As an established player UPL manufactures and markets agrochemicals, industrial chemicals, chemical intermediates, and specialty chemicals, and also offers crop protection solutions. When we build an investment case, we need to look at the stock with a holistic approach. With that perspective in mind with a long term track record, UPLseemed like a financially-sound company with an impressive track record of annual revenue growth, dividend payments and an excellent growth outlook

However, of late things were not quite the same in the last year. Coinciding with the Arysta acquisition, revenues were more or less flat and net profits declined steadily for the most part of the last few quarters :

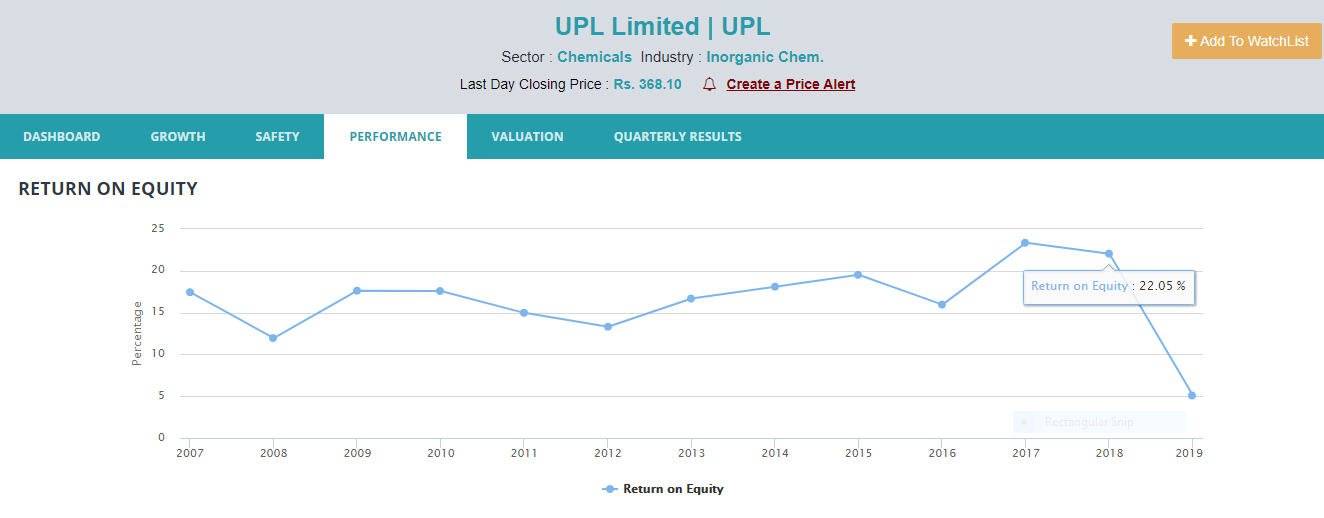

This steady fall in earnings has thus also reflected in the performance with UPL’s annual return on equity encountering precipitous fall to 5.04 in that year, which otherwise was hovering around a much higher level of 15-20 % for almost all part of the last ten years. Following chart thus depicts the relevant picture for the same :

The debt burden accumulated due to Arysta acquisition leading to the rise in interest costs, therefore, seems to have weighed down on the earnigs for these last few quarters. The silver lining though came from the pleasant 77% jump in net profit YoY for the third quarter of the last fiscal(Q3 FY20) as visible in the first chart above. This probably has come out due to the expected seasonal upside in revenue and the absence of non-recurring adjustments witnessed in the first half of FY20.

Meanwhile, to add to that, Company has said that it expects its net debt to be at approximately $2.9 billion as of 31 March 2020, lower than $3.8 billion as of 31 March 2019. This represents a significant reduction of debt which would come on the back of healthy realizations of receivables and inventory taking place in the fourth quarter. The company plans to reduce debt further in the coming years by way of improvement in performance, better cost synergies, and judicious working capital management. There is no denying that there are uncertainties looming in the short term owing to prolonged lockdown all over the globe. However, UPL sees the demand in line with the expectations as the farming season continues to be normal across the world, being supported by governments across the world for the purpose of strengthening their security of food supply.

Shares of UPL were among the big losers on Tuesday after the Centre issued a draft order to prohibit use of certain insecticides, citing risk to humans and animals. The development is negative for UPL as some of its major products like acephate, monocroptophus fall in the list. The list also includes insecticides like chloropyrifos, mancozeb, which are part of UPL’s portfolio.

