This is supposed to be a high quality thread and everyone is supposed to post relevant matters here.

Please don’t waste space and flow of this thread by putting up long winded posts which has little relevance.

This is supposed to be a high quality thread and everyone is supposed to post relevant matters here.

Please don’t waste space and flow of this thread by putting up long winded posts which has little relevance.

Please go through the company announcement regarding fire incident. Not major damage it seems.

usha martin fire announcement jan 2023.pdf (253.4 KB)

Why there is no exchange filing on the fire accident and the implication on the companies performance. Even the letter listed above is not signed by anybody.

Market also seem to have ignored the incident.

Usha has come out with good q3 fy 23 results. Main highlight has been managing margins in an environment where raw material (metals) prices have been volatile. Might be further proof that company is a pure play converter of steel and not much exposed to vagaries of steel price volatility.

Results for q2 fy 23 ( comparision is y on y)

Sales up 17% from 712 cr to 834 cr.

EBIDTA up 20% from 101 cr to 131 cr

Net profit up 25% from 67 cr to 84 cr.

9M EPS (not annualised) 8.05 per share.

results and press release attached.

usha q3 fy 23.pdf (4.8 MB)

usha q3 fy 23 press release.pdf (421.5 KB)

Is their any plans/news of company promoters to reduce it’s promoters pledges?

2 posts were merged into an existing topic: 52 week highs and all time highs strategy

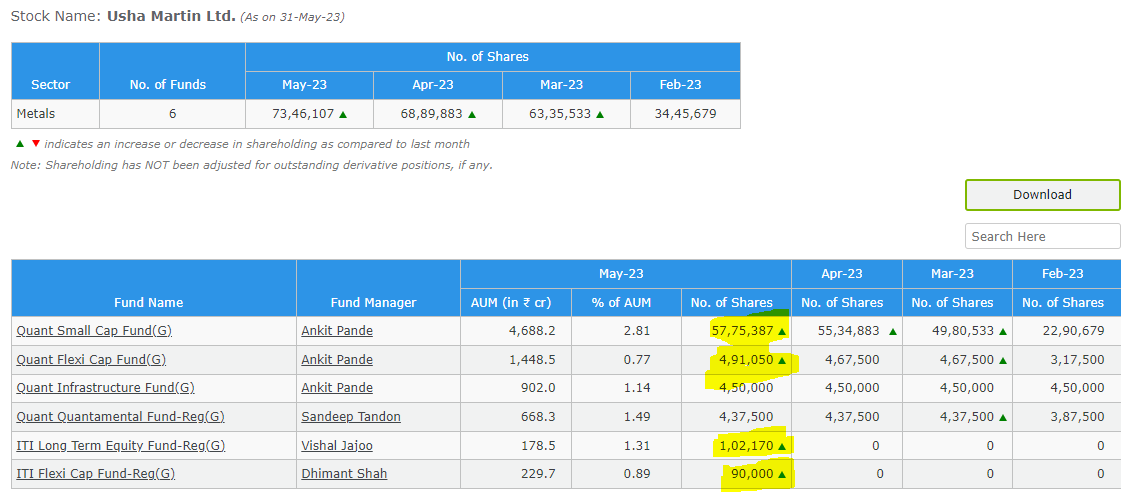

Technicals and charts apart, is there any data on buying by institutions which I strongly believe is the reason for this break out in price ?

