all my learnings from valupickr, youtube, scuttlebutt, annual reports, and other sources

USHA MARTIN- A POTENTIAL TURNAROUND

ABOUT

UM is engaged in the business of manufacturing and sale of steel wires, strands, wire ropes, cords, related accessories, etc. Majority of company’s products are value-added as they are customized based on the customers’ requirements, resulting in higher and more stable realizations and better customer relationships.

The company’s products cater to various non-correlated end-user industries - elevators, mining, container port cranes, fishing, others.

Basically the cables that are used in the elevators of your residential buildings and corporate offices, the cables used in the mines, cables used in cranes to carry extremely heavy weights, the cables used in fishing rods used by fishermen, these cables are made up of the steel wires and ropes that are manufactured by UM martin.

On technical front for new customer projects, UM has either matched or exceeded life expectancy requirements. Plastification increases the life of the ropes, UM has capability to offer plastification in ropes (better margin).

The company is trying to get out of segments which has low contribution to margins and get into higher margin segments.

The company has manufacturing capacities of ~5500 TPM in India and with the capex it is expected to go up to 8000 TPM.

INDUSTRY

The industry is growing at 4-5% CAGR.

The industry in which UM operates is a technology disruption free industry (very hard to come across these days).

Industry trends- record high order books being reported by major players, strong demand in US, LATIN AMERICA and RUSSIA.

No new player has been able to emerge and establish itself in the market for past 5-6 decades. There have been many who tried (domestically and globally) but have not been able to make a dent, sustain operations, or challenge incumbents significantly.

Replacement Market contributes 70-75% Sales (thus cyclicality is hedged).

Low-volumes, large no of SKUs, high inventory-carrying costs (industry feature).

OEM Sales: Replacement Market Sales is 25%:75% for most product segments. Therefore there is a steady flow of 70-75% of regular business, even in tough years.

Mining segment - This is a highly specialized segment with reportedly very high contributing margins. UM has only scratched the surface - with earlier wins in Australia, South Africa, and recently in Latin America and the US.

Port Crane Ropes - UM is the largest player with 87-90% market share from crane ropes in all major ports in India. Middle East and most of GCC countries UM has between 80-90% market share. Major ports in South East Asia including Singapore, Indonesia, Vietnam etc. UM enjoys significant share.

Elevator Ropes - All the major elevator players Kone, Schindler, Otis are company’s customers. Company has received approval from Fujitsu for elevator ropes and supplies are expected to commence in the near term (this customer basket also creates a sense of confidence for the customers).

Fishing Ropes - UM secured a big win recently in the South American Market for deep sea fishing applications, where margins are high. Spain, Portugal and India are other markets big markets for the company.

LRPC- Most of the large steel players (JSW and TATA) are also present in this segment and are expanding capacity. The company has decided to be cautious in spending capex in this segment. This is a cyclical segment with large contribution coming from Infrastructure segment (most bridges use LRPC, metro projects). In an upcycle, all the companies make very good margins (18-20%+) and these margins go down to 10% in a downcycle. To mitigate this company has included in the latest expansion 10,000 MT of plasticated LRPC which fetches higher margins.

Well diversified customer segment spread. No one sector cyclicality is particularly damaging for the company. Besides replacement cycle demand spread out over 1-2-4-8-10 years plus (for different products) weighs in.

What’s the story of turnaround (past versus present)

In 2016-2019 timeframe, company was dealing with steel segment and corresponding high debt, there was little or no focus on wire ropes business. With the steel business sold (to TATA, there is still a chunk of that payment left to be paid by TATA to UM), insolvency avoided and largely net debt free balance sheet, company finally seems to be focusing on wire ropes division.

UM Martin is focused on upping the value migration curve significantly in the coming years. 60% of new expansion is going into high-end steel wire ropes segment - Elevators, Cranes, Mining. Wire Ropes. Exiting lower margin wires (VC HT Black), shifting to higher-grade wire segments (HT 200/220/230), and other such higher contribution-margin wires. Recent wins in high-end mining segment in Australia, South Africa, South America, and most profitable markets like the US, high-end deep sea fishing segment in South America bolsters the drive significantly. By the time customers gain confidence on initial delivery and scale up orders, the new capacity will be ready.

With steel sourcing advantage from India, distribution strength of the business in India and more importantly overseas, some macroeconomic tailwinds (higher oil & gas prices encouraging capex/exploration investment globally) - the company has a real chance to get into Top 2-3 globally in Wire Ropes business in the medium term if they can execute well.

