This may be useful :

Pigments division - 32% of revenue

Surfactants division - 53% of revenue

IT Division - 14% of revenue

The company also manufactures detergent under the brand name OOB.

Why will an accomplished professional want to be an independent director unless he is remunerated well

Hey thanks for this! Where can i get such TIA notes of each year?

An Independant Director, in an ideal world, is a watchdog for retail investors, against any excesses of the management, which gives it undue advantage. For this his commission, regardless how small or big (within regulatory limits), should be independant of company’s net profit. This is what I have tried to highlight.

2 Likes

Qtr 4 result will include contribution from newly Added capacity also.

I think That is why stock is moving higher near results

Big Investors (like Marcellus) piling in for a structural long term play due to consistently compounding earnings and extremely high ROCE and cash generation. Price target of 800 (20 x Normalised PAT). See below links

Hi All,

Please advise on below point.

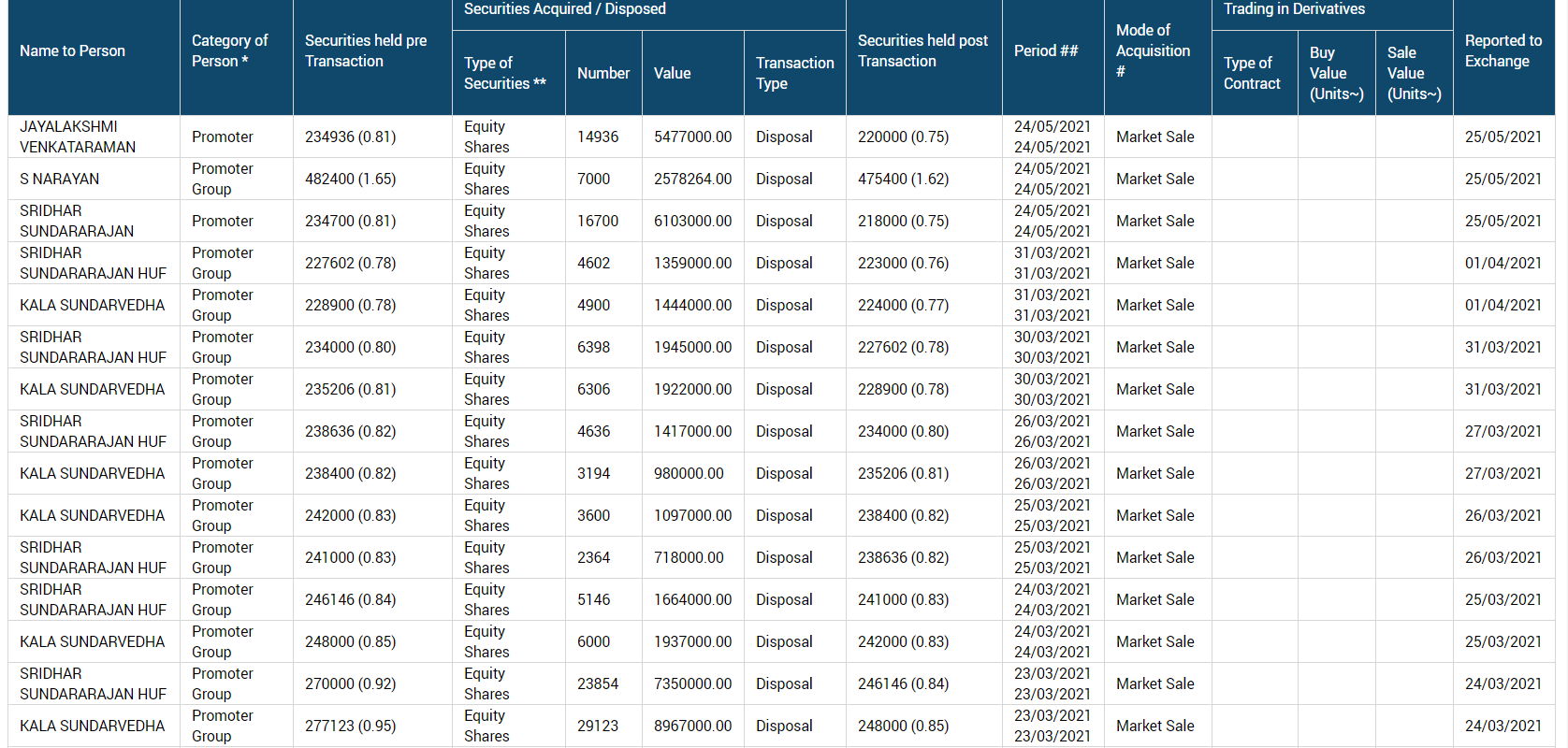

- Any info why Promoter continuously selling shares from past three months…

The person who is selling isn’t associated with the day to day operations of company. There is some dispute as per unconfirmed sources so he is selling and wants to get out of the company. Fundamental wise this isn’t an issue as per me.

I have tracked this company for a long time and have also held the stock for long periods of time. Company is very opaque and does not meet investors or host conference calls. Only platform to meet management is the AGM

Now the company is a contract manufacturer of detergents and surfactants (which is not speciality chemicals as some of the PMS gurus would like you to believe)

The margins get impacted when crude oil and LAB (Linear Alkyl Benzene) prices go up. So that could be the reason why a lot of insiders are selling. See the sharp YoY correction in 4QFY21 margins

Businesses do not change just because some PMS Guru buys the stock in his Little Champ portfolio.

4 Likes

Even if there is a dispute between factions in the company, if one believes prospects are good would one sell their shares?

