What is the risk of default for UPL? With such high debt , I am currently comfortable to buy it at book value only.

Not invested: keeping a watch.

I think we can wait. As per management presentation expecting recovery from Q2FY25

1 Like

improvement in the chemical cycle and interest rates cut globally may lead to some positive results

The decline in revenue was majorly attributed to Destocking and lower demand in the European Union and the margins have been impacted due to high-cost inventory liquidation and higher rebates to support channel partners. The company mentioned that the business will be back to normal only after Q2FY25.

We have been witnessing a bearish price trend for the company and the same is expected to continue for the time being.

The company has, at last, realized that its main priority is to reduce debt and it will raise rights issue of up to $500 Mn to repay debt and explore other opportunities to repay debt.

4 Likes

This is what I am fearing for. Market wil beat such high debt ridden stock. Will only accumulate near book value. I rest my case here.Open for discussion.

3 Likes

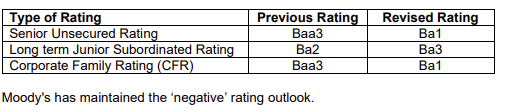

Noob question: With the recent rating downgrade will the interest cost rise for existing debt as well? Or will the higher interest cost (based on ratings) be applicable for fresh loans?

3 Likes

Fitch Downgrades UPL Corp to ‘BB+’; Outlook Negative

UPL’s weak performance mainly reflects sustained pressure from overcapacity in China.

UPL expects channel destocking, which has affected demand, to subside by 1HFY25. However, the outlook for capacity in China is more uncertain. We assume UPL’s product prices and margins to rise meaningfully from 4QFY24 on supply rationalisation in China in response to weak profitability. However, there is risk that the glut will persist for several years and constrain UPL’s EBITDA margin improvement.

1 Like

UPL out of the NIFTY50.

2 Likes

p/bv is al time low & EV/EBIDTA-11 Low to peers. Capex , share holding only 16% retail holding; OPM should mean to reversion. Inventory normalized, Q4 should be better. Margin of safety looks good. Price retest trendline july 2013 to mar 2024 on monthly line chart.

1 Like

Is it a value stock or a value trap though?

The main problem that has emerged recently is their high debt levels (incl. high working capital reqs.) which are significantly worsened in a soft worldwide agrochems market.

China is a big landmine, with excess capacity at home, they are dumping.

Demand may revive, but what about china?

Exclusion from index is also a bad thing.

Overall, it does not look like a good thing to buy or hold right now. The long term growth will also be slower this decade compared to last (perhaps high single digit). There is no visibility on when rate cuts will begin worldwide also.

IMHO this is not yet peak pessimism and more pain can be expected.

DISCLOSURE - just a lay person, i am also known to be an idiot, so …

6 Likes

UPL plans to launch an IPO for its seeds business named Advanta Enterprises in early FY25 as per CNBC TV18 report.

2 Likes

Outlook: Negative

CARE Ratings Ltd. (CARE Ratings) believes that though there could be an improvement in UPL’s performance in FY25 over FY24, its

business and financial risk profile may remain under pressure in the near term owing to the unprecedented challenges faced by

the agrochemical industry, especially if the pace of recovery is slower than envisaged.

UPL Expands Footprint in China

UPL announced today plans to increase its stake in Uniphos International China Limited (UICL) to up to 49%, thereby making it an associate company. This strategic move will see UPL’s subsidiary, UPL Hong Kong, invest up to USD 98,000 in UICL, which is engaged in the sale and purchase of crop protection chemicals. The investment will be made in phases.

UPL Q1 FY25 Analysis: Key takeaways!!

Business Outlook:

- Q1 FY25 revenue was flat at 1% YoY growth, with 16% volume growth offset by 14% price decline

- Management expects gradual recovery in crop protection demand and cost optimization to drive 4-8% revenue growth and >50% EBITDA growth in FY25

- H2 expected to be significantly stronger than H1 as high-cost inventory liquidation completes and margins normalize

Strategic Initiatives:

- Focus on differentiated and sustainable product portfolio, targeting 40% mix by year-end vs 33% in Q1

- Cost optimization targeting $100 million savings in FY25 through employee rationalization, lower travel/marketing spend, and shared services

- Restructuring India business with tighter credit policies to improve working capital and cash flows

- Rights issue expected to close by end of FY25, proceeds to be used for deleveraging

Trends and Themes:

- Channel destocking largely complete in key markets like North America and Europe