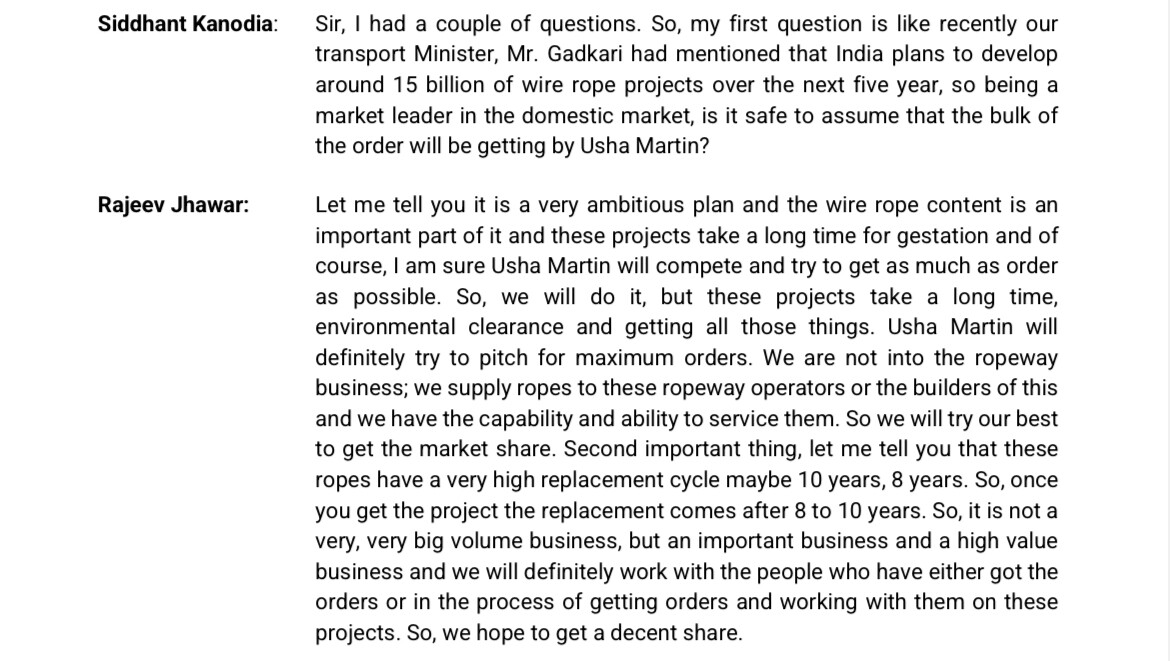

Article - India to build 250 ropeway projects worth ₹1.25 lakh cr: Nitin Gadkari

https://www.fortuneindia.com/macro/india-to-build-250-ropeway-projects-worth-125-lakh-cr-nitin-gadkari/112342

First ever Conf call, my detailed notes, 4th March 23:

Focus areas per mgmt:

Turn around in European subsidiary:

On ability to pass on RM - avg. consumption of wire rod has inc. from 44k/t (FY21) to 62k/t (FY23). EBITDA - 15.9 to 26.5k/t ( FY21 and 23 resp.) - we have been able to pass on RM increases, also increase EBITDA - active mgmt. on product portfolio - do more value-added products. LRPC is more linked to commodity prices. Plasticated LRPC is more of a specialty flavor. Company has been able to plan around this.

North America: Company initially focussed only around the Houston area in North America - 2-3% Market share (MS). Strengthened mgmt and opened offices in east and west. Able to get OEM orders. If we move to 4-5% will double our volumes.

biz model is to have our own distribution model - stock inventory according to customer needs - Leads to higher realization - and thus leads to higher ROCE. The target is to go towards 25% from 17 to 19% (currently)

Intend to do more of wire ropes; within LRPC want to do the value-added like plasticated LRPC; even within strands do value add - but both these won’t be as good as the ropes and specialized wire ropes.

Take FY23 as a benchmark going forward.

Capex plan: Phase 1 is 310 crores giving approx 40k TPA - Q3 FY24 target completion.

25-30k TPA is the output of 167 cr in phase 2 of capex - 18-24 months to complete—10k tonnes of wire rope. - predominantly for Mining Rope - are single-length ropes- need heavy machinery. Capacity can be 25-30kt - Installed capacity might be higher, but 10k TPA is what we realistically feel we can make and sell ( in the next 3-4 years).

62 crores for Thailand modernization for compacting and non-rotating ropes

Indian plant - crane ropes, mining ropes and some specialized wire ropes.

Value added would be aimed to be around 50% of the pie.