UM is doing a Capex of 285 Cr completely out of Internal Accruals of FY22. This should suffice for next 2 years expansion requirement. Meanwhile Profitability in 2-3 years is probably headed to 2x current levels. One can easily visualize this rare high Return on Equity, high Free Cash Flow combination playing out. As long as they continue to not falter on execution front, and continue to gain market share.

The Capex plan includes significant replacement of older machinery. This provides huge savings on space, energy, labor & manufacturing costs/overheads, and reduces wastage, giving a huge benefit to company’s rapid expansion plans .

Imagine where UM did nothing for almost 10 years+, and still retains 60% plus market share in domestic market, and #5 globally. Now just imagine what can happen with the new refocused and rejuvenated mindset and strategy UM is enforcing.

Post the sale of its steel division, UM demonstrated strong operational performance over FY20-FY22 with no supply glitches despite no backward integration. It now procures key raw material from the open market. However, during the slump-sale, UM had entered into an agreement with TSLPL for the supply of 100,000 TPA of wire rods from the Jamshedpur unit up to FY24. UM has been able to pass on volatility in raw material prices, albeit with a lag.

Steep Value-Migration curve- systematically reducing share of commodity; phasing out extremely low-margin products; shifting from low margin VC Wires, HT Black to higher grade segments; introducing higher-margin plasticated LRPC.

MANAGEMENT

Although the top management is non technocrat, they have a vast experience of various industries and are or have been in the board of top companies and Groups.

If carefully observed the management actions and plans through the annual reports and investor presentations, there seems to be a concrete plan/vision that the management has. Kind of a renewed interest one can say to drive growth and profitability. Decision to sell the steel segment, reducing debt, entering into higher margin products, doing a huge capex in higher margin products, getting the younger generation of executives ready to drive future growth by letting them handle the growth divisions. All these things signal to a management with a new and future ready thought process.

Key members of erstwhile Technical Team led by SUMIT MODAK (had joined Bharat Wires) is back in UM and in charge leading the latest expansion and modernization drive happening at the Ranchi plant (shows as to how they incentivize/compensate the top executives). SHREYA JHAWAR (ex JP Morgan, Innosight, 8 years) joined the business in Mar 2022 and is based out of Singapore. She is looking after Innovation Strategy & Growth. Shows Management’s renewed commitment to driving UM business forward energetically through the younger generation.

The remuneration of the top management is well within the stipulated limits.

Entry Barriers

SWITCHING COST- Hard to get in applications but once in hard to be replaced. This is due to high switching costs (mental model), this is as the products of Usha are a fraction of the cost of the customer’s final product so the customer really needs an incentive to switch to another product. Think of the last 10+years where Usha Martin was nose deep in all types of misdemeanours and did virtually nothing to protect its turf, it still retained 60% plus market share in India, and #5 position globally.

STRONG CUSTOMER RELATIONSHIPS- With excellent delivery on high value-added application requirements leading to sequence of wins this year, there is dwindling technology differentiator leadership from Global majors. At the same time unmatchable cost-leadership by Usha Martin (RM/labor/energy fronts) ensures product delivery capabilities at 50% of market prices for even high-end applications places it in a very advantageous position to quickly gain customer approval/confidence.

CRITICAL APPLICATION- There can be no compromise on quality, say elevators, cranes, mining etc., as it can lead to accidents, loss of human lives. Very strict technical criteria, strict adherence to replacement cycles. New Vendor approval cycles are > 3-5 years. Besides Sales Contracts have in-built product-liability claims which need $Million insurance covers. Customers are generally very wary of bringing in new vendors.

EXCLUSIVE DEALERS/COMPANY- Owned Distributor /Warehousing set-up is probably unique to UM in this industry. An under-appreciated key strength for UM. This has been built up incrementally over last 40-60 years and is very hard/costly to replicate for any new entrant or even larger incumbents. Huge number of SKU/Inventory Management for Replacement Market is another big entry barrier to being close to the customer, servicing them efficiently and cost-competitively.

Thesis/triggers

US market opportunities has now opened up for Usha Martin with BBRG closing the Canada factory.

Russian Market Opening up - Earlier Russia was importing (from EU/US) lots of high-end ropes particularly for mining and crane ropes but now with sanctions in place they are unable to do so, and UM is reportedly getting lot of enquiries. Expected to yield good results in next 2-3 years as Russia is another big market.

