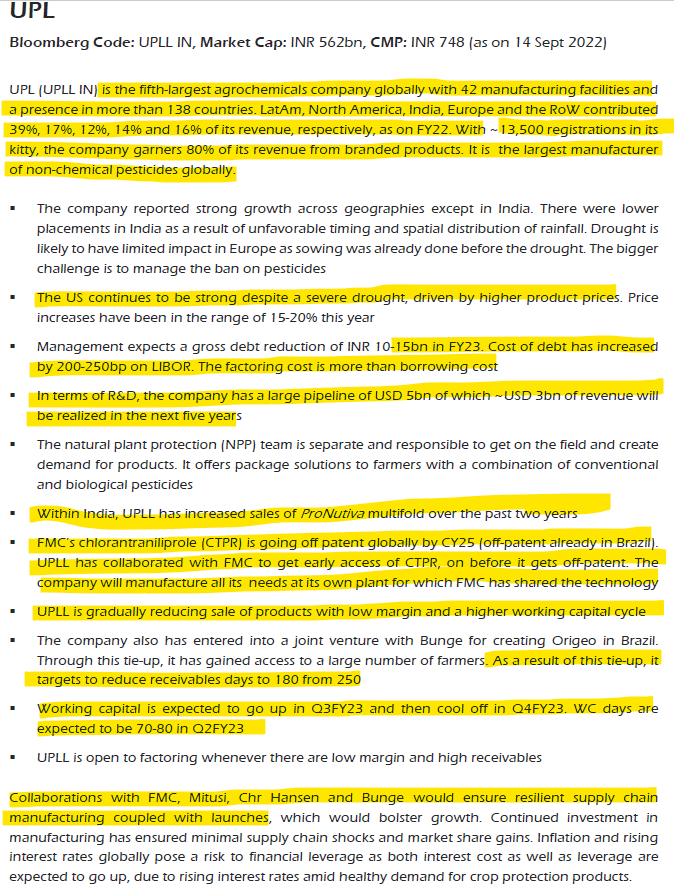

Fy22 vs Fy21: 19% revenue growth( volume +8%, price +10%, 1 % Fx), EBITDA Margin constant at 22%

Raised a Green Bond with 35 bps lower interest rate, which can further reduce by 5 bps on meeting sustainability targets, more Green finance initiatives planned

New product (<5 yr old) revenue : 21 %

Fy23 Guidance 10 % revenue growth, 12-15 % EBITDA growth. Investor PPT

Disc: Invested with a significant allocation

If you don’t mind, I would very much like to hear your investment rationale. For me, UPL seems to have made the leap from a generics player (post patent products) to

an innovator. Some new stuff, they are working on appears very future-proof. On the negative side, the debt overhang and modest growth (10% guidance), muted return ratios in the short term have dow rated it. The cash flows are far and out much better compared to others in the ag Chem space (whose earnings carry 3x to 4x rating).

Disc - invested at around 800 level.

I have been invested for a few years. Key points in favor when the decision was made, and which have continued, prompting me to hold and add whenever valuations have looked reasonable:

UPL has consistently grown faster than market for a long time, and that is a trait I value a lot. It shows ability of management to think differently that peers, this has helped me well in my other investments like Persistent.

Focus on new product development and stated targets on revenue from new products

Reasonable valuations

Agri chem industry is in a sweet spot, years of low growth and investments have created a lot of vendor consolidation, and Agri product prices are rising, increasing farmers propensity and ability to use these products. The price hikes taken by UPL this year are a clear indication of this, and I would not be surprised to see some more hikes in the coming year.

Concerns

Debt (is reducing steadily though), and the poor handling of communications like the Auditor change.

Second major fire in recent times in major plants. Looks like safety standards are not as good as they need to be.

All the positives like worldwide diversification, push into value added products like NPP, synergy with acquired Company etc on the one hand are being weighed against the huge debt, rising interest rate, potential global recession, bloating in work capital and currency weakening against the USD.

Also UPL has guided higher and any negative earnings surprise will weigh this down further along with FII selling of Indian equities.

My personal bet is that UPL will manage it’s debt eventually, may be acquired which will EVENTUALLY lead to rerating. However market has written off UPL until it gets to a comfortable DE ratio.

DISCLOSURE - Invested at 750 avg price, underwater, but aim to hold for long time.

I am a confirmed IDIOT. Words are not recommendations

It is hardly as bad as the market makes it out to be. Trading at P/E lower than its 10yr average is just unseemly. Almost feels like a bear cartel is at works here.

D/E story has been pushed since the Arysta acquisition as if the group would go bankrupt. Nothing bad happened, they have managed their debt well. Then the whistleblower and brouhaha about rent paid on some properties in Bandra that broke in 2020. And now, all the hand wringing on inflation and recession and receivables in Brazil

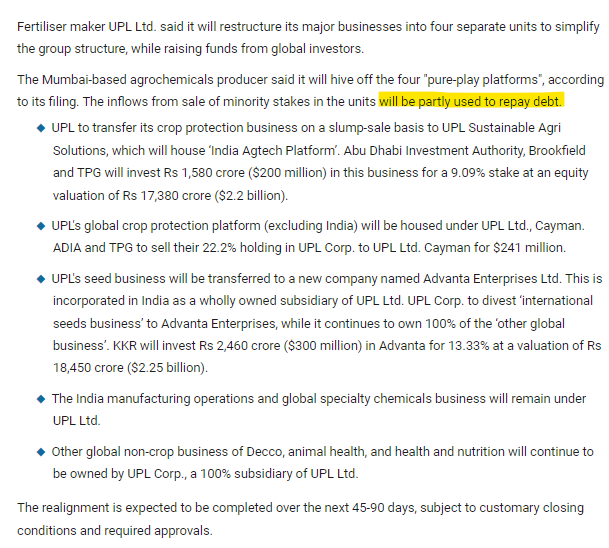

A positive development. UPL seems to be judiciously using debt but markets are not happy about their debt, incl recent surge in WC debt. The restructuring is beautifully done - paving way for demerger of advantage and UPL SAS in due time. UPL can venture beyond Agchem into the broader specialty Chem space where PI industries enjoys such a large PE.

Management doing all right thi gs to create shareholder value, somehow Mr Market still coy…

DISCLOSURE Invested at 750 levels, under water now, Mere words of a lay person, not a recommendation ofanu kind

UPL posted good set of results, might have missed estimates but still results looked good to me… Stock is getting beaten down and is trading at very less PE. Is Europe slowdown such a huge factor?