BTW if there is a dispute, dont you find it even more worrying

3 Likes

Interesting to see if the selling will continue because the sellers still hold huge quantities of stock. If they plan to exit, like subsequent posts call out, there could be more selling in the months to come. The reason they don’t sell in one go is to avoid crashing the stock. Like in case of Astec, there could be attractive buying opportunity if selling continues

Company is doing capex to move into specialty chemicals where margins are higher. This was the trigger for the stock. In this market, even a capex plan that delivers results 2 years down is priced into the stock today itself.

The family Sridhar, Jeyalakshmi ,Kala,and Narayan who are continous sellers hold still about 14 lac shares in the promoters category and hopefully their friends/relatives must be holding another 5-6 lacs. So approx 20 lac shares will keep hitting the mkt.They havent bought into Thirumalai though the other family(Parthasarathy) has bought substantially between Jan21-May21.

The sellers have not sold any shares above Rs375 (30 apr and 19 May).Strange.

Such promoter selling doesn’t augur well for the co and any investor will desist from investing when a sword like this hangs above your head and god knows what damaging disclosures will come if the fight gets ugly.

Forwarding my write-up on the company:

Ultramarine & Pigments Ltd

(Price:330 ; Mcap: 980 Cr ; EV/EBITDA: 12x)

Company Profile

- Co. was formed over 6 decades back in 1960 by Mr. Rangaswamy Sampath, Thirumalai group promoters with manufacturing units located in Chennai & Tamil Nadu

- Product Profile: Inorganic pigments & Surfactants with core products- inorganic pigments(32% of topline) & Surfactants(54% of topline). Company does contract manufacturing for leading FMCG clients and has its own retail brand- “OBB” which is dominant in southern India. They also have an IT division(15% of topline).

- Pigments product basket includes ultramarine blue, ultramarine violet & Bismuth Vanadate which are used as colorant in industries including plastic, fabric, printing ink, cosmetic etc.

