its the non operating promoter who is selling, he is not left with much stake and soon the supply overhang will be done with in my opinion.

1 Like

yes, lets see how the company captures US market share as decided in the conference call

Outlooks From Credit Rating Report

-

Capacity enhancement of the plant at Ranchi, Jharkhand, which shall enhance its overall capacity in India by around 25% to 291,000 tonnes per annum (TPA).

-

UML also plans to enhance capacity at its Thailand plant by 8% to 39,000TPA.

-

The capacity expansion plan also includes adding new high-value,high-margin niche products to UML’s portfolio having a significant demand in the export market. Thus, the expanded capacities shall be more EBITDA-accretive than the existing operations once fully operational.

-

Most of the production is order-based, UML has been able to pass on volatility in raw material prices, albeit with a lag, as reflected in its range-bound EBITDA per tonne.

Disc: - Invested and I am No Reg. Advisor and Not an Recommendation.

7 Likes

Results out for Q1-2024

At the outset, the results look flat. On QoQ margins fell down but YoY improved.

Link for Q1:

Link for Investor presentation:

ConCall on: August 8, 2023 at 5:00 PM (IST)

Usha Martin Q1FY24 (other than financial numbers)

- Wire Ropes Volumes increased while LRPC , steel wires volume decreased

- Within wires ropes contribution of speciality (value added) wire ropes increased from 65 to 71%

- Exports marginally higher (56 vs 55)

- YoY EBIDTA margin (18 vs 15.5)

- Marginal Decrease in volume. This quarter is more of a value growth.

Product mix playing out as per management guidelines.

7 Likes

Key Information noted from Aug-23 Presentation

-

Segment wise contribution to overall volumes

Q1FY24 :Wire Rope – 52% (PFY 49%); Wire & Strand –16% (PFY 19%); LRPC – 32% (PFY 32%) -

Q1FY24 Operating EBITDA stood at Rs. 145.7 crore as against Rs. 117.3 crore, higher by 24.2% on a Y-o-Y basis.

-

Slide Indicating Raw Material Price Fluctuations and EBITDA co-relation.

Raw- Material and EBITDA.pdf (99.2 KB) -

Expansion at Ranchi is on-track and is expected to be completed by end of Q3

-

Key - Monitorable :- Volume Growth in the Ropes which is higher margin product.

Disc : - Invested and I am No Reg. Advisor and Not an Recommendation.

