this is a great write up! i was trying to figure the following -

who would be Ultramarine’s closest competitors in the surfactants division? on comparing rough realizations of UPL in surfactants on a per kg basis with Galaxy Surfactants, it works out to following - UPL - INR 59 per kg (160 crores / 28000 MT) vs Galsurf’s 114 per kg. have you looked at this?

Do you know how much would the 1,500 MT new pigment capacity contribute to sales?

what % of RM costs would be Alpha Olefin?

if you are ok sharing, what is the source for 13% market share?

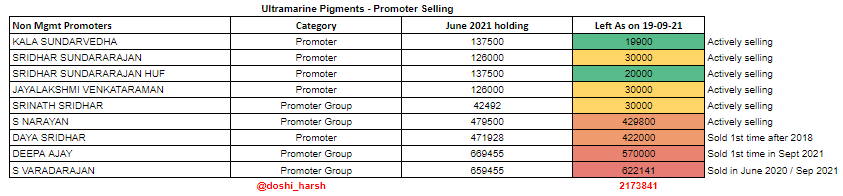

Can someone please explain what was the rational behind promotors selling shares everyday rather than just selling it at once or maybe in a few transactions?

Promoter shareholding reduction is mainly due to exit of a set of promoters who were NOT running the business. The promoters who are running the business have increased their shareholding.

I think the company is good, but if you see its sale has a CAGR of 20% for the last 12-13 years but the problem is the bottom line which hasn’t moved more than 5-6%.

Also, the company doesn’t seem to have the advantage of passing the price hike, which can be seen in its stock price.

Pls answer this question, If we see the difference between FY22 and FY23, there has been a difference of around 127Crs in reserves, did they do any huge CAPEX?

The company has made Mr. V Bharathram as MD, how well he will make the company go big and how he will contribute is the question