Germany is a huge supplier of wire ropes, but due to issues of high costs of energy and RM some of the customers may shift to India.

As Oil prices move from $70-$100 levels, it has been seen lot new investments and new opportunities start coming in both on-shore and off-shore oil rigs. Actual Investments take time to fructify but UM has seen lot of enquiries and pipeline growing significantly in last 6 months. If Oil sustains above $100, UM sees strong uptick in Oil & Gas segment business for 2years plus.

Emerging Service Segment: Large oil-field companies engage UM for lot of services (stocking, cutting to size) in Europe with significant markup**. Much higher-margin** segment and one-step closer to the end-customer. Same model is being rolled out in Singapore markets, and slowly in Middle East. Expanding Services market does not require heavy investment. Needs local people, skilled knowledgeable people who know the market/application. Currently at $14Mn annual sales, expected to go to $20Mn in annual Sales in next 2 years.

Many geographies/markets are still virgin for UM. North American Steel Ropes market segment has reportedly much higher 2-3x margins, that UM has only very recently bagged initial orders in.

UM is doing capex of 285Cr funded through internal accruals. Larger investment is in wire ropes segment (increasing volumes and improving product-mix) and for improving facilities and modernization of Ranchi plant. Wire ropes capacity would be expanded by 30-35K MT. The capex is expected to be completed by Q4 FY23 and revenues start coming from FY24. The company expects Asset Turns of 1.5-2x on this capex.

Competitive Advantage- Local availability of Steel, Cheaper Labor, Lower energy Costs. Significant portion of UK finished products is sourced from India (in the form of wire strands) giving significant advantage over cost structure of European competitors. From some reports UM enjoys significant cost advantages ~30-35% over larger competitors. In recent high-end value-added segment wins like Mining, cost advantages are significantly higher which can aid rapid scale-up once customer approval is in and confidence is built.

Significantly 60% of additional 30K MT Wire Ropes capacity (post expansion) will be towards higher-value-added Mining, Ports, Elevator and Oil Sector products. Margin expansion visibility is very high, especially on the back of recent high-end segment wins, that can potentially scale-up rapidly.

UM has booked more than 200T for mining ropes in America and South America this year. Expected to go up to 500 T/month within 2-3 years. The company is also looking to enter Russian market through a distributor.

The infra push by government may lead to higher sales of the LRPC segment which has higher realizations.

The company is deleveraging and has already significantly reduced the debt, this in turn will lead less stress on the P&L statement by increasing the PBT.

There is an increase in the demand for real estate, as more and more buildings and offices will be built, they need elevators and UM already being certified by the major elevator players will be the preferred choice for supplying wire ropes.

Antithesis/risks

Overall Market is growing at sub 5% rates. So UM to do justice to its guidance of growing at least 15-20% CAGR for next 2-3 years, can only grow by taking away market share from Competitors which can be a bit messy.

With commissioning of JSW plant LRPC segment margin pressures may be imminent. Management feels UM has a good cost structure and will be able to maintain margins.

Volatility in Steel Prices and Freight Rates over last 7-8 quarters. UM has been able to maintain margins despite above volatility. In most contracts for EU and US price increase pass-through is enabled.

UK and Thailand subsidiaries not doing well. Both subsidiaries are expected to start showing good turnaround in FY23. Thailand subsidiary will see an investment of $4-6 Mn in the next 2-3 year for wire ropes and fine chords segment to make these more sustainable.

