as per news upl will be out of nifty 50 next year

Increased debt by over 9000cr this quarter… not a great sign for a highly indebted company with commodity price headwinds. Sold position.

2 Likes

UPL is trading close to bottom of cycle… question is how long this would continue. Bought to play the cycle

as the interest rates in US start to decline, the profit will start to inflow.

2 Likes

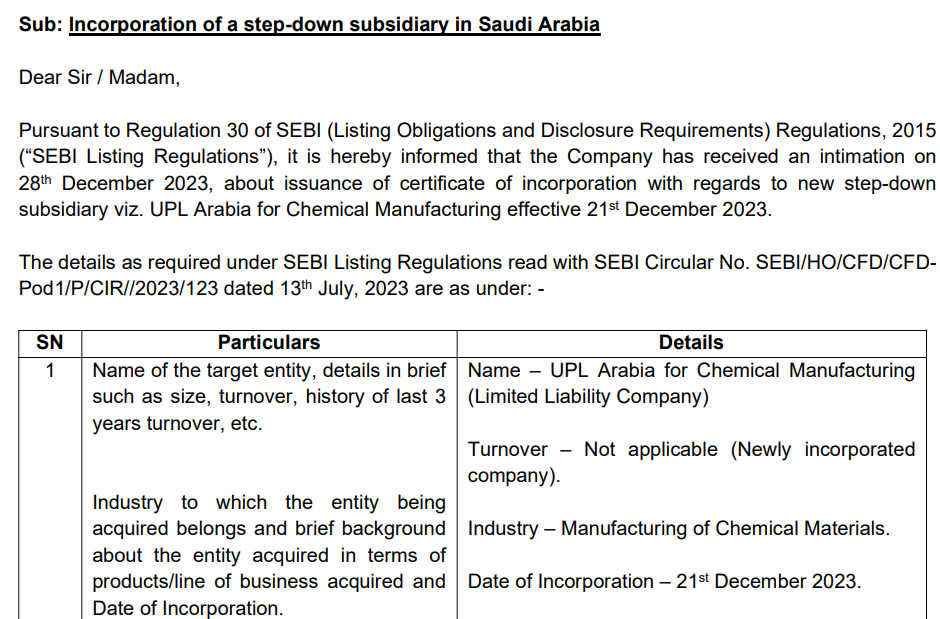

UPL had acquired some stake in Clean Max Kratos Pvt Ltd to foray into renewable energy. And now they are in the list of 14 companies interested in setting up green hydrogen production facilities