- Surfactants product line comprises of Linear Alkyl Benzene Sulphonic Acid (LABSA) & Alpha Olefin Sulphonate (AOS), which are used in detergent, dish washer, cosmetics

Industry:

-

Bifurcation between organic & inorganic pigments:

-

Global market for ultramarine pigments is estimated to grow at 4% CAGR from $190 Million in 2020 to $249 Million in 2027. So, ultramarine has roughly 13% market share globally in ultramarine pigments division

-

Ultramarine blue- an inorganic pigment, is made using China clay. It is a difficult manufacturing process because it takes lots of trials and errors to master the quality of the pigments. It is used while making plastic compounds so that the plastic retains it color for longer time. High grade pigment is used in plastic, paints, coating etc. whereas lower grade pigments are used in whitewashing & laundry application

-

Surfactants are compounds that lower the surface tension (or interfacial tension) between two liquids, between a gas and a liquid, or between a liquid and a solid. Surfactants may act as detergents, wetting agents, emulsifiers, foaming agents

-

Key RM for surfactants is Alpha Olefin which is 100% imported and very volatile in nature.

Key Rational:

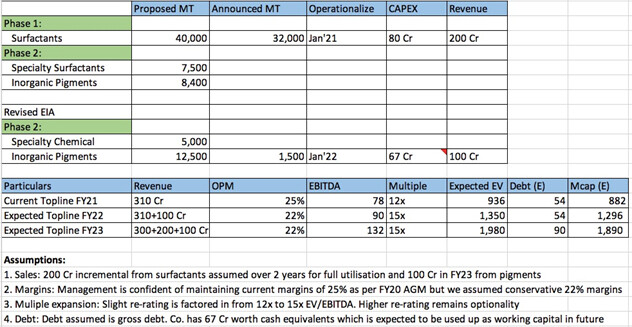

Greenfield CAPEX:

The Company has seen tepid growth over the last decade in pigments wherein topline has increased from Rs.45 Cr to Rs.100 Cr whereas surfactants have increased in topline from Rs.55 Cr to Rs.165 Cr. This growth was achieved with mere debottlenecking in pigments and slight capacity addition in Surfactants.

- However, in Jan’21 co. has commercialized its greenfield project at Naidupet, Andhra Pradesh with capital outlay of Rs.80 Crores, majorly funded by internal accruals. Stabilization of all processes was achieved by 31st March’2021.

This capex is in surfactants division (32,000 MT) and can generate around Rs.200 Cr of incremental topline as per management guidance given in FY20 AGM. - Co. has also formed a subsidiary- “Ultramarine Specialty Chemicals Ltd” on 09/12/19 to implement a greenfield capex in Naidupet, Andhra Pradesh with capital outlay of Rs.67 Crores, revised upwards CroreRs.36 Crores. Ultramarine blue and other pigments are to be manufactured from this expansion (1,500 MT) and it is expected to commercialize by FY23. Incremental revenue generation of Rs.100 Crores at optimum utilization

Strong Financials:

- Company was debt free until now and has grown over decades primarily with internal accruals. Management is extremely risk averse

- Company has never diluted its equity capital

- It generates cashflows of around Rs.50 Cr annually and these cashflows have funded debottlenecking and innovation in product mix in the past

- As on H1FY21, co. has cash & cash equivalents of over Rs.67 Crores and debt of Rs.36 Crores. Debt is expected to rise as funding for pigment capex would also be needed once Environmental Clearances are in place. Also, working capital requirement for the new capacities could put slight strain on Balance sheet. However, strong cash position and cash flow generation provides comfort

- Margin profile is very sticky and have structurally grew from 17% to 25% over last 5 years. These margins are expected to sustain as they are due to higher contribution from value added products

- It also has 20% holding of Thirumalai Chemical Ltd which is valued at over Rs.200 Crores. However, we are not assigning any value to it as its part of cross holding and there are no plans to liquidate the stake in near future

Prudent Capital Allocation:

Over last decade, company generated cumulative CFO almost equal to the cumulative PAT. Almost 50% of Cumulative CFO was distributed as dividends

Changing Product Mix:

- With a focus on improving yield of high value grades of pigments, the company invested in R&D in all stages of the production process, from Raw Material procurement and processing to the final stages of value addition. Co. is currently processing 30% more of the high value grades than they did last year by volume, and 150% more than they did in 2016-17, entirely due to internal innovation.