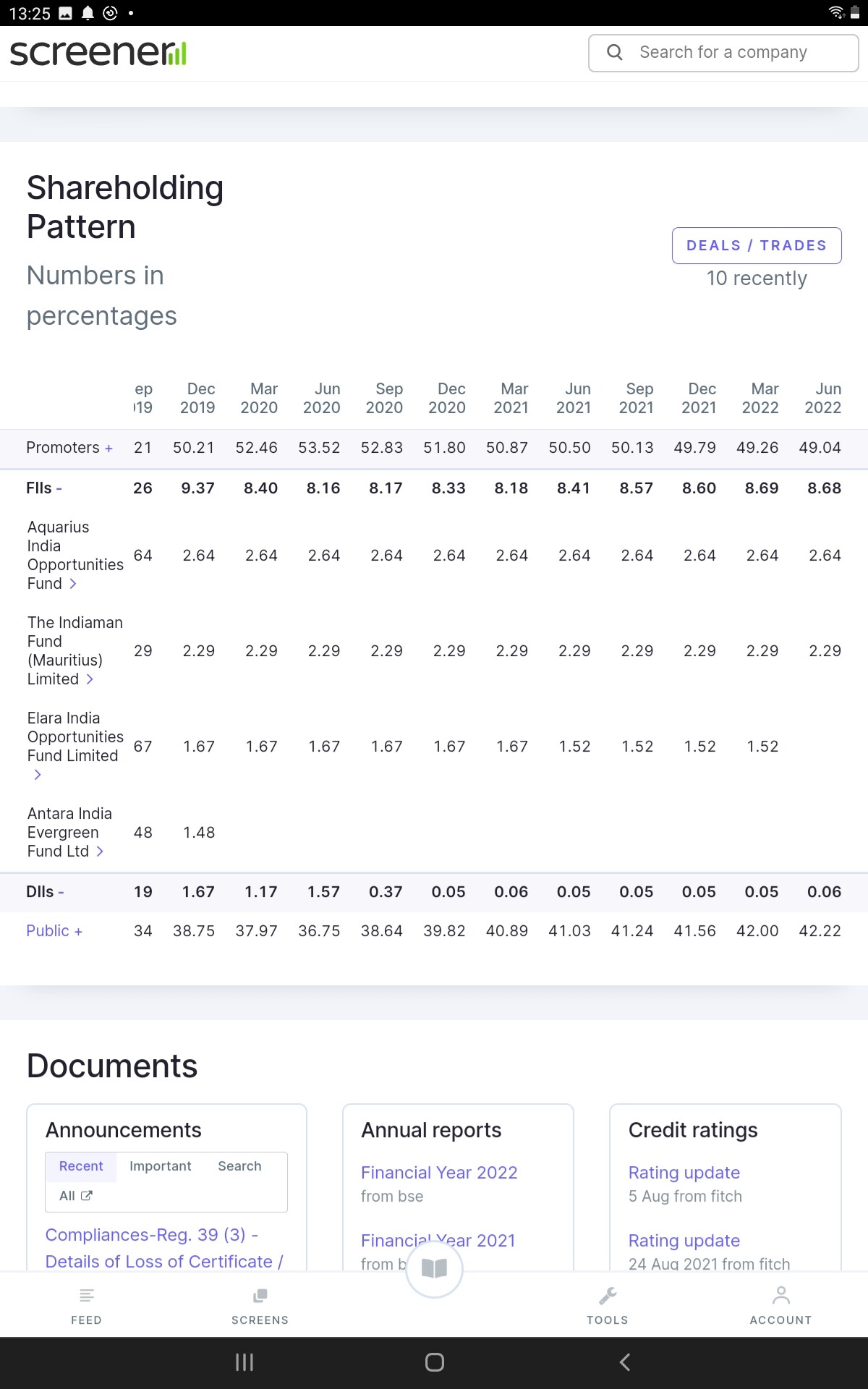

54.02% of promoter shareholding is currently pledged. Given the cleaned up balance sheet and strong cash flows, this should get cleared up pretty soon (ideally).

Though Rajeev Jhawar (MD) has been increasing shareholding gradually, Promoter shareholding has seen gradual steady declines. Bulk of the selling is seen from Prashant Jhawar controlled entities like Peterhouse Investments. Basically both Rajeev and Prashant are brothers and used to run the business together but due to some conflicts Prashant had to leave and thus becoming a non-operating promoter who had a substantial equity stake, Rajeev is increasing his stake but Prashant has been selling continuously. This is creating a supply overhang in the short term.

Prashant Jhawar shareholding is currently around 17% of shares outstanding, out of which 13% is pledged which cannot be sold (until revocation of pledge). The balance of 4% shares when sold, should get easily absorbed by the market, as has been the case so far (1.06% of unpledged equity is left with him)

