Since the previous thread was closed, restarting another one on the company

15 Likes

Usha Martin valuation seems comfortable for a almost zero debt co leader with 65% mkt share in India & growing tks to the myriad application of its products in elevators. Mimes, OIL & gas, Ports, construction etc. Its also among top 4-5 steel wire n ropes producers in the world.

Co post its sale of steel business is now focused on value added steel wire segments .Its no longer a commodity play but a steel processor with pricing power albeit with a lag of 1 Qtr. or 2. Most of its exports are also now on FOB basis unlike CIF basis earlier.

Any concerns on inventory days side ? Prashant Jhawar branch still has good stake which they keep selling so supply overhang also there.

VIEWS INVITED.

PPT DEC 21.pdf (2.7 MB)

11 Likes

Usha Martin q4 fy 22 presentation. Short and concise, as presentations should be. They should not make us lost in details. ![]()

Important point for me was "Price stoked the recovery this fiscal, volume the driver for next. " Plus debt reduction and dividend payment is a welcome step. Good free cash flow generation.

usha martin q4 fy 22 presentation.pdf (2.9 MB)

17 Likes

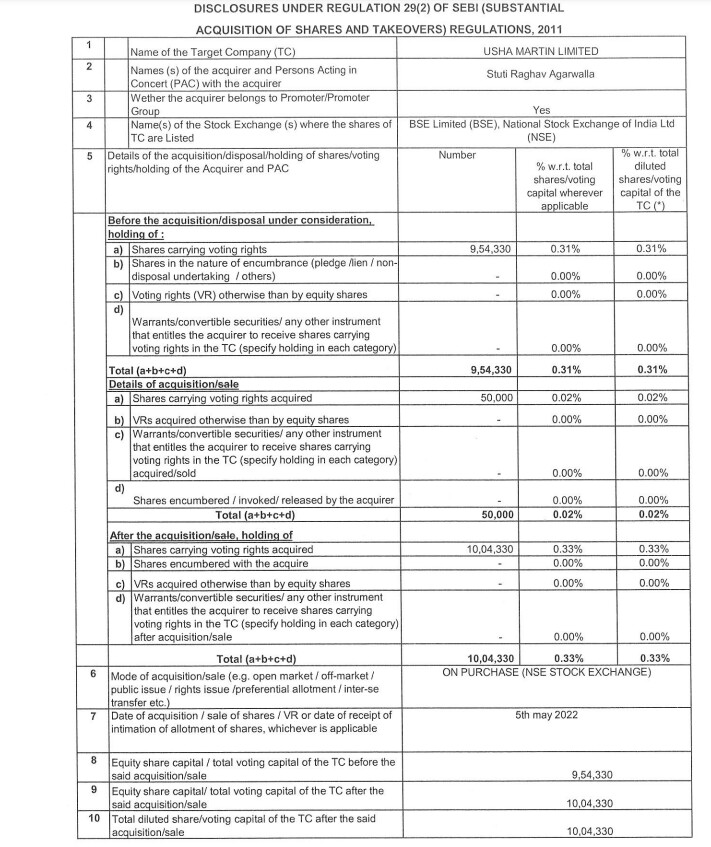

Usha Martin promoter Stuti Raghav Agarwalla acquired 50,000 shares from market today (5-May-22) amounting to 0.12%

More buying:

Usha Martin promoter Stuti Raghav Agarwalla acquired 25,670 shares from market today (6-May-22)

7 Likes

As per trendlyne, there were also 600,000 shares sold by “Peterhouse Investments” recently which is listed as a promoter.

2 Likes

This company sales one of the premium product for whcih there is a continuous demand and no promotion is required but than also this company never got the desired valuation

The reason is corporate governance

1 Like

Confusingly there are two entities with similar names in promotor group, “Peterhouse investments limited” and “Peterhouse Investments India Limited”.

The first one has reduced its stake to more than half, in the last two years now. There is constant downward pressure on the stock price.

Two brothers- one selling and the other buying. Checking the past history might help here ![]()

9 Likes

Thanks @Worldlywiseinvestors. Now I recall your video where you mentioned this. Given the pattern there is still 5% more to go.

2 Likes

One of the products of Usha martin I am aware of is Post Tensioning cables, This are highly specialised pre-coated and sleeved cables, This are used by us in post-tensioned & pre-stressed structures.

Though this type of designing structure is not new, but the trend is now picking up due to new un-bonded cables which are pre coated and sleeved which reduces both cost and efforts significantly compared to a bonded PT (Post-tentioning).

Another reason for the trend to pickup momentum is PT structures gives more flexibility compared to conventional RCC structures in designing very long spans, flat slabs, voided slabs, slim beams etc. and architects also recommend us to use more PT then conventional RCC structures.

Other benefits of PT include saving of resources & time of construction compare to conventional RCC structures.

Other 2 companies I am aware of providing such cables are DP Wires (listed) and Kataria (not listed).

This is a niche segment right now but there are even more application of PT cables, like in pre-engineered buildings, Pre-cast segments etc.

14 Likes

Usha AGM NOTES:

5 Likes

A few words about the technicals. The stock is in a clear uptrend above the 200 DMA. Formed a cup and handle breakout.

Invested from 137 level based on some TA since it’s no more cheap as it used to be 1 year back. But the controlling promoter buying from open market recently gives confidence.

2 Likes

But oil only contributed 15-20% of the revenue.

Before the restructuring the company was more of steel play and hence used to move along with steel cycle.

Regards,

Raj

Disc: Invested

See if you can compare the chart by putting in nifty levels below the stock price level and oil price level… Might be correlated more with overall mkts…

2 Likes

Exactly. Chart is just showing past correlations, due to exposure to steel business, smaller contribution to oil& gas etc… Could possibly see decoupling now, correlations may not sustain, cant say… point was that it followed crude well in the past…

Current Daily TF: Nice ARC setup in chart, and respecting the arc as well…

1 Like

Yes Hitesh bhai, excellent spotting: Seems to follow the trajectory expect for the Yellow marked periods:

2 Likes

Solid Set

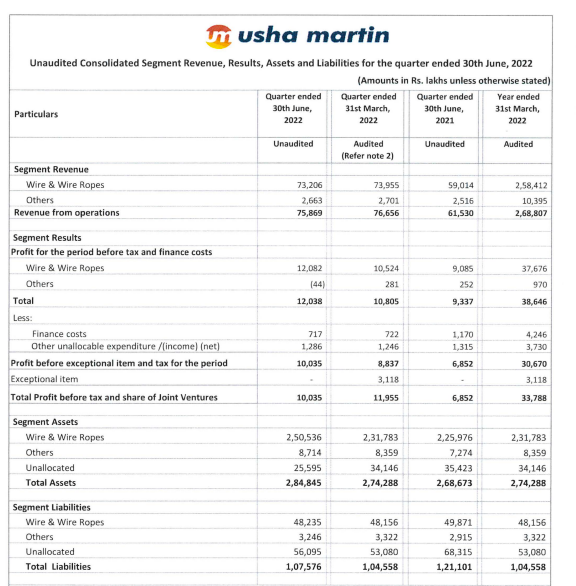

EBIT in wires division has grown 108 crores to 120 crores QoQ. Almost a growth of 12%

YoY ebit has grown from 93 crores to 120 crores.

PAT not comparable QoQ due to exceptional items and tax rates.

Disc:- invested since Rs68. Interesting to see the perception change slowly and numbers playing out. Not a reco.

11 Likes