3 Likes

1 Like

Usha Martin Q1 concall highlights-

Offers wide range of-

Specialty Wire ropes

High Quality Wires

LRPC wires

Bespoke end fitments, accessories & related services

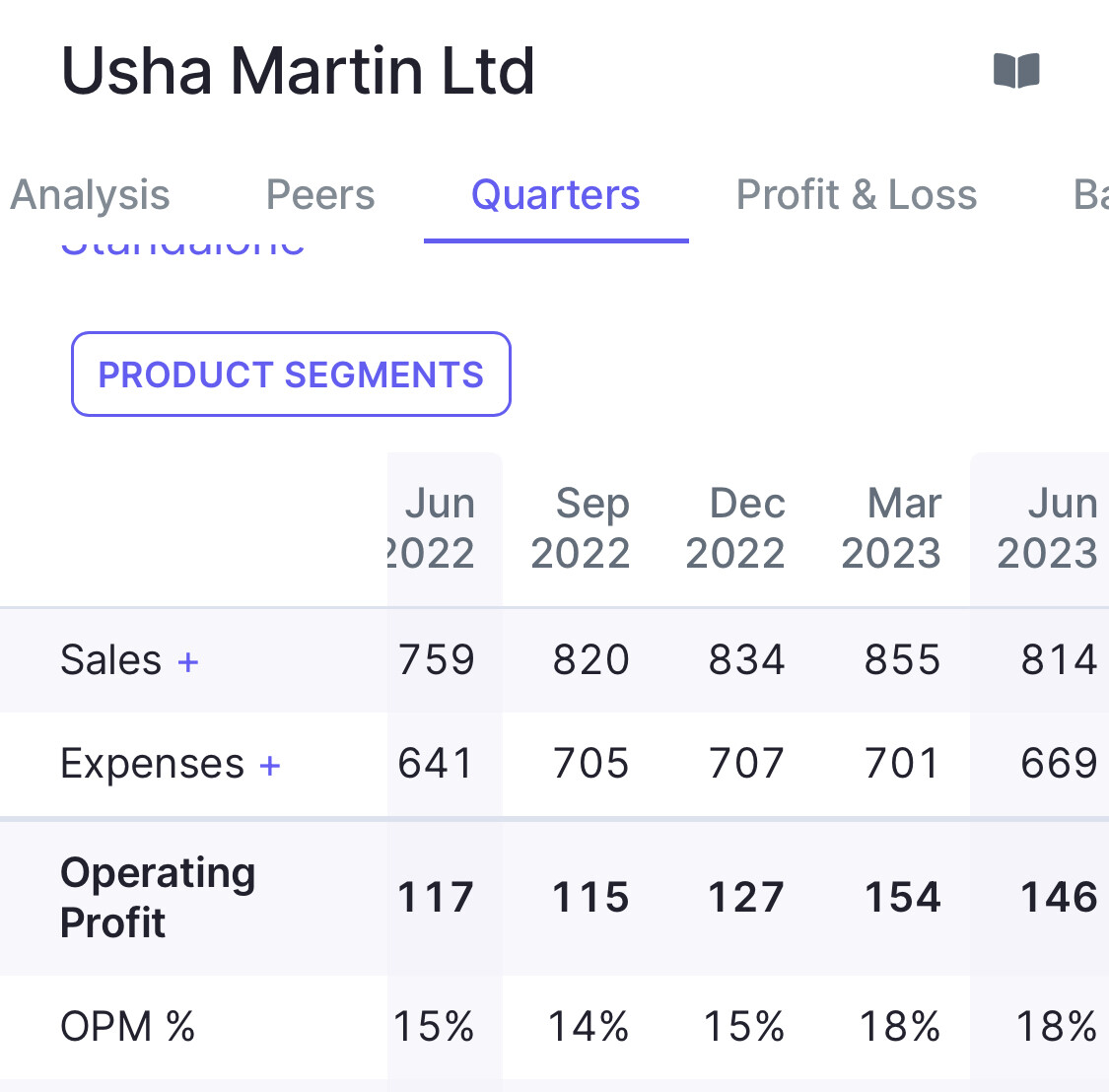

Consol Q1 outcomes-

Sales- 814 vs 760 cr

EBITDA- 146 vs 117 cr ( margins @ 17.9 vs 15.5 pc )

PAT- 101 vs 82 cr

Segmental revenues -

Wire ropes - 553 vs 481 cr, up 15 pc yoy

Wire and Strands - 65 vs 86 cr, down 24 pc yoy

LRPC - 116 vs 148 cr, down 22 pc yoy

Segment wise sales contribution -

Wire Ropes - 68 vs 67 pc

Wire and Strand - 8 vs 10 pc

LRPC - 14 vs 15 pc

Increase in rope sale in line with company’s strategy to focus on value added products

Volume wise data -

Wire Ropes - 23k vs 21k MT

Wire and Strands - 7k vs 9k MT

LRPC - 14k vs 17k MT

Geographical sales breakdown -

India - 44 pc

Europe - 24 pc

America - 7 pc

Middle East & Africa - 11 pc

Asia Pacific - 14 pc

In Q1, within Wire Ropes the share of speciality ropes ( for cranes, elevators, oil & offshore, mining, fishing ) increased from 65 to 71 pc

Revenues increased in Q1 despite YoY fall in RMs due better mix of value added sales

Exports in Q1 were up 13 pc

Nett Debt down to 99 cr vs 185 in Mar 23 despite 68 cr of Capex spend in Q1 - due very healthy cash flow generation

EBITDA / Ton @ Rs 32230 vs 26470 in FY 23 vs 19625 in FY 22 vs 15880 in FY 21

Committed to maintain > 18 pc EBITDA margins

Intend to improve the margins further as the product mix improves

As wins new international customers, margins can improve significantly. Current guidance is conservative

New wire ropes Capex to be concluded by Q3. Fresh volumes to start flowing in from Q4

Full ramp up to happen in 3-4 Qtrs

LRPC realisations are under pressure due capacity additions from Jindal Group, Tata Steel. Company now focussing on plasticated and galvanised LRPC products to differentiate and to add value

Hope to be Debt free by end of FY 24

Ranchi capex of aprox 350 cr to be completed by Q3. Has the potential to add 800 cr of annual sales at full capacity. Also, the products breakup from this new capex will favour the Higher Margin Speciality business

Chinese are not significant players in the value added segments

Guiding for 13-15 pc volume growth this yr and next yr despite volume contraction in Q1 !!!

Globally, Wire Ropes are growing at aprox 5 pc / yr. Company is gaining mkt share in international Mkts due better pricing vs Intl players and increased efforts towards customer service

Company’s global Mkt share is 5 pc. Intend to take it to 7-8 pc in medium term

Also looking to add value in the Wire segments for both domestic and export Mkts. This is also a huge mkt and can offer a lot of growth opportunities

In 2-3 yrs, EBITDA margins can be upwards of 20 pc due continuous focus on value additions

Disc : holding, biased

6 Likes

Hello all,

Wanted to get an understanding of the valuations and current valuation levels.