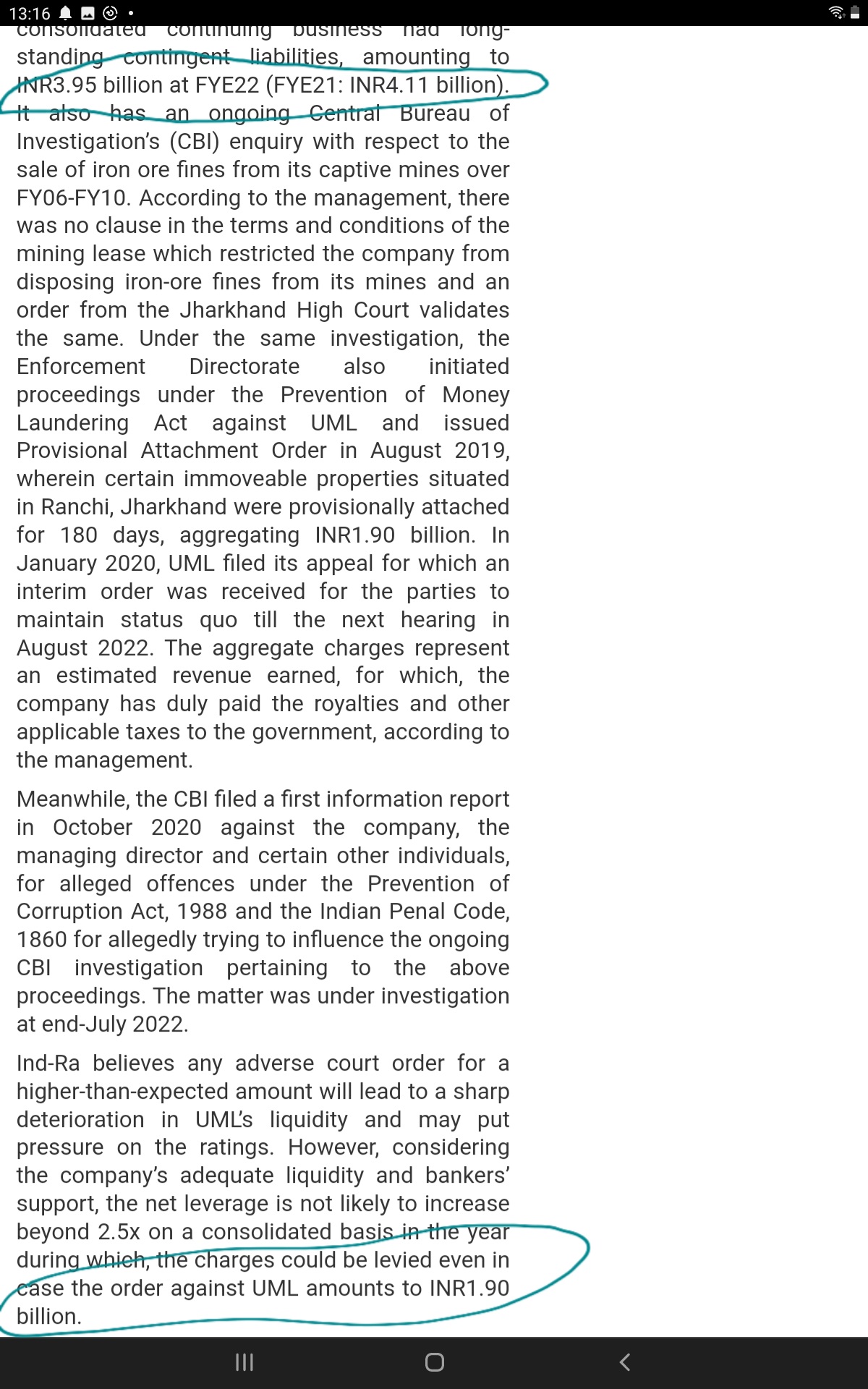

Contingent liabilities- The company is facing an ED case of 190 crores - The case is an old case related to iron ore export which the company had won in the High Court. But ED reopened the case in 2019 and attached assets of 190cr. Management is of the view that it has a very strong case. Even in the worst-case scenario, if the company loses the case, paying Rs.190 crores is not a challenge for the company at current cash flow levels. **Central Bureau of Investigation (CBI) Bribery case-**Usha Martin is facing a CBI case in which NMP Sinha a (recently) retired CBI officer was arrested accepting Rs.25 lakhs (allegedly provided by Usha Martin) from a middleman. Mr Sinha it is quoted in the reports as the same person (posted under the Economic offences wing of CBI as SP) who was earlier handling the Usha Martin cheating case against its mining arm. The CBI has made the company MD Mr Rajiv Jhawar accused, but the company has strongly denied the charges.