- Shift towards just-in-time inventory management by distributors

- Stabilization of input costs and crop protection chemical prices after significant declines in FY24

Industry Tailwinds:

- Strong farm-gate demand for crop protection products at or above last year levels

- Normalization of inventory levels in distribution channels

- Lower input costs improving margins

Industry Headwinds:

- Continued pricing pressure from Chinese suppliers, especially in commodity products

- Softness in agricultural commodity prices impacting farmer economics

- Higher freight expenses due to geopolitical issues

Analyst Concerns and Management Response:

-

Concern: Significant decline in Q1 EBITDA (-28% YoY) despite flat revenue

Response: Management expects margins to normalize in H2 as high-cost inventory liquidation completes and cost savings kick in -

Concern: Delay in rights issue timeline

Response: Clarifications sought by regulators being addressed, confident of completing by Q3/Q4

Competitive Landscape:

- UPL gaining market share in most key regions as demand normalizes

- Strong competition from Chinese suppliers in commodity products, but UPL leveraging India manufacturing base for cost competitiveness

Guidance and Outlook:

- FY25 revenue growth: 4-8%

- FY25 EBITDA growth: >50% YoY

- Cash flow from operations: $300-400 million

- Net debt reduction: $300-400 million (excluding rights issue proceeds)

Capital Allocation Strategy:

- Focus on deleveraging through improved cash flows and rights issue proceeds

- Evaluating monetization options for some business platforms

- Maintaining R&D investments in differentiated and sustainable products

Opportunities & Risks:

Opportunities:

- Market share gains in key regions as demand normalizes

- Margin expansion from cost optimization and lower input costs

- Growth in differentiated and sustainable product portfolio

Risks:

- Continued pricing pressure from Chinese suppliers

- Adverse weather conditions impacting crop seasons

- Geopolitical issues increasing freight costs

Regulatory Environment:

- Potential antidumping duties on some Chinese imports in India under investigation

- Increased focus on sustainable and bio-based crop protection solutions globally

Customer Sentiment:

- Strong farmer demand for crop protection products

- Shift towards just-in-time inventory management by distributors

- Increased interest in differentiated and sustainable solutions

Top 3 Takeaways:

- Volume-led growth (+16% YoY) offset by pricing pressure (-14% YoY) in Q1, but management confident of H2 recovery

- Focus on cost optimization, working capital improvement, and deleveraging through rights issue and improved cash flows

- Continued shift towards differentiated and sustainable product portfolio to drive growth and margins

4 Likes

Q2 FY25 Results and Concall insights.

| Particulars | Q2 FY25 | Q2 FY24 | YoY Change |

|---|---|---|---|

| Revenue | 11,090 Cr | 10,170 Cr | 9% |

| Profit Before Tax (PBT) | (447) Cr | (389) Cr | Loss Widened by 15% |

| Profit After Tax (PAT) | (585) Cr | (293) Cr | Loss Widened by 99% |

| Basic EPS | (5.90) | (2.54) | Decreased by 132% |

| Diluted EPS | (5.90) | (2.54) | Decreased by 132% |

| Debt to Equity Ratio (times) | 1.01 | 0.99 | Increased Slightly |

YoY Changes (Q2 FY25 vs. Q2 FY24):

-

Revenue: A 9% increase year-on-year, driven by a 16% volume growth that offset a 7% price decline. This positive trend aligns with the company’s continued focus on increasing market share through volume-driven growth.

-

PBT: The consolidated loss before tax widened by approximately 15%. While revenue grew, factors contributing to this increased loss might include higher fixed overheads (up 5% YoY), increased finance costs (up approximately 3% YoY) potentially due to higher SOFUR rates and a lower credit rating, and a less favorable foreign exchange impact (a loss of 375 Cr compared to 229 Cr in the previous year). The increase in provision for expected credit loss (ECL) due to a customer filing for Chapter 11 in the LATAM region also likely played a role.

-

PAT: The consolidated loss after tax saw a substantial increase of roughly 99%. This is likely due to the combined effect of the wider PBT and the non-recognition of deferred tax assets (DTA), potentially reflecting the company’s conservative approach in the current economic environment.

-

EPS: Both basic and diluted EPS declined considerably (approximately 132%) year-on-year, reflecting the amplified losses incurred in Q2 FY25.

-

Debt to Equity Ratio: A slight increase year-on-year, suggesting a marginal shift towards a higher reliance on debt financing.