- This change in product mix, towards value added products have led to margin expansion over last couple of years with operating margins increasing from 20% to 25%. Management is focused to increase the specialty products in both surfactants and pigments going forward

Key Weaknesses:

Volatile Raw Material: Surfactants are relatively low value-adding business. The key RM used for surfactants is Alpha Olefin which is crude derive which is 100% imported and is highly volatile with erratic availability. Hence, co. may not be able to instantly pass on the RM rise in finished products and margins may be hampered in short term. Such margin squeeze was observed in Q4FY21 wherein operating margins fell to 19% compared to 24% YoY and 28% QoQ

Product Concentration: Almost 1/3rd of topline comes majorly from Ultramarine Blue pigment which has very niche market globally and co. is already a market leader in ultramarine pigments with market share of 13%. Hence, scalability in this segment might be difficult in future

Delay in ramp up: Any delay in ramping up surfactants plant to optimal utilization or delay in attaining EC for pigments can delay the growth expectations in the co. and put minor strain on the balance sheet.

Management selling: Company was promoted by few different families but from recent shareholding changes, it looks like consolidation of shareholding is happening wherein few promoters are constantly selling the shares in open market. The promoter selling creates pressure in short term on the stock and such promoters still have 13L shares which is 4.5% of total equity and may create pressure on the stock as it is highly illiquid counter.

34 Likes

Excellent writeup. Any website where we can track Alpha Olefin prices?

FY21 Annual Report came out recently. Sharing key highlights-

-

Dividend of Rs. 5/-

-

Company was able to maintain the manufacturing division’s exports (52cr (PY 55cr)) at the same level but ITES division’s revenue declined.

-

Company has successfully commissioned the Sulphonation plant at Naidupeta

-

Revenue from Pigments division dropped by 7% as compared to previous year.

- Revenue- 92cr (PY 98cr)

- Reason for fall- Company faced supply chain bottlenecks and logistical challenges, which slowed our export shipments.

-

Surfactant- division continues to achieve 100% capacity utilisation

- Sales grew by 14% in volume and by 12% in value

- Reason- flexible product mix & the efficient operation of the plant

- Revenue- 184cr (PY 164cr)

-

Greenfield Capex in Pigment division through WOS-

- Outlay- 67cr

- Timeline- Hope to commence operations by Q3FY22

- Key Benefits- Company expects to have a shorter operations cycle, and higher proportion of value-added products.

-

An interesting extract from the MD&A-

Misc points-

-

Average percentage increase in the salaries of employees other than the managerial personnel in the financial year is 16%

-

All CSR amount spent

-

Loans given (details not given)- 31cr (PY 34cr)

-

Contribution of Customers in owing more than 10% of Total receivables- 53% (PY 45%) (Need to understand what this exactly means, does it mean two customers form 53% of the trade receivables? If it is so high then when don’t have number of customers from who they get revenues more than 10%)

- There are 2 such customers that form more than 10% of receivables

-

Nothing much in RPT apart from salary, minor rent to Thirumalai, and minor reimbursement of expenses to Thirumalai

-

R&D expense- 1.62cr (PY 1.47cr)

Disc: Tracking

9 Likes

Any Idea why promoters relentlessly selling the shares. Its not one/two days. They started selling from May. Any insight will be helpful

I believe, The operating promoters are not selling. Its a large family…sort of separation is going on. company should give a reasoning for the same.

Isn’t the opportunity size very small in ‘Ultramarine’ category & surfactants is a commodity business ? How would you value this co. ? We should evaluate sudarshan chemical as well. bigger/aggressive co. with wide market presence.

Galaxy Surfactants is a 10K market cap company. The surfactants manufactured by Ultramarine and Pigments compete in the same market?

Current Valuations look like this :

Galaxy - EV 10000 Cr , Sales 1830 Cr ( Mainly Surfactants)

Ultramarine - EV 900 Cr , Sales 300 Cr ( Surfactants + Pigments)

Aarti Surfactants - EV 1200 Cr, Sales 500 Cr+ ( Surfactants)

Disc : Invested in Aarti Surfactants

3 Likes