Plasticated LRPC - current capacity is 500tpm, after phase 1, 800-1000tpm - in 18-24 months

on wire front - in the past we had to evacuate the steel we had so we had higher contribution from this segment in the past and now the wires have come down - setting up 167 crores galfan line - zinc aluminum - 10ktpa and 10ktpa of specialized wires.

Servicing biz: Aberdeen and Rotterdam - turn over of 700 crores per year has been attained. Dubai and Thailand just started. Expect to grow by about 15-20% in the next few years. Margins are going to be higher than wires. 4-5% higher than regular wires.

ROCE target is 25% and this should lead to

Steel price has reached as high as 18k/t and still been able to manage the volatility. As we go to higher value-added products, steel as a component reduces.

Having a base in India helped seize on the opportunity during the geopolitical crisis. Next 3 years we have very good visibility.

Total capacity is around 300kt - 70% is our current CU. LRPC 60-65kt, Ropes 126kt, production is 110kt. Since product mix plays a vital role - getting to 70-75% CU is very good according to industry standards.

Revenue growth target = 15-18% CAGR

LRPC don’t plan to grow, as capacities grows across contribution will be lower overall. Ropes will contribute close 70-72% of revenue in the longer run.

Have to look at annual numbers and use FY23 as a base, not to look at quarterly numbers.

with steel prices softening currently, the company does not foresee any inventory loss.

OEM - 20% and replacement market - 80%

International subsidiaries - Capacities and capacity utilization (CU) below are for Ropes

BruntonShaw - 50% CU - no plans to expand here, as there is scope for growing here, based on client additions. When we get closer to 75-80% we will consider plans to expand.

BruntonShaw - a diff league, premium product is 200-350-400 Tonne single weight rope - goes into critical applications, very few players produce something like this.

Geographical comments:

Next 5 years, we have good visibility for growth, would not comment about 10 years.

Synthetic ropes and steel wire ropes - have very little common ground. Focus for us to stay in steel wire ropes.

Ebitda/tonne growth over the past two years - as it been because of steel prices or efficiency - its not steel prices which is a pass-through, its because of our product mix, wire rope contribution to pie has gone up.

International operation Ebitda/tonne has been - Rs. 27.6k/t

Domestic operation Ebitda/tonne has been - Rs. 18.7k/t

Share of International biz has also grown in the pie (realizations are higher)

We have a steel plant in Thailand and UK, and we don’t see a big steel price arbitrage (with ±$30-$40/tonne). This arbitrage was there 3 years ago during the pandemic.

60-65% Market Share(MS) in India for wire rope, good relationship with our dealer network (been with us for 40-45 years), key customers working relationship. Challenging to increase beyond a certain MS - we will definitely grow with govt. push. We see a good opportunity in other areas internationally, where the MS is very low - this will be our future growth driver.

for India with Gadkari’s announcement - We are not into the ropeway biz, we service them with our ropes - they have a longer replacement period - 8-10 years - we work with clients who have bagged these orders.

PS: any misinterpretations, mistakes, or typos are purely mine.

~Ganesh Raao

Does anyone have concall transscript or audio recording of q4 fy2022 of usha martin.

you can find audio recording uploaded on their website!

Transcript posted on exchange by the company https://ushamartin.com/upload/investorrelations/Earnings%20Call%20Transcript%20-%20Q4%20&%20FY%2022-23_20230508170046_earnings-call-transcript-q4-fy-22-23.pdf

Is it good news for usha martin as they are also into Ropeways .

Please share your views.

My notes from Usha Martin Limited- Annual Report 2022-23

One of our main focus areas would be to produce high-value products.

Target to achieve top-line CAGR of ~15% & Operating EBITDA margins of ~18% over the next 2-3 years.

To support this, we planned a capex of Rs. 310 crores during FY22 and Rs. 167 crores proposed during FY24. Our objectives include expanding our capacities, modernising our existing production facilities to improve productivity and reduce the cost to serve, enhancing our R&D and testing facilities, improving our plant infrastructure, and digitalizing our operations.

The increased capacities would primarily focus on value-added products such as

We plan to fund most of the capex through internal accruals, with about 20-25% through debt, and our focus is on achieving asset turns of 2-3x over the next two years at optimal utilz levels.