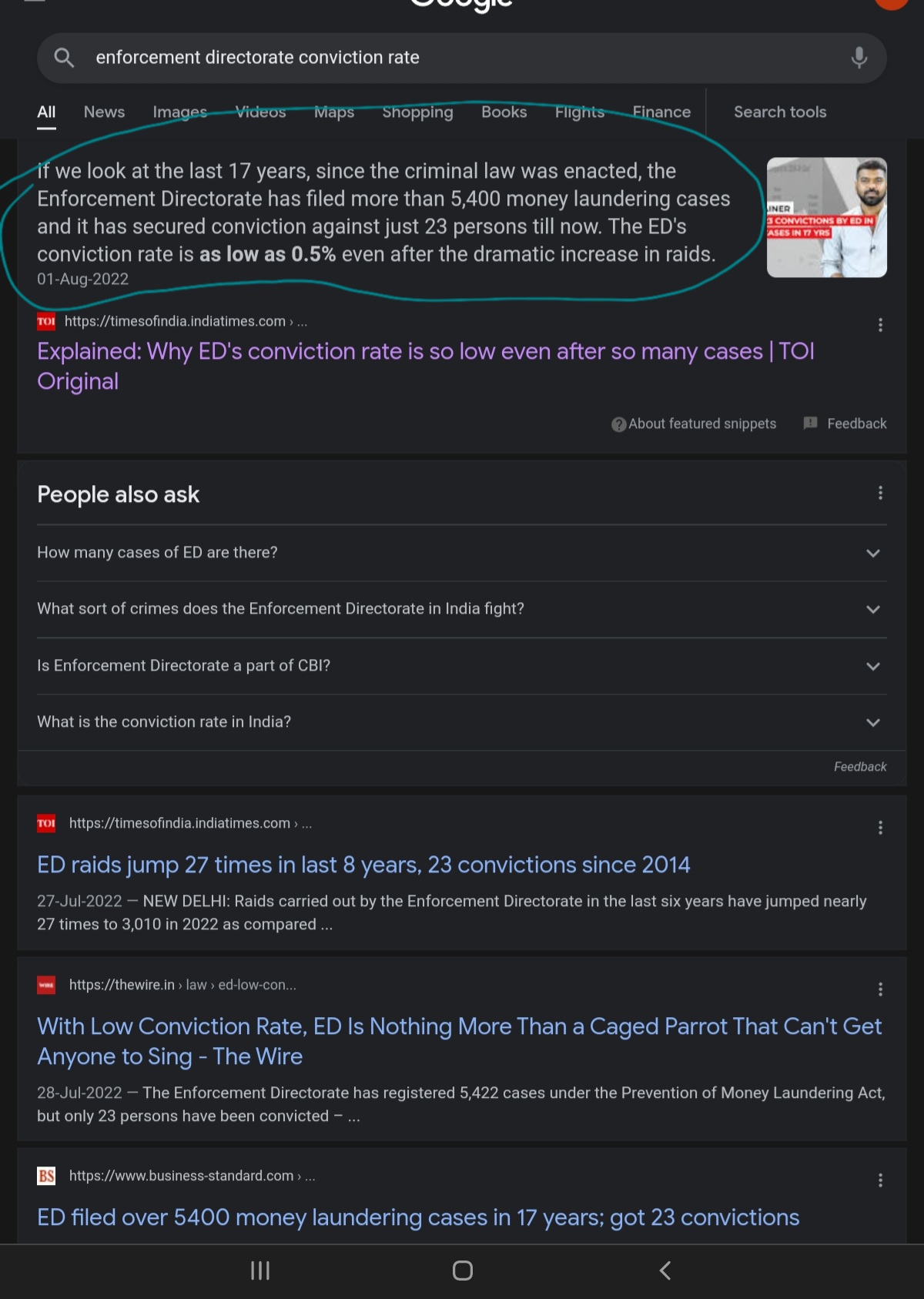

Should the ED case get dismissed in Usha Martin favour, the bribery case could automatically get shelved. ED and CBI cases are major overhangs on the stock. If & when these do get resolved in Usha Martin favor, UM could see higher participation from Institutional Investors.

Did many diworsifications previously after an upcycle to earn quick. If does capital misallocation again, may result in the same cycle of debt increasing and worsening the cash flows.

The related party transactions are high.

The trade receivables are increasing.

the writeup is a bit old and does not include the last 1-2 quarters of updates