This is the first time I am attempting to start a thread. Please pardon me if there are some mistakes. Basically I was screening for ideas: cheap stocks, with decent return ratios and dividend yield, zero debt and yes no pledged shares because I find the Indian stock market extremely expensive. I found the following:

Company : Ultramarine & Pigments

Market Cap: 232crs

Listed on: BSE

Website: http://www.ultramarinepigments.net/

Stock P/E 13x trailing,

Promoter group: Related to Thirumalai Chemicals.

Manufacturing plants in Chennai, Ranipet and GIDC in Gujarat.

No institutional holdings in the stock currently

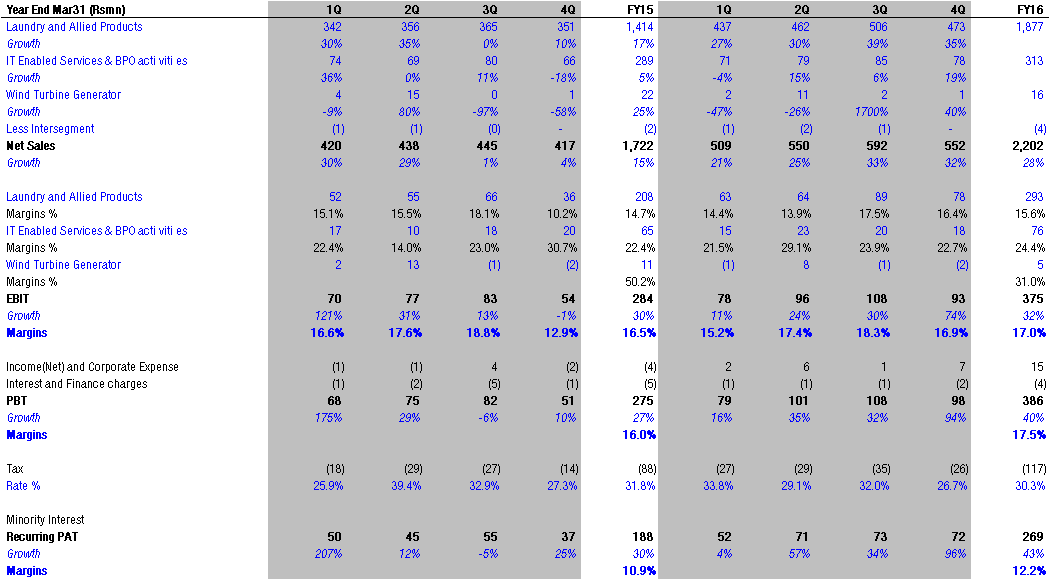

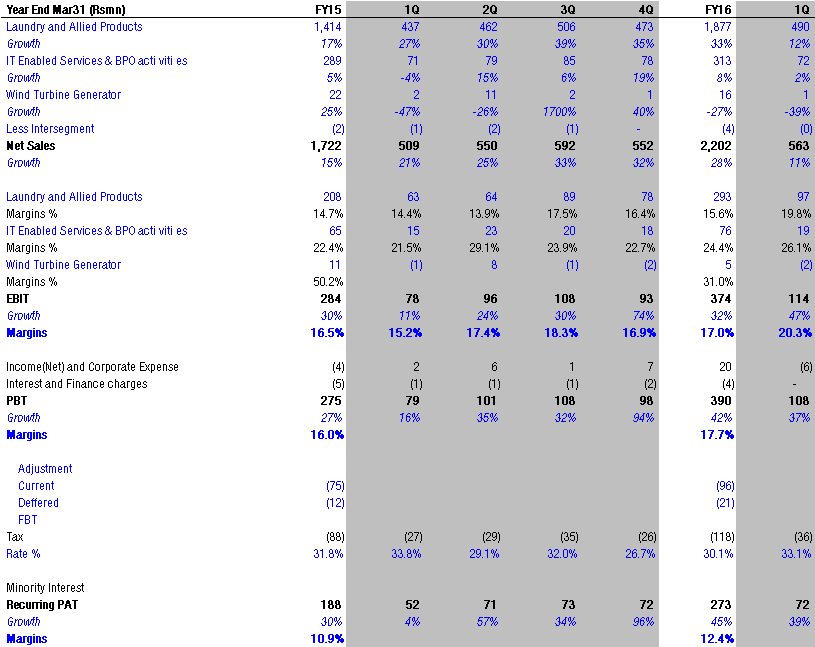

Company makes pigments and surfactants. The pigments are supplied to paints, plastics, rubber and building materials companies. Surfactants are supplied to FMCG companies for making detergents, dish washing liquids etc. It also has industrial and agri applications.

The company has also launched its own brand of detergents and dishwashing liquid in South India in FY15 and got a positive response.

Last but not the least the company has an IT/ITES division called Lapiz Digital services which is involved in digital publishing (similar to MPS) and medical billing

Promoter stake is 51%+ and is increasing every quarter

http://www.bseindia.com/stock-share-price/stockreach_shp.aspx?scripcode=506685

Company has PAT margins of 8.3 - 13%, average RoEs in the 14-23% range, average RoCEs (pre tax) 20-28% levels. Positive cash flows from operations and positive FCF. Over last 6 six dividend payout is in the 47%-81% levels. Zero Debt, Dividend Yield 3.7%,

The stock reminded me of how Anuh Pharma financials and valuations looked like when I first saw it at Rs300 levels. Of course Anuh has better return ratios

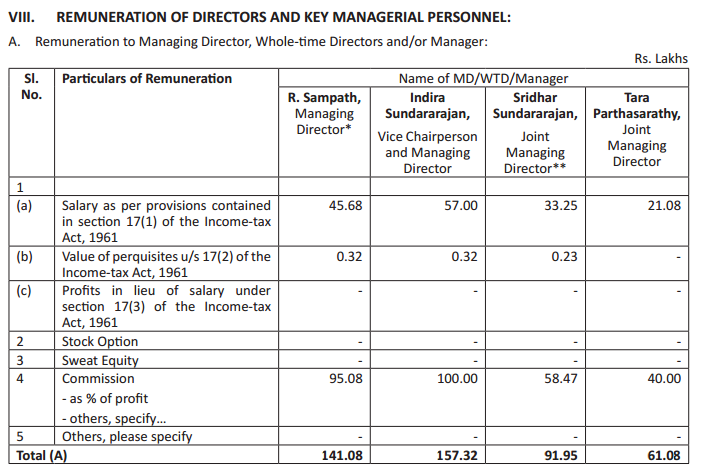

Chairman details

Mr. R.Sampath graduated in Chemistry from the University of Bombay, and obtained his Chemical Engineering degree from Washington State University, USA. He started his career as a Process Development Engineer in M/s. Hercules Inc, Missouri (USA) . Subsequently he returned to India and joined Unilever’s Indian subsidiary. He joined Ultramarine and Pigments Ltd in 1970 as Project Engineer. Since then, he has worked in various capacities as Project Manager, Development Manager & General Manager before being appointed as the Managing Director in 1990 and Chairman & Managing Director in 1997. Apart from introducing new varieties of pigments (new grades), he was responsible for starting the surfactant division in 1973. Subsequently, the surfactant division has expanded considerably, and now forms about 50% of the revenue of Ultramarine. Since the start of his tenure as MD, the turnover of the company has shown a ten-fold growth in 20 years. The company’s sales footprint has expanded from 2 countries to 50 countries and is still growing widely in emerging markets in Latin America and Africa.

Disclosure: Have a small tracking position in the stock