Exactly, and all the analyst reports also have declared the same in their latest updates.

2 Likes

2 Likes

Seems like UPL is having some sort of corporate governance issues. Gap vs PI Industries is getting wider and wider. I think it is a matter of time PI Industries replaces UPL in nifty50.

Disclosure: Not invested in UPL or PI Industries

2 Likes

I have heard UPL CEO on air on CNBC and amount of stuttering/stumbling (Err…Err Umm) while answering questions like “who owns Sadafuli” etc was a clear indication that something amiss here.I would prefer to stay away from this stock. Just my 2 cents…

I know it would be flagged as folks don’t like counter opinions on many forums…

Disclosure - not interested at any levels

8 Likes

Well here’s the video in case anyone missed it,the complaint was allegedly made by Mr Shroff’s estranged wife in 2016:

3 Likes

Old article:

Given the allegiance, things will be taken care of.

Amounts claimed in today’s alleged fraud don’t seem material.

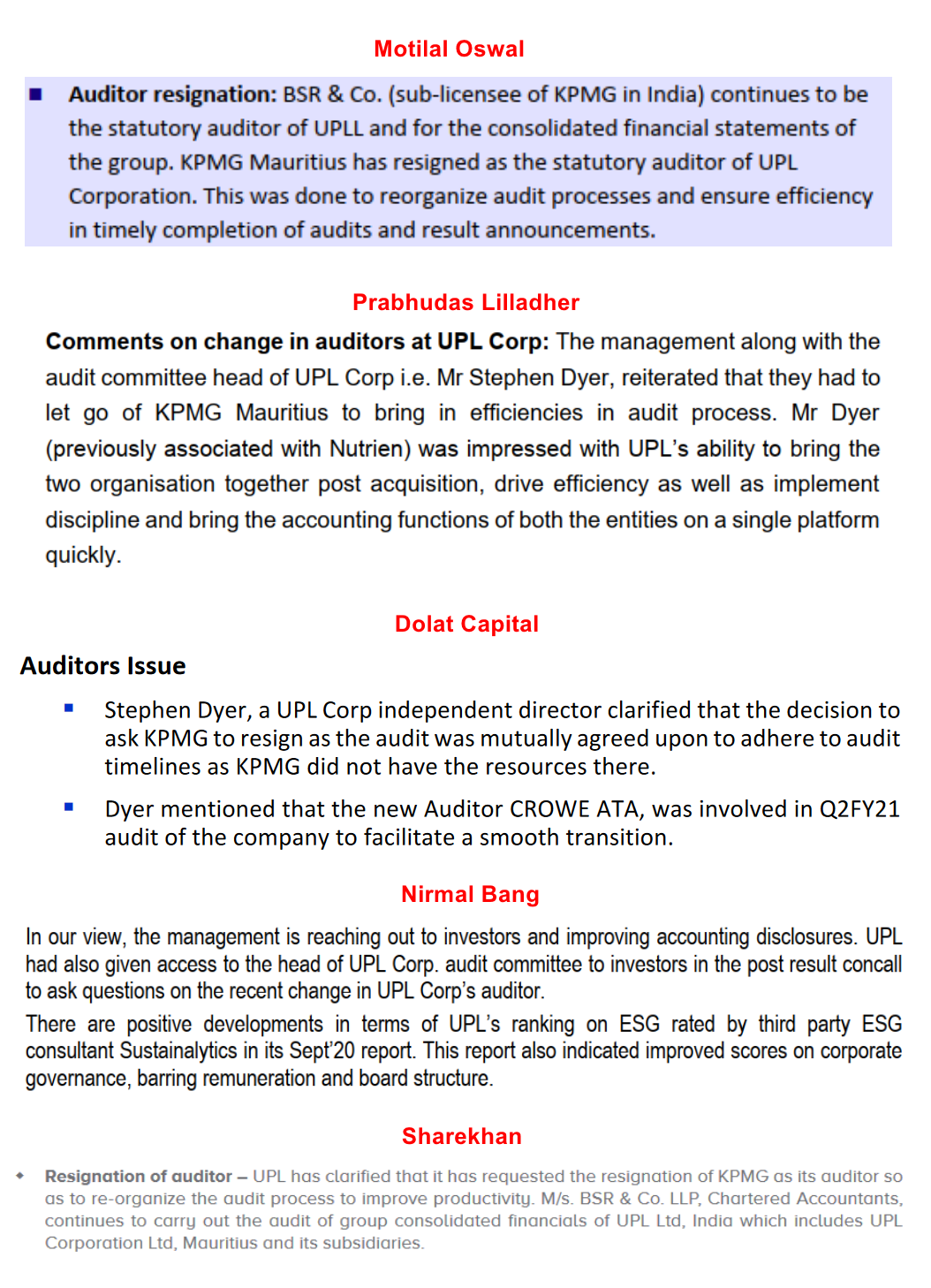

But need to track the auditor resignation issue, if it will raise it’s ugly head again.