You see, from March2020 to March2023 the valuation has risen between 13-34 times, but the growth in EPS be it QOQ, or QYOY or just YOY does not in any way support this increase in valuations.

Now, I also looked at the revenues, the growth there is nothing that supports current levels of valuations.

One can suggest that “its the back to 2020 levels” theme getting played out.

March 2020 EPS stood at 13.74 and its just 11.49 in March2023 (Mar21 : 4.91, Mar22: 9.56).

Revenues have also growth from 2100 in March2020 to 3268 in March2023, so, about ~50% growth.

Yes there is reversal and growth, but a growth that supports valuations that went from 10-25/share to 348/share as of today?

There also has been a margin expansion from 11% in 2020 to now 16% in 2023. Some quarters have shown 18%. But are we sure even doubling or margins gets us this high of valuations?

I did consider the future prospects and how valuable the product could be, yet such a growth in valuations seems to show that market and participants are expecting the company to evolve in a way that borders and maybe has crossed the exuberance and hubris.

I see many a names that are invested and I ask you all to correct me if I am wrong.

Edited to add this :

I saw a similar thing happening in Dreamfolks and a few other names. The underlying business dynamics in no way supported the valuations.

Hence, I decided to ask the members before forming any opinions.

tl;dr

Trying to understand the logic behind current valuations.

March 2020 :

Revenue 2154

OPM% 11%

EPS 13.74

March 2023 :

Revenue 3268

OPM% 16%

EPS 11.49

March2020 - Closing Price 16

March2023 - Closing Price 214 (13x of 2020)

July2023 - Closing Price 337 (21x of 2020)

Seems extremely overvalued.

Business Fundamentals do not and can not support these valuations, which continue to grow still.

Would like to be proven wrong.

1 Like

March 2020 income includes ‘Other income’ of 520 crores from sale of Steel plant. Please exclude it from your calculation.

Sure, removed.

Yet the point stands.

Excluding the Other Income as you pointed out, the EPS comes to about ~2.1.

EPS in 2023 is ~12, so 6x.

Yet as I pointed out the valuations are 13x at the lower to 21x at the higher side.

How should I see it?

Taking Price immediately after covid crash as the base is incorrect. If you take Jan/Feb price, it was around 25-30. Now EPS increased by 6 times and stock price increased by 10 times… so not totally out of whack, especially considering the vast improvement in fundamentals with significant reduction in debt, capex and improved business prospects. Market always discounts the future

Disclosure - Invested and hence biased.

3 Likes

I think you need to answer a few questions related to Usha Martin business before asking these numerical questions. ( and here too, if stock price worked on excel sheet or mathemtical calculations, all the statisticians and mahematicians in the world would be the billionaires. )

-

What were different segments of business in 2020?

-

What are the sales figures for the last few years? Which are the segments contributing to these numbers?

-

How have the margins panned out over the period in question?

-

How has the balance sheet and return ratios evolved over the period in question?

-

How is the consistency and predictability of the business now as compared to earlier. ? ( for that one needs to listen to concall and get a sense of the business. )

Usha Martin is a textbook case to understand an evolving multibagger when it was first put up by @Anant in this forum. You should first make an attempt to go through the threads ( we have two of them, one is Colloborators corner and the other one is older one)

Earlier Usha Martin was a company which had not gone anywhere with two warring cousins trying to get control of the company and wanting to run company in their own thought out way.

First real piece of good fortune/smart decision was sale of commodity steel business to Tata Steel. Secondly this was followed up by cleaning up of debt using the above sale proceeds. Third was focus and capex into the higher margin and much more predictable and steady wire ropes business, where company was in a dominant position and had global ambitions. Fourth was more transparency from management, with presentations and concalls, so that investors got an idea about the business and management intent and integrity.

If this transformation was to be summarised in a few words, it was a transformation of a largely commodity type of business into a more predictable business with global scale. Improvement in quality of earnings is a big trigger. This is a recipe for multibaggers and this kind of model can be used in future also to uncover potential winners. One needs to have an open mind to see and accept the changes without getting caught up in numbers.

Beauty lies in the eyes of the beholder. Same thing applies to valuations. Something that appears expensive might appear to be reasonable for others and that is the only reason why there is a buyer for a seller most of the times. ![]()

40 Likes

“Beauty lies in the eyes of the beholder. Same thing applies to valuations.”

Yet there are limits to what market participants, as a whole group, accept to be unwise or flat out wrong.

Triple digit P/Es, High D/E, Promoter Selling (Shivalik) and multiple such aspects.

I have gone through the company and the product is sticky, very sticky, I agree with you there, BUT exuberance is dangerous.