Other Key Metrics (Q2 FY25 vs. Q2 FY24) from Consolidated Data:

-

EBITDA: Remained relatively flat, with a slight improvement compared to the 28% decline observed in Q1 FY25.

-

EBITDA Margin: Decreased, likely influenced by the drop in prices and regional mix.

-

Net Working Capital: Reduced significantly compared to the same period in the previous year. This improvement stems from effective inventory management, resulting in a reduction of 18 days in inventory days.

-

Net Debt: Decreased by $411 million year-on-year, aided by reduced working capital requirements and lower capital expenditure.

Additional Observations:

-

UPL expects continued business momentum in the second half of FY25, leading to favorable results.

-

The company aims to achieve operational free cash flow of $300 to $400 million, which will be allocated to reduce outstanding debt.

-

Efforts to unlock value in its subsidiary, Advanta Enterprises Limited, are underway through various options including fund raising.

Summary of UPL Limited’s Q2 FY25 Earnings Conference Call

The following is a summary of UPL Limited’s Q2 FY25 earnings conference call held on November 11, 2024. The summary includes key insights and questions from analysts and investors, along with the responses provided by UPL’s management team.

Global Crop Protection Business Update

- Mike Frank, CEO of UPL’s global crop protection business, provided an update on the market and financial performance.

- He stated that the global crop protection market was experiencing mixed conditions with destocking nearly complete but continued price pressure.

- He highlighted the strong volume growth across regions like Latin America and Europe, driven by strong performance in fungicides and insecticides.

- He acknowledged the compression in contribution margin due to price declines, primarily in Latin America, and unfavorable mix in Europe.

Regional Performance

- Mike Frank provided insights into the regional performance, specifically highlighting the challenges in Latin America due to a large distributor filing for Chapter 11 bankruptcy.

- He mentioned that the company was closely monitoring the situation in Brazil, where grower margins continued to be squeezed, and was taking steps to mitigate the risks of bad debt and write-offs.

Outlook for Q3 and FY25

- Mike Frank expressed optimism about the outlook for the remainder of the fiscal year.

- He anticipated normalized margins in the second half, driven by lower input costs, improved product mix, and higher market share in key regions.

- He emphasized the company’s focus on SGNA discipline and operational efficiency.

- He also highlighted the strong pipeline of new product launches, particularly in the differentiated and sustainable segments.

Other Business Updates

- Anand provided a brief update on the other business platforms:

- UPL Sustainable Agri Solutions Limited (India Crop Protection): Strong rebound in Q2 with 20% YoY revenue growth and significant improvement in EBITDA margins.

- Advanta Seeds Limited: Good improvement in Q2 with 4% revenue growth driven by margin accretive growth in grain sorghum and corn.

- Superform (Specialty Chemicals): Reported as part of UPL Limited for the quarter.

Q&A Session

The Q&A session covered various topics, including:

Guidance

- Sorup Jim from HSBC inquired about the revenue guidance for FY25.

- Anand confirmed that the company was maintaining its revenue guidance of 4-8% YoY growth.

- Analysts also questioned the feasibility of achieving the 50% EBITDA growth guidance.

- Anand and Mike Frank explained that the guidance was based on multiple factors, including lower input costs, improved product mix, recovery in high-margin regions like the US and Europe, and the absence of the one-off impact related to rebates and inventory mark-to-market adjustments experienced in the previous year.

Rights Issue

- Angel Sense from Prudent Asset Management and Lynn from BNP Paribas inquired about the status and timeline of the rights issue.

- Anand stated that the company was prohibited from commenting on the timing of the rights issue due to regulatory restrictions. He assured analysts that the company would provide relevant updates as per SEBI guidelines at the appropriate time.

- He later mentioned that the Board had approved a revised amount of $400 million for the rights issue.

Advanta Monetization

- Angel Sense inquired about the progress on the potential monetization of the Advanta seeds business.

- Anand stated that the process was ongoing, with the company working on the necessary documentation and financial details. He stated that updates would be provided as the situation progressed.

Debt Refinancing and Rating

- Analyst: Lynn inquired about the progress on refinancing short-term loans and the communication with Moody’s, which had placed UPL on negative watch.

- Response: Anand confirmed that arrangements for refinancing had been made, though he could not disclose the terms. He stated that the company was in constant communication with Moody’s and all other rating agencies, providing them with transparent information about the company’s performance and the industry outlook.