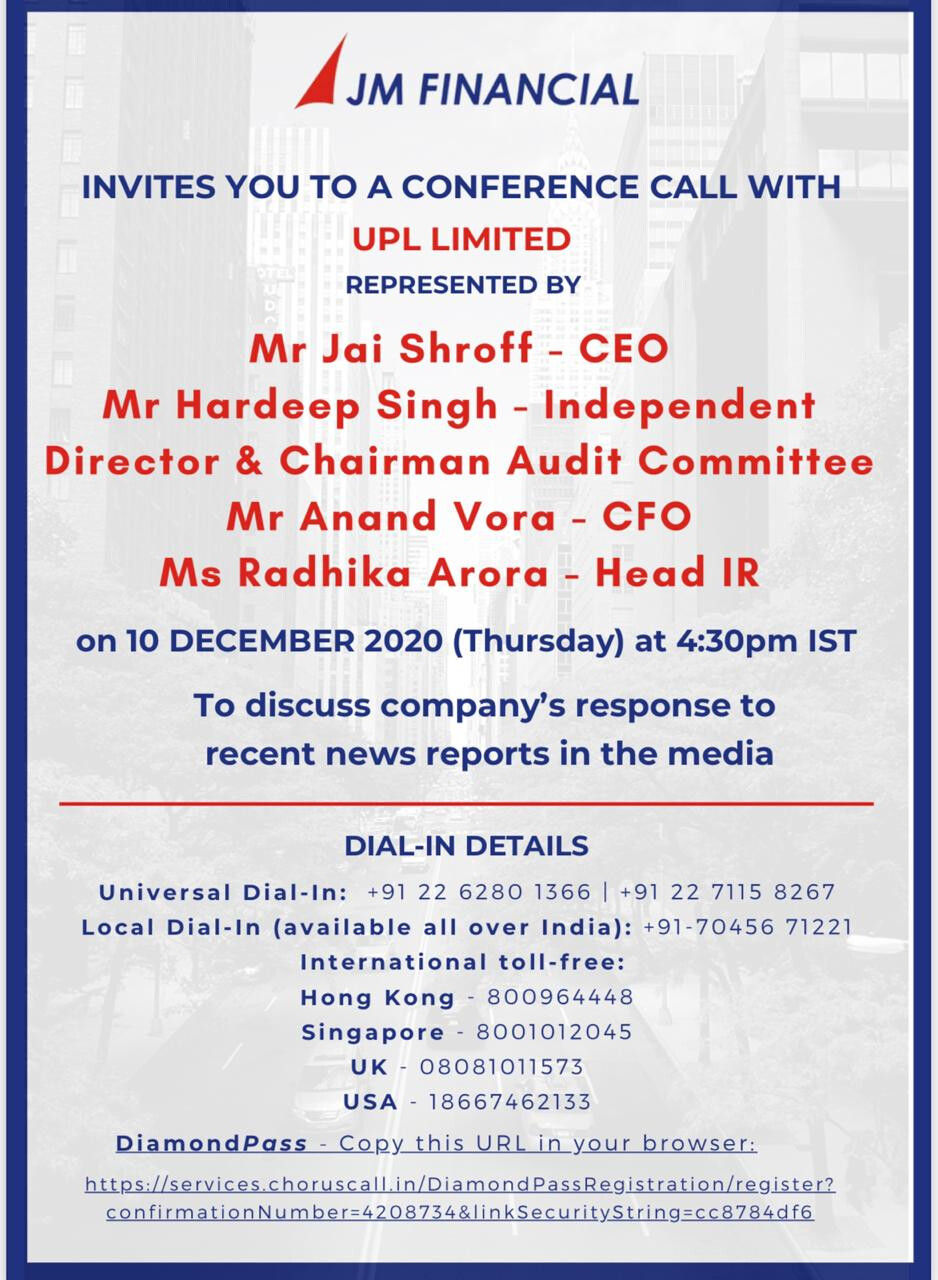

Company conf. call @ 4.30 to clarify today’s news:

Updating the post:

Paraphrasing relevant points from the call below:

Apparently same as old matter from 2016 which was a complaint from estranged wife of CEO.