World is very quickly moving towards AI and ML being the norm, real disruption. Yet is anyone willing to pay 50-100xP/E for our top IT companies? Of course not, and it is clear top IT names will enjoy the fruits of this revolution. So, there is a limit to your statement about someone finding something valuable which is considered bad by others. Subjective Preference can not escape reason for long, which is what I fear seems to be the case here.

Hence, it is confusing to see why such big benefit of the doubt for Usha Martin and not for other names who fall in similar trends, demography and industries.

I really like the product, its such an obvious winner, but buying a not so great company at great valuations is better than a great company which is valued this way - 6x EPS growth and 10x valuation growth.

Edited to add this :

Appreciate your comment Hitesh. Been through the threads you mentioned, will do so again.

What makes you so sure that the market was totally correct about Usha martin in March 2020 ? Is it simply to take the lowest price point and increase the X in your argument ??

Also our IT companies are mostly manpower replacement companies .While all of them quickly has added AI/ml to all the sentences they speak publicly, any actual AI disruption will only reduce their business since they are not into the development of AI but only users .

3 Likes

I still cannot understand your grouse against Usha Martin except for the run up in prices and the valuations… Regarding benefit of doubt, what is the doubt regarding this business? Valuations is something given by markets, which is a collective wisdom of a lot of market participants.

And this ML and AI and IT companies comparision is not apple to apple comparision.

I suggest you attempt to answer the questions I put up and you will understand the transformation this company has gone through. And this transformation in business has been well received by investors and there is a change in perception towards the company.

There was a similar situation in case of Ajanta Pharma, back in 2010-11 when it used to quote at 5-7 PE for nearly 3-4 quarters inspite of consistently reporting 25-35% CAGR in profits. And once perception changed, stock went up 60 times in a matter of hardly 4 years and stock used to quote at 35 PE… That’s how markets work and that’s how multibaggers happen.

Idea should be to learn how multibaggers evolve and have an open mind without any pre conceived notions of our own.

Usha as of now might be richly valued, but when perception regarding a company changes, valuations can sustain high levels as long as growth continues, and promise of further growth is visible.

The key determinants of high PE being accorded to any company are

- Opportunity size. this provides run way for growth.

- Scalability. Here execution of management comes into play.

- Balance sheet and return ratios.

- Management quality.

- Competitive advantage.

There may be more factors at play for above PE equation, but these are the ones that immediately come to mind.

40 Likes

One assumption in this debate is that the price of Usha Martin in 2020 was “fair”. The other assumption is that the p/e rerating should happen at the exact rate as growth.

But p/e is awarded by market on expectation of future growth and it often goes to stratospheric levels till the expected growth materialises before inevitably turning into a consistent compounder or tumbling back to its historical p/e.

Usha Martin made a transition from a company that was valued according to the commodity cycle to a company that makes value added products. Plus the cleaning up of debt allowed for market to be more optimistic. One thing I’ve learnt is that if a stock has gone 5 times it does not mean it can’t go up 5 times more. The irrationality of the market is the only way money is made. More often that not, the market takes it to 20 times and then retail investors who are gullible enter and then it falls 50 percent.

Whether to invest in Usha Martin at current levels is a matter of personal evaluation but it doesn’t really make sense to question why it has gone up so much.

12 Likes

There have been value investors in the forum, who even calculate fair value of a business based on many models. So if you are one of them, then you are true to the name of the forum, literally, and as such, you can participate in other stories, where there is not much action, and as such, being first among few, can reap equal benefits if not more, as growth investors or GARP investors, BAAP investors do.

If you are new, then I can say from my limited experience, market is a place which defies math and physics for extended periods of time like Keynes said, purely based on greed, and FOMO which in this day and age is available abundant. If you are not new, then I guess you are a value investor like Walter Schloss.

And there have been many stories in VP where there was excitement, an optimistic narrative, when the price is going up, with some voices reminding of caution, and when a fall happens, the narrative changes, some voices say the proverbial ‘i told you so’. And this has happened in both strong businesses and shady ones.

No investing in the business, just saying, although I was intrigued by the discussion, because Dr. Hitesh replied to you, who I know have seen a lot of things over his long journey, multibaggers one among them.

2 Likes

It is indeed valid to understand things from a valuation point of view.

The doubt is not the business, but simply whether the market has been giving too rosy of a future image for the company BASED on the current valuation.

My aim is to simply understand “Why?”. Even though most replies to my query have been biased investors (as mentioned by their disclosures), you all have shared some interesting points.

Like I mentioned before, the issue is NOT with the company, BUT the market perception Hitesh.

If ML & IT is not an apple to apple comparison, so is Pharma. Also, again, I emphasis, my query is about valuations and not the company and the demand for its product or its future prospects.

1 Like