Regional Revenue Discrepancy

- Sorup Jim from HSBC pointed out a discrepancy in the reported revenue growth for the Rest of the World region between the consolidated UPL level and the UPL Crop Protection segment.

- Anand agreed to follow up with the analyst separately to clarify the discrepancy.

Impact of US Political Landscape

- Steve Bryan from Bank of America asked about the potential impact of a change in US trade policy, particularly regarding tariffs on Chinese exports.

- Mike Frank believed that any policy changes aimed at reducing dependence on China could potentially benefit UPL as an India-based manufacturer. He added that the company was prepared to capitalize on any opportunities that arose in North America.

Biologics Pipeline

- Steve Bryan inquired about UPL’s pipeline for biological products, following the strong growth witnessed in that segment.

- Mike Frank highlighted the robust pipeline for bio stimulants and biocontrol products, emphasizing that over 80% of the $85 million targeted new product revenue in FY25 would come from differentiated or sustainable products, including biologicals.

Gene Editing in Seeds

- Steve Bryan asked about the potential impact of evolving regulations on gene editing in seeds, particularly in Europe.

- Bupin Dubay, CEO of Advanta Seeds, acknowledged the benefits of gene editing technology. He noted that while the regulatory pathway was becoming clearer in Europe, some uncertainties remained, and the industry was still seeking further clarity.

Quarter-on-Quarter Trends

- Lynn asked for details on the quarter-on-quarter changes in volume and price.

- The management team did not provide specific quarter-on-quarter figures but clarified that the presentation primarily focused on year-on-year comparisons.

Receivables and Factoring

- Lavanya Sharma from JP Morgan inquired about the trends in receivables, particularly in Brazil, and the outlook for factoring in Q3.

- Mike Frank explained that while the situation in Brazil posed some risks, the company expected improvements as the soybean planting season progressed. He highlighted that growers and distributors were currently purchasing products closer to the time of need, resulting in a healthier order book for UPL.

- Anand added that the company’s factoring limits remained intact and that they were strategically using factoring to manage credit risk and improve collections. He also noted that approximately 50% of the outstanding factoring was related to Brazil.

High-Cost Inventory

- Vikas Arora from Bank of America asked about the remaining balance of high-cost inventory.

- Anand estimated that the remaining high-cost inventory was less than $20-30 million, out of the total inventory of approximately $1 billion.

Drivers for EBITDA Growth

- Vinit Ahuja from BlackRock inquired about the key drivers for the 50% EBITDA growth guidance and whether the improved inventory management played a significant role.

- Anand explained that the guidance was based on several factors, including the absence of the one-off impact of rebates and inventory mark-to-market adjustments experienced in the previous year. He also highlighted the benefits of having fresh inventory at lower costs, improved inventory management, and higher sales of differentiated products.

Inorganic Growth Opportunities

- Vinit Ahuja asked for updates on inorganic growth opportunities, particularly regarding the seeds business, given the anticipated recovery in the industry.

- Anand stated that the company continues to explore various opportunities, including those related to the seeds business, but refrained from providing specific details due to the sensitive nature of such discussions.

Regional Outlook for Next 6-12 Months

- Analyst: Samuel Shen from Alliance Bernstein inquired about the management’s outlook for different regions in the next 6-12 months.

- Response: Mike Frank expressed optimism about North America, highlighting the potential benefits from the US government’s focus on supply chain resilience and potential investigations into anti-competitive behavior in the market. He also expressed a positive outlook for Europe, citing opportunities for growth in both traditional and bio solutions segments. Regarding Latin America, he acknowledged that the region was currently facing some challenges but maintained a cautiously optimistic stance.

Overall Impression

The conference call conveyed a message of cautious optimism from UPL’s management. While acknowledging the challenges faced in the first half of FY25, including pricing pressure and the impact of the distributor bankruptcy in Latin America, they expressed confidence in the company’s ability to achieve its guidance for the full year, driven by lower input costs, improved product mix, new product launches, and operational efficiencies. The management team also highlighted the company’s focus on working capital management and debt reduction, along with its commitment to exploring inorganic growth opportunities.

Note: Content include AI summarized notes of Investor Presentation, concall and other reports.

Disclosure: Not invested. Post purely for study purposes. thanks.

4 Likes

Rights issue by UPL

3 Likes

I was seeking some guidance to understand what’s the most effective way of utilizing the upcoming Rights Entitlement (RE) for UPL.