If Draft order is implemented , it will impact UPL (Acephate, Mancozeb,Pendimethalin & others),Bhagirdha Chem (Chlorpyriphos), Aimco Pesticides Ltd(Chloropyriphos), Excel Industries Ltd((Raw Material for Chloropyriphos), Atul Ltd (2,4D), Meghmani Organics Ltd(2,4 D,Deltamethrin etc), Coromandel International Ltd (Mancozeb). This order may not ban export of these molecules. Therefore impact will be less

Above list is of Technical products. More than 100 formulations or combination products(ready to use) will be banned. It will impact Rallis india Ltd, Insecticides India, Crystal Crop etc.

Major overhang on UPL is taking up of additional Debt of 3 Billion Dollars due to Arysta acqusition. Another point is recent Draft proposal of Central Government to ban 27 Pesticides.

If UPL reduces Debt in next 2-3 quartesr and Draft Ban proposal is not implemented, UPL may be rerated.

UPL has entered into global agrochemical arena with Arysta acquisition.

Due to unique model of Arysta, whereby, the manufacturing of the products is undertaken by third parties under its brand, it has traits of FMCG.

The lower valuation is on account of higher sales accounted by Latin America (38% in 2020), that experience wide currency fluctuations due to multiple factors.

Have patience, it will reward you in the near future, as the stability returns.

Latin America, a key market for UPL, reported robust 12% yoy growth (a beat of 4%) on back

of strong demand for its key products despite currency devaluation. Growth momentum will

continue in H2 as higher acreage led by better weather conditions and high spending by

farmers on back of improved crop pricing (corn/soybean).

North America also witnessed robust revenue growth of 9% yoy (a beat of 17%) led by

better weather conditions and ease of trade tension between the US/China. Growth is

expected to remain higher in H2 on back of better crop prices and demand.

Europe had some covid led challenges but despite that UPL delivered a strong growth of 9%

yoy (a beat 7%) primarily led as differentiated and higher value products sales (benefits of

integration). RoW had the highest growth of 27% yoy (a beat of 5%) with contribution from

SE Asia (new product launches), China (better B2C business) and South Africa/Australia/New

Zeand (better weather conditions). India continues to see better growth due to strong

kharif demand. Revenue growth was at 18% yoy (a beat of 7%).

#Synergy: UPL is continuously outperforming its guidance for cost/revenue synergy by achieving

revenue synergy of US$299 mn in just 5 quarter of integration (vs target of US$350mn in 3

years) and cost synergy of US$153 mn by now (vs target of US$ 200mn in 2 years).

#Balance Sheet improvement: 1) Despite of qoq rise in working capital by ~US$300mn, the

gross debt reduced by US$ 103mn in Q2 and the management is confident to cut debt worth

US$ 750mn in FY21. 2) In Q2, WC cycle also improved by 14 days with

receivables/inventories/payables days improving to 124/105/123 from 124/108/113 last

year…

Guidance: Despite of strong beat in its growth guidance during H1, management maintained

FY21 revenue/EBITDA growth guidance at 6‐8%/10‐12%. Debt reduction by US$750mn in FY21.

Was there any comment on the AUDIT issues that seem to be plaguing the stock? We have seen it fall from 51 to 415 now and management is not giving clarity with a strong voice leading to suspicions of some mismanagement

Could anyone clarify the implications of this or is this routine procedures? What could be some of the reasons to decline sharing of details around their exit?

Still waiting for clarity. On the charts, there has been a clear breakdown.

Jai Shroff appeared once on CNBC, but has been missing since. Very little communication from the management.

Even after a good result, stock continues to decline.

The stock is 5% of my portfolio and I have been holding it for a very long time now. I would like to give benefit of doubt to the management at this point, but waiting for more clarity.

Honestly this auditor resignation issue is unusual with respect to the auditor refusing to fill the SEBI template of resignation. This is either a bear cartel spreading rumours or it could be that KPMG Mauritius is trying to hide something. (related to their own performane / capabilities or even UPL)

The new Mauritius Auditor is Crowe ATA, which i dont know whether is credible…they used to be UPL corp’s old auditor as can be seen in the 2019 UPL corp annual report.