1 Like

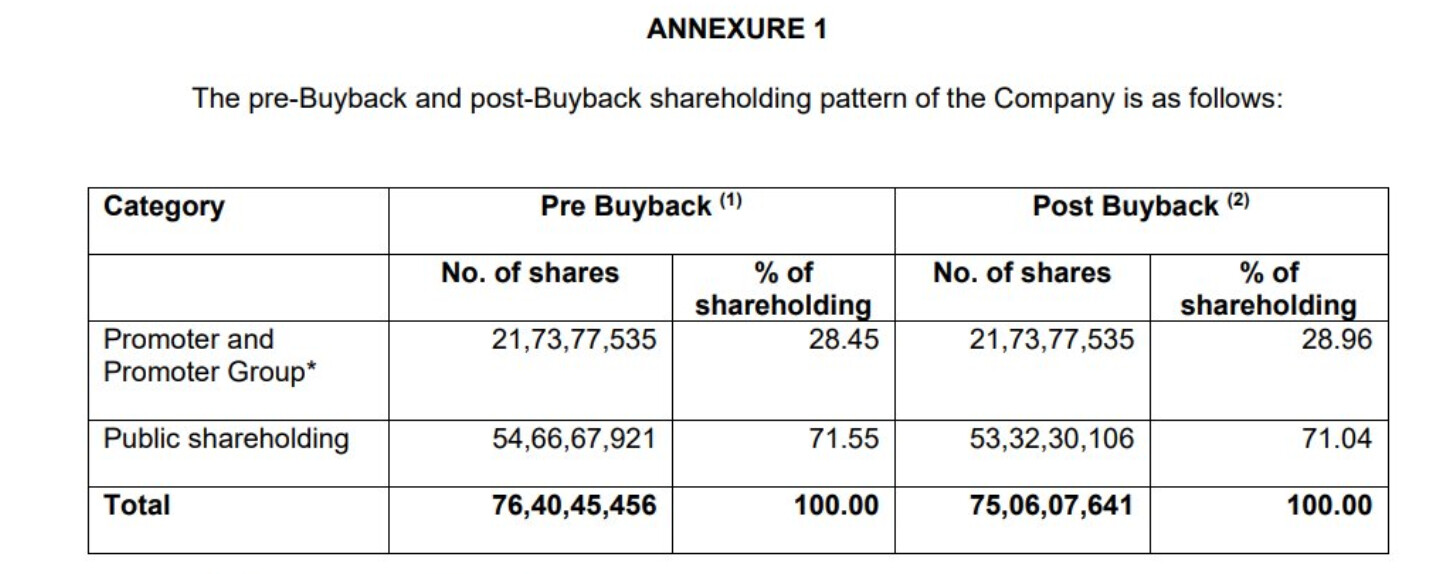

promoters didn’t participate in the buyback last year so some of the noise about corporate governance issue in the wake of current rights issues are not correct.

2 Likes

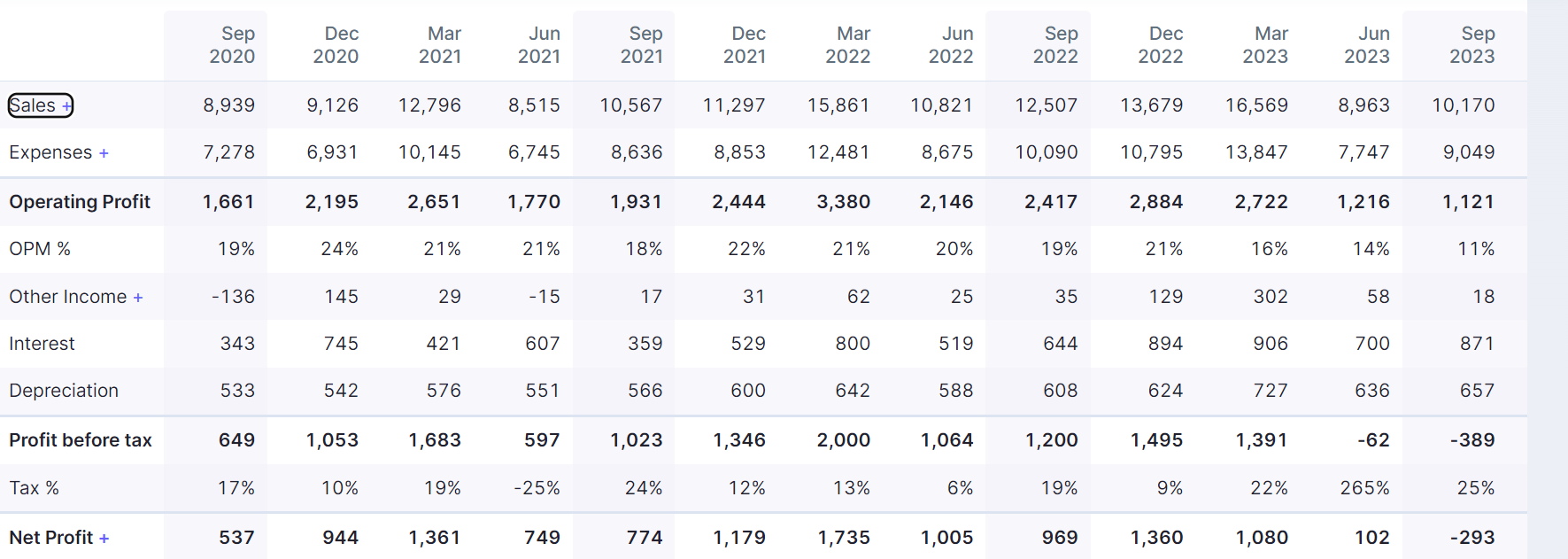

- The top line seems to be getting flattish

- OPM is now very close to single-digit

- High debt, so interest payments continue to balloon / low-interest coverage ratio

- Reported negative PAT in the last two quarters

EBITDA this year will probably be the lowest for them in the last five years.

I am unsure where this company is headed and whether the thesis continues to hold.

1 Like

Agrochemical firm UPL to raise funds up to ₹4,200 crore via rights issue (cnbctv18.com)

looks like funds rising for debt payment.

2 Likes

if you are sure that company would see through next 12-18 month without risk of default or in cas eof default , co anyways is values > current mcap , buy UPL stocks and hold. This is value investment.

disclosure: one of top holding in my pf

2 Likes

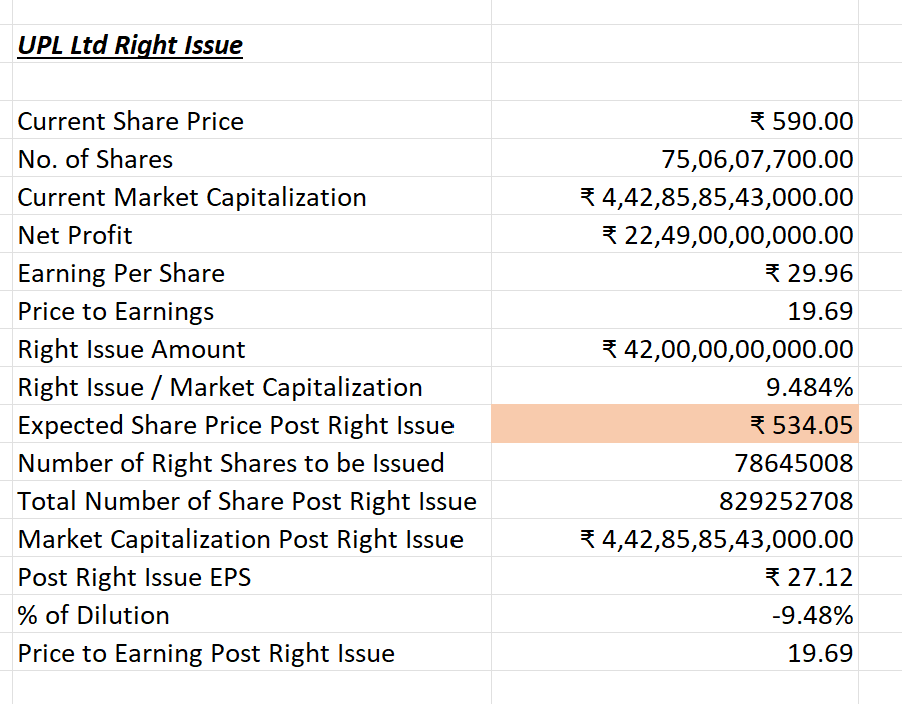

Was trying to calculate what could be the rights issue ratio and resultant EPS dilution. Pls suggest if this is the right approach:

4200Cr to be raised by rights issue Current marketcap around 43K; assuming around 10% discount to CMP; rights issue to be at around 540

4200/540 = 7.5Cr shares will be issued

Currently 150Cr Equity capital comprises of shares with Face Value of 2; that means currently 75Cr shares issued. with 7.5Cr more shares to be issued; equity base rising 10%; EPS should dilute by 9%.

I believe the underlying business is not yet out of the doldrums, the stock may ultimately reach the rights issue price in the coming quarter…

2 Likes

rights issue ratio could be around 1 share for 10 or multiples thereof. a slightly higher amount could be reserved for retail investors. If the issue price is at a significant discount to CMP, I would consider applying for extra shares. I feel the business should rebound in the next few years. what will happen to the stock? only the market knows!

I expect that UPL Ltd price falling within the range of 530 to 550, I aim to add more of it to my portfolio around these levels.

5 Likes

High D/E ratio makes UPL difficult to buy even at 530. Market never spare such high debt company in bear market. I am still figuring what is the attractive price to buy this heavy debt ridden company. One thing which comes in my mind is to buy close to its book value. but UPL has never gone below P/B below 1.5 in the past which is now the present value.

Disclaimer: Tracking with uncertainity in mind. Not holding. @rranjan @Amit_Jain3

1 Like

Thats crux of value investing. Unless there is a new info , i would be truck loading upl at book value.

Sector has headwinds , give it 6 to 12 month to get more clarity

2 Likes

How are you so comfortable with debt to equity ratio of UPl? I know that with reducing interest cost will certainly provide some relief to debt of company but any correction in this bull market will result in drastic fall in share prices. As far as business is concerned, it is right to wait for 1 years to pass the headwinds. Just trying to understand your frame of mind.

1 Like

This is not showing up on the exchange’s website. Hopefully no additional debt is taken to fund this.

Probably this is the reason behind the rights issue.

Worst result !! https://www.bseindia.com/xml-data/corpfiling/AttachLive/de32a4db-8182-45a7-947b-8362226eb54c.pdf

Anyone done detailed analysis - is worst over? what’s future for this excellent company once upon a time!

Bad results again by UPL. Missed the estimates by a huge shot. Debt’s interest cost is very high tbh

2 Likes