We have successfully expanded our business by diversifying into various geographies and sectors. This has helped us reduce our dependence on a single product or market and enabled

us to sustain growth and profitability. International business have recorded

a substantial growth in revenue, and made up 55% of our FY 2022-23 revenue. Revenue from international operations recorded a substantial increase of 34% in FY 2022-23 over the previous year.

Our growth is supported by both macro-economic and internal factors. Macro-economic factors, such as growth in the oil & gas and renewable energy sectors, specifically offshore wind, continue to strengthen our performance.

Key growth segments include:

The Indian economy however showed remarkable resilience through these tough times

due to its strong fundamentals. Development in sectors like -

Volumes:

| PRODUCTION VOLUME Value Added PRODUCTS–STANDALONE | ||

|---|---|---|

| FY 2022-23 | FY 2021-22 | |

| Wire Ropes | 64,428 | 59,802 |

| Wire/ Strands/LRPC | 91,853 | 93,450 |

| Conveyor Cord | 3,129 | 2,343 |

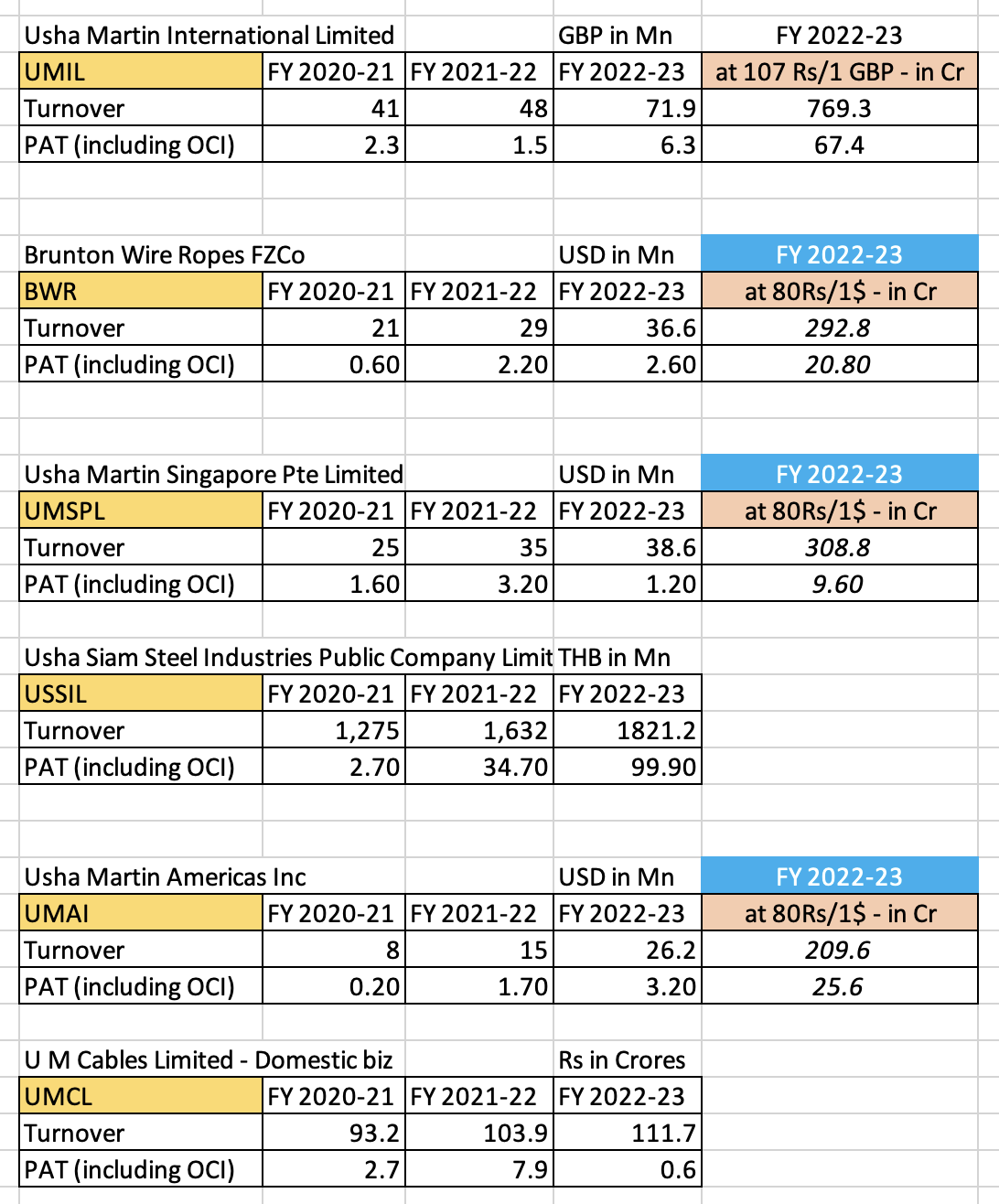

Subsidiaries of Usha martin - Sales and PAT

Opportunities

Threats, Risks & Concerns

Outlook

Government spending in infrastructural and social welfare projects such as roads, railways, water, and sanitation along with an expected revival in the auto sector will give an impetus to the demand of specialty products of the Company. With a renewed focus on specialty wire-rope business and strategic initiatives to consolidate leadership, the Company is undergoing a strategic transformation.

A couple of key points from MD’s commentary:

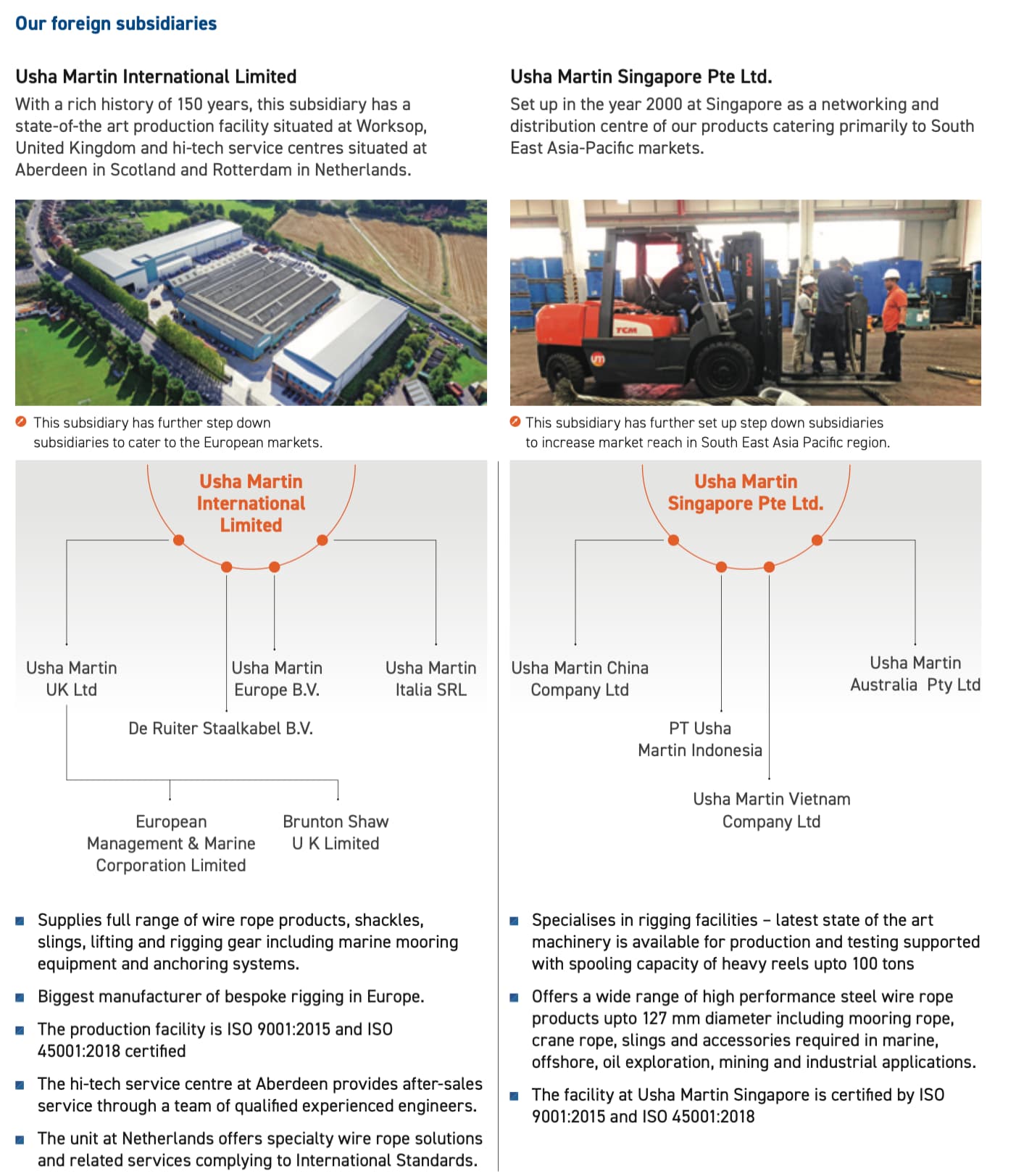

They have added a nice visual subsidiary chart, reproducing as-is for quick reference.

and

Brunton Shaw is Usha Martin’s subsidiary.

Bekaert which is an international peer of Usha Martin reported 16% Topline growth and 13% EBIT growth.

Offshore Oil & Gas capex has been picking up if we read the commentaries of offshore drilling contractors in US (Both are listed).

Moreover, Bharat Wires grew its volumes by 15% and sounded positive in the concall.

Sectors often do well together. Good signs for Usha M.

Disc: no recommendation to buy or sell. No transactions in last 30 days.

From Latest credit ratings

Large Capex Majorly Self-funded: UML is undertaking debottlenecking, modernisation, upgradation and capacity enhancement of the plant at Ranchi, Jharkhand, which shall enhance its overall capacity in India by around 25% to 291,000 tonnes per annum (TPA). UML also plans to enhance capacity at its Thailand plant by 8% to 39,000TPA. The total estimated cost is INR5.390 billion (increased from INR2.856 billion due to increase in scope) and the capacities are likely to become operational in phases over 3QFY24-1QFY26. Around 80% of the project will be funded by internal accruals and the balance by term debt (INR1.00 billion; 100% sanctioned, INR0.55 billion yet to be disbursed as on 31 March 2023). The capacity expansion plan also includes adding new high-value, high-margin niche products to UML’s portfolio, having a significant demand in the export market. Thus, the expanded capacities shall be more EBITDA-accretive than the existing operations once fully operational. Ind-Ra believes the company shall have adequate internal accruals supported by strong operational cash flows (likely to be over INR3 billion per year), free cash balances (FYE23: INR1.569 billion), unutilised working capital lines (end-March FY23: INR3.17 billion) as well as the realisation of pending dues from TSLPL (INR0.8 billion). UML shall remain 100% self-sufficient in terms of power as its existing power plant has surplus capacity. Also, with the modernisation and upgradation of facilities, the total power consumed per unit is likely to reduce, thereby improving the efficiency of operations over the medium term.

Ability to Pass on Raw Material Price Volatility: Despite the absence of backward integration post the sale of its steel division, UML demonstrated strong operational performance over FY20-FY23 with no supply glitches. It now procures key raw material (wire rods) from the open market. However, during the slump-sale, UML had entered into an agreement with TSLPL for the supply of 100,000TPA of wire rods from the Jamshedpur unit up to FYE24; this ensures raw material availability for around 50% of the requirement. For the balance requirement, the company relies on other domestic players in its vicinity and has diversified its supplier base over the last 12 months. As most of the production is order-based, UML has been able to pass on volatility in raw material prices, albeit with a lag, as reflected in its range-bound EBITDA per tonne