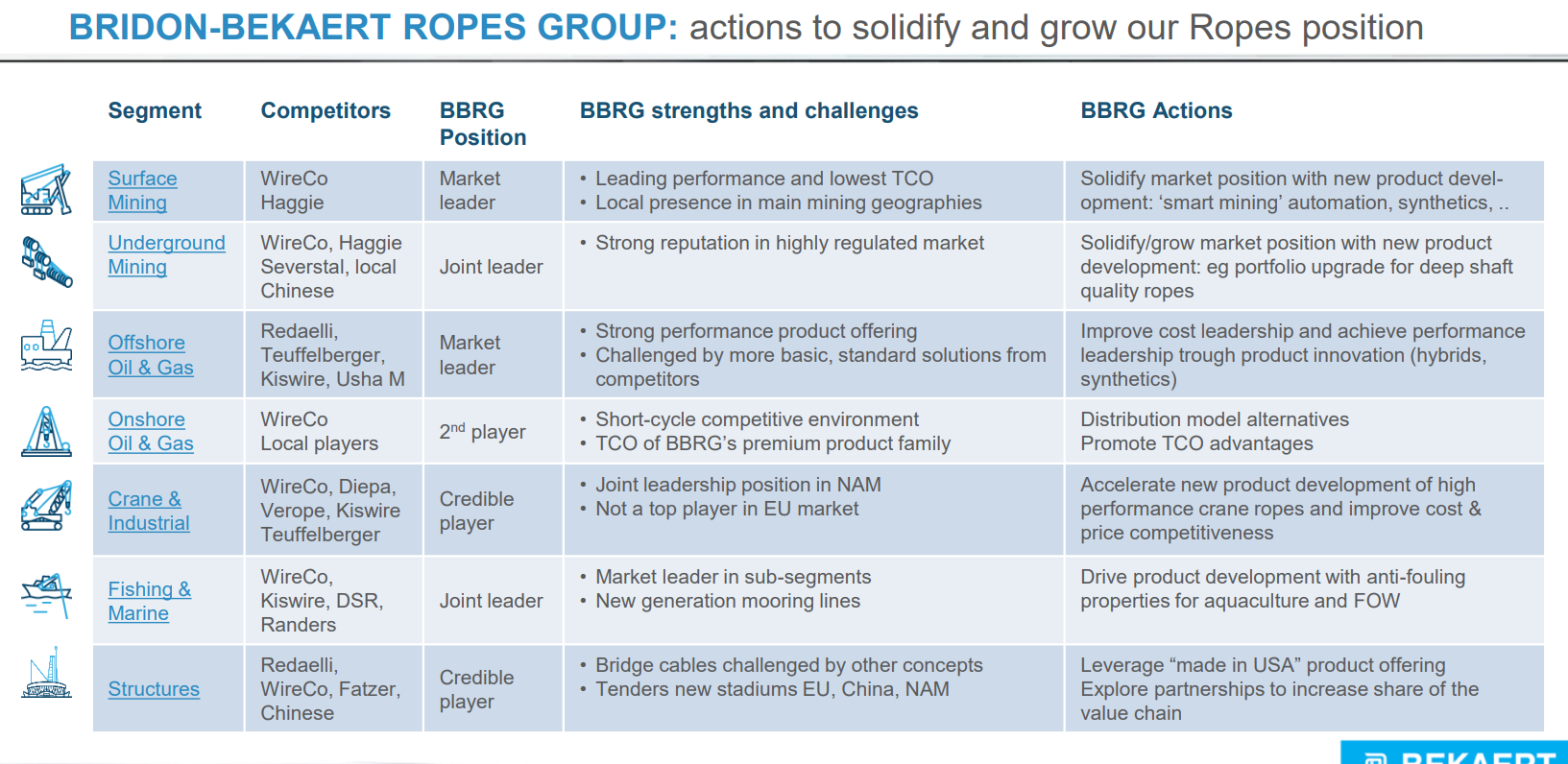

Following slide from BBRG capital markets day captures strengths and challenges of various segments as the leader does it. This provides good direction on how to think about these segments.

SUBSIDIARIES

* Pengg Usha Martin

JV between Usha Martin and Jon Pengg of Austria

Produces oil tempered wire required by automotive industry

* Brunton Shaw, UK

Provides all wall rope products

* European Management and Marine Corporation (EMMC)

EMMC corp holds contracts with Technip, Dolhpin drilling, Saipen, Bibby and Maesrk

DNV approved manufacturers of slings

* De Ruiter Stalkaabel BV

* Brunton Wire Ropes, FZCO

JV between Usha Martin and Gustav Wolf, Germany

Manufacturing in Jebel Ali Free Zone

-

Usha Siam Steel Industries Limited (USSIL)

-

TESAC Usha Wire Ropes

JV between USSIL and TESAC wire ropes, Japan

CUSTOMERS

Following is non-exhaustive list of customers of Usha Martin providing a glimpse into its global presence

Wire Ropes

**Bridges**

Lions Gateway Bridge (Canada), Vidyasagar Setu (Kolkata, India), Durgam Cheruvu (Hyderabad, India)

**Elevator Ropes**

Johnson Lifts, Otis (First company to get approval from Otis), Theyssenkrup Elevator India, Schindler India, Kone, Fujitsu

**Oil Exploration**

Shell Brasil, Kuwait Drilling company

**Crane Ropes**

Samudera Indonesia, Singapore Port, Adani Ports

**Mining Ropes**

BHP, Glencore Mines, Rio Tinto (?), Anglo American, South32

LRPC

L&T, Dilip Buildcon, JMC Projects