Alpha Olefin (AO) price is linked to crude price any sharp rise in crude price, as happened in 2008 will adversely affect the profitability.

That is true. Sharp rise in crude prices can impact margins negatively for all chemical companies in india barring say a vinati organics and a few more. On the flip side the stupendous increase in margins over last 2 to 3 years is because of fall in crude prices and rupee depreciation.

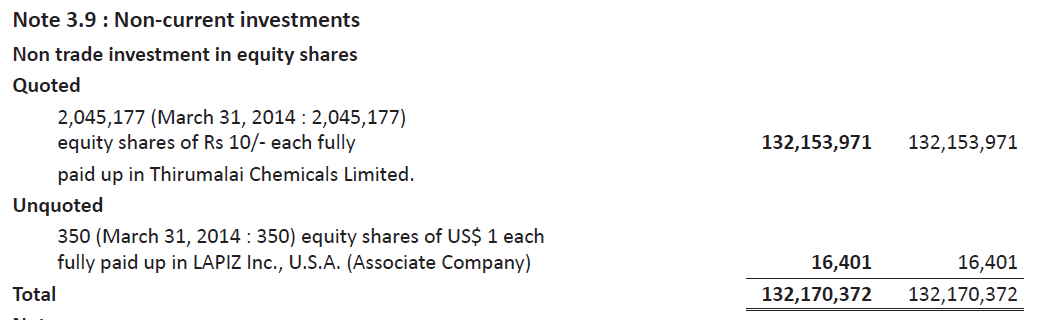

This company has 20% stake in listed company Thirumalai Chemicals whose stock has grown over 5 times in last 1 year. How/where does this show up/reflect in stake holding company’s financial results ?

You can see this in the annual report of U&P. See below. These are are cross holdings which might never get unwound. Ideally one should not attribute any value to the same. BTW this print screen is from FY15 annual report. I assume there has been no changes in FY16 annual report