Supposedly if someone owns 80 shares of UPL then with 1:8 ratio they will be entitled for 8 RE shares and basis their holding average, they can decide whether to encash the REs during trading days or use them to receive additional shares at lower price.

What would be the short term and long term scenario for an investor and trader both with the current market price? Can someone please throw some light?

Thank you!

1 Like

is UPL finally out of red ? profitable after 6 quarter (barring one quarter of 30 cr profit in between)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/9ccc27f9-3dbb-4e1c-98b1-91ada20d937c.pdf

i will wait for con call but then if it has tuned around, we are in good up move over next 4 -6 Q.

3 Likes

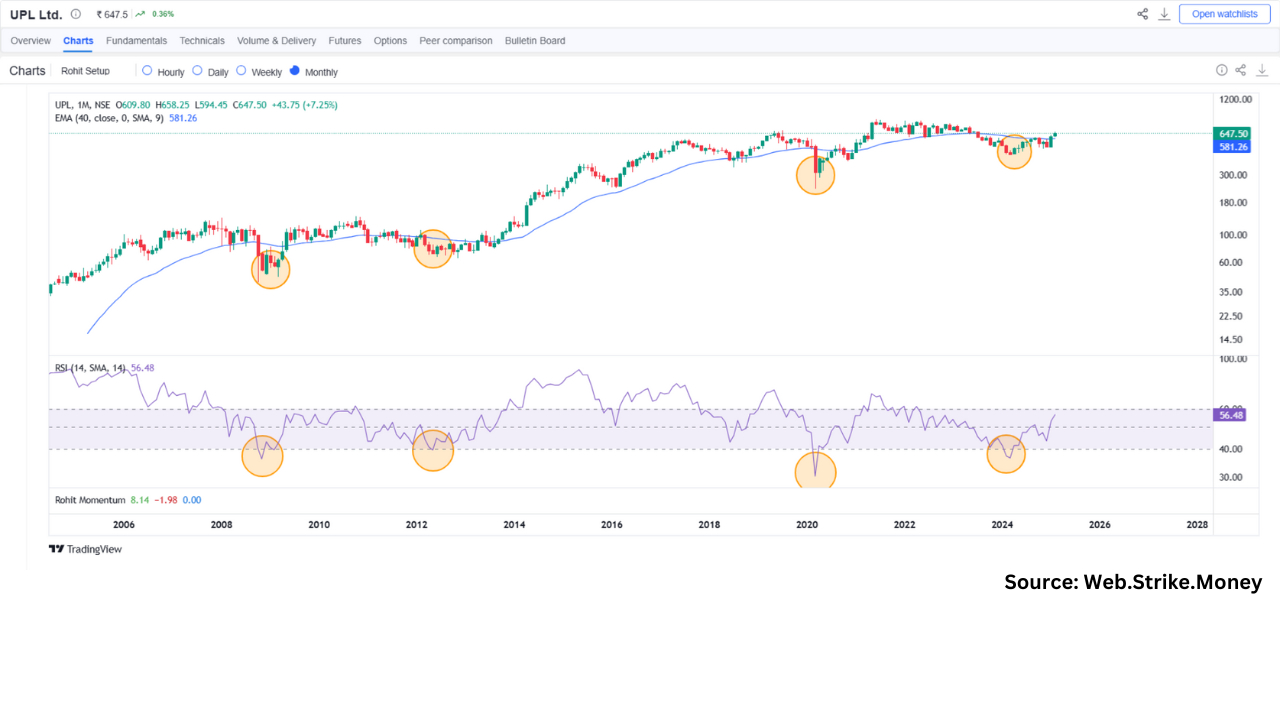

Technically, I believe UPL is a strong stock, and the best time to buy or invest is when its monthly RSI drops below 40, indicating extreme oversold conditions. Historically, UPL has reversed into a bullish trend each time its RSI has fallen below 40, though this has only happened four times since 2007.

Most recently, in March 2024, UPL once again became oversold, with its monthly RSI dropping below 40, forming a bottom along with an inverse head and shoulders pattern. However, for the stock to move upward, it must break through its resistance level.

Let me know your thoughts!

While this is delayed, they have recently sold some stake in Advanta which makes it overall valued at $2.8 Bn which is a little steep, but here are 2 key triggers:

- EU is working to ease their regulatory framework wrt to gene edited seeds, is beneficial as they are one of the bigger non China players in this space.

- They are launching a modified corn seed in India, which has more carbs and more ethanol benefitting both the farmer as well as ethanol manufacturers.