Overall amount questioned = ~$3 million over 5-7 years majorly with entity (SADAFULI…) towards txns related to rent of property taken for CEO

Sameer Mehta is a consultant known to UPL promoters. He is not a related party or employee. He owns one of the entities in questions, SADAFULI, which had rented the house to UPL for CEOs stay and had some related transactions under different heads such as advance rent by UPL etc. Sameer Mehta is also on the board of entities such as UPL INVESTMENT PRIVATE LIMITED where UPL has stake. All txns at arms length.

Hardeep, the Audit committee chairman, told that he spoke to the reporter of this news a week back and offered him to visit UPL office to review any relevant documents and satisfy himself. But reporter did not avail that offer.

ET article claims that whistle blower complaint is by board member. But Hardeep said that he spoke to all present and past board members from past 7 years and all have refused any hand in this complaint.

Some other points discussed on call include subjective growth projections, debt reduction and reason for so many subsidiaries given their multinational operations and acquisitions over time. Plan to try to simplify structure over time.

Disc: Invested

2 Likes

Another debt prepayment. Still a long way to go to being debt free though.

Management bought 2 % stake in December when it had fallen. Bear operators who prey on high debt and pledge have so obviously planted these fake stories to make a good killing. It will pass when second repayment takes place in march.

Yes debt is huge and will take atleast 5 /8 years to pay off but once it reduces to say 1/1 then they need so slow it down as it’s available to UPL at very low cost vs equity so it best to let it run and give higher dividends to shareholders like Apple does when debt is so cheap and agrichem is going thru a good cash generation cycle with nagri commodity prices so good

3 Likes

How about the sales and margin figure… it seems steady but… Still it is having huge debt even after PE re-rated?

Impressive revenue growth continues with

- YoY 9% Revenue Growth : Driven by 6 %volume, 2 % Price hike and 1 % Currency movement

- EBITDA up 9 %, but PAT up 23 % driven by Lower Tax incidence

- Geos: LATAM(24 %) and India(27 %) were good, North America ok at 11 %, and Europe/ ROW bad with declines

From Notes in Consolidated accounts:

The Warehouse fire in South Africa has an estimated loss of 330 - 370 Cr, but management believes there is enough insurance coverage. The Insurance claim for the Gujarat plant has been approved, and part of the money has been received.

Results presentation is here: https://www.upl-ltd.com/financial_result_and_report_pdfs/ZQUywqSur8yLl9lt9E5ul0Ao4M2jy4xCi5H8pjwj/Q1FY2022_Results-Presentation.pdf

Disc: Invested and holding.

Good results, mainly due to global footprint, unlike many India focused peers like Rallis.

- YoY growth: Revenue + 24 % (Driven by 11 % volume, 13 % price hike), GM Down slightly to 43 %, EBITDA +21%, PAT +40%

- Regions: Latam +22, NA +57, EU +26, ROW 15, India 0 growth (but no decline)

- For 9 Months revenue +17 % , EBITDA 15%, PAT 23 %

- WC Has gone up, but Q3 Days have reduced slightly.

Cons results: https://www.upl-ltd.com/financial_result_and_report_pdfs/9TIaHjg1FNoir7gYFYEx3o6kswzAN6sVcnR0ReCw/Consoldiated_Dec-21.pdf

Inv Ppt: Financial Results | UPL

Disc: Invested and holding

1 Like

1 Like

The company has denied this as a rumor when it was first flashed in news channels. Meanwhile, they announced a buy back through the market route and in a week’s time the promoters have already accumulated 600K shares. The debt levels are still high and merger with a larger company can’t be ruled out.

Disc: Invested and waiting for a good price to exit

2 Likes

“UPL BROADENS BIOCONTROL PORTFOLIO

WITH ACQUISITION OF NEW NATURALLY-DERIVED FUNGICIDE, OPTICHOS”.

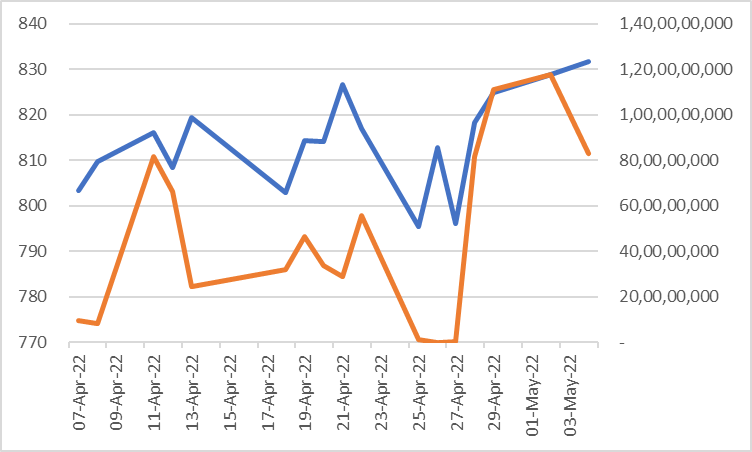

The Company came out with its buy back plan wherein they proposed to buyback equity shares of the company through open market rate for a total amount of Rs 1,100 crores upto a maximum purchase price of Rs 875/share. The Company posts a daily update on the amount of shares it bought back through both exchanges and also the average price of the shares bought that day and then the cumulative figures of the buyback programme. What struck me as odd was that as the share price decreases the company (or the appointed merchant banker or whoever) buys less and vice versa. Whereas as per common sense the money deployed in a day should increase when the price of the stock moves south. Below is a tabular presentation of the summary of all the daily disclosures :

| Total money allocated for buyback | 11,00,00,00,000 | |||||

|---|---|---|---|---|---|---|

| Date | BSE | NSE | Total shares | Avg price | Money spent | Money left |

| 07-Apr-22 | 1,20,000 | - | 1,20,000 | 803 | 9,63,97,439 | 10,90,36,02,561 |

| 08-Apr-22 | 30,000 | 69,900 | 99,900 | 810 | 8,08,99,495 | 10,82,27,03,067 |

| 11-Apr-22 | 4,00,000 | 6,00,000 | 10,00,000 | 816 | 81,60,49,040 | 10,00,66,54,027 |

| 12-Apr-22 | 2,60,000 | 5,60,000 | 8,20,000 | 808 | 66,28,08,485 | 9,34,38,45,542 |

| 13-Apr-22 | 65,000 | 2,35,000 | 3,00,000 | 819 | 24,58,44,039 | 9,09,80,01,503 |

| 18-Apr-22 | 1,40,000 | 2,60,000 | 4,00,000 | 803 | 32,11,90,988 | 8,77,68,10,515 |

| 19-Apr-22 | 2,03,897 | 3,67,502 | 5,71,399 | 814 | 46,52,80,298 | 8,31,15,30,217 |

| 20-Apr-22 | 1,34,000 | 2,82,000 | 4,16,000 | 814 | 33,86,73,475 | 7,97,28,56,743 |

| 21-Apr-22 | 1,10,000 | 2,40,000 | 3,50,000 | 827 | 28,93,36,327 | 7,68,35,20,416 |

| 22-Apr-22 | 2,82,811 | 4,00,000 | 6,82,811 | 817 | 55,78,66,768 | 7,12,56,53,648 |

| 25-Apr-22 | 860 | 13,154 | 14,014 | 795 | 1,11,45,929 | 7,11,45,07,719 |

| 26-Apr-22 | - | - | - | 813 | - | 7,11,45,07,719 |

| 27-Apr-22 | 2,623 | - | 2,623 | 796 | 20,87,908 | 7,11,24,19,811 |

| 28-Apr-22 | 4,40,000 | 5,60,000 | 10,00,000 | 818 | 81,83,74,080 | 6,29,40,45,731 |

| 29-Apr-22 | 3,00,000 | 10,46,534 | 13,46,534 | 825 | 1,11,05,91,000 | 5,18,34,54,731 |

| 02-May-22 | 4,63,289 | 9,55,396 | 14,18,685 | 829 | 1,17,57,33,151 | 4,00,77,21,580 |

| 04-May-22 | 2,50,000 | 7,50,000 | 10,00,000 | 832 | 83,17,77,280 | 3,17,59,44,300 |

| 7,82,40,55,700 |

Here we can clearly see that when the stock was at its lowest i.e. on 25th and 27th respectively then only an amount of Rs 1.32 crores approx was spent on buying back shares whereas apart from these two days the Company regularly buys shares north of Rs 55 crores. What sense does it make? Has this got something to do with the commission of the merchant banker? Would appreciate if some finance industry person can so throw some light on this.

Below is another chart to show this data graphically

Hoping for a response. Thanks!

Disclosure : Invested

6 Likes