Surprised to not see a discussion on this company.

I guess that perceptions matter.

Anyway, UPL is one of the largest generic agrochemical companies in the world but more importantly, also one of the most profitable and most capital efficient.

Competitors are Adama, FMC, Cheminova, and all the IP-owning agrochemical companies such as Bayer, Sumitomo, Syngenta, etc.

The portfolio of products ranges from seed, seed care to pesticides, biological and organic chemicals and also post harvest crop care.

The company has one of the largest supply chains and manufacturing capabilities in the world- selling in all the major continents to 122 countries.

Unlike Indian formulation players (that are essentially asset-light and focused on the Indian market only) UPL’s key advantage is the diversified nature of earnings. So, 2 poor monsoons did not have a big impact on the company’s ops; then again, a great monsoon might also not impact the company much.

The biggest hurdles with the company are the asset heavy nature of its operations, scant disclosure of its global manufacturing footprint and also its reliance on a global supply chain (which the company actually believes to be a strong suit, since other global companies have either scaled back on their global supply and manufacturing abilities).

The key risks are from increasing global use of GM seeds which reduce depends on pesticides, bad debts in Latin America where receivables typically go to 190 days or so (as is the nature of that market), and an inability to match production & supply with global demand.

In addition to this, the company keeps spending on global product registrations which are expensive and time consuming.

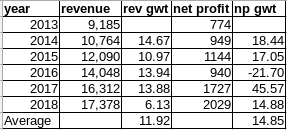

EPS has grown from 13.01 in FY12 to 30.31 in FY16

M Cap from 6000 cr to 25000 cr odd (Price: 130 to 590 odd)

ROE has moved from 19% to 22% over the last 4 years

In the process, it bought back about 7% of the o/s shares

The company is currently trading at 20 PE odd

Good focus on managing working capital and debt

And soon, it will complete its merger with its associate company, Advanta Ltd.

The concall transcript for that can be downloaded here: uplonline.com/Transcripts-Kotak-UPLAdvanta-23-Nov-2015.pdf

Post-merger, it will be a truly global company with global branding strategy and serving the entire agricultural chain.

Numbers are difficult to predict, but the management has proven itself to be very focused on profitability, stability, and risk management. They did give some sort of indirect guidance for the merged organization - PAT of 1800 cr for FY17 if the merger is complete by then.

And attached is a transcript of the recently held annual investor meet for FY16. This is a transcript that I commissioned, the video is available on youtube: UPL Capital Markets Day 2016 - Webcast recording - YouTube

UPL CMD 2016.docx (59.2 KB)

Best wishes doing your research!

Hope this begins an interesting discussion…

Discl: I am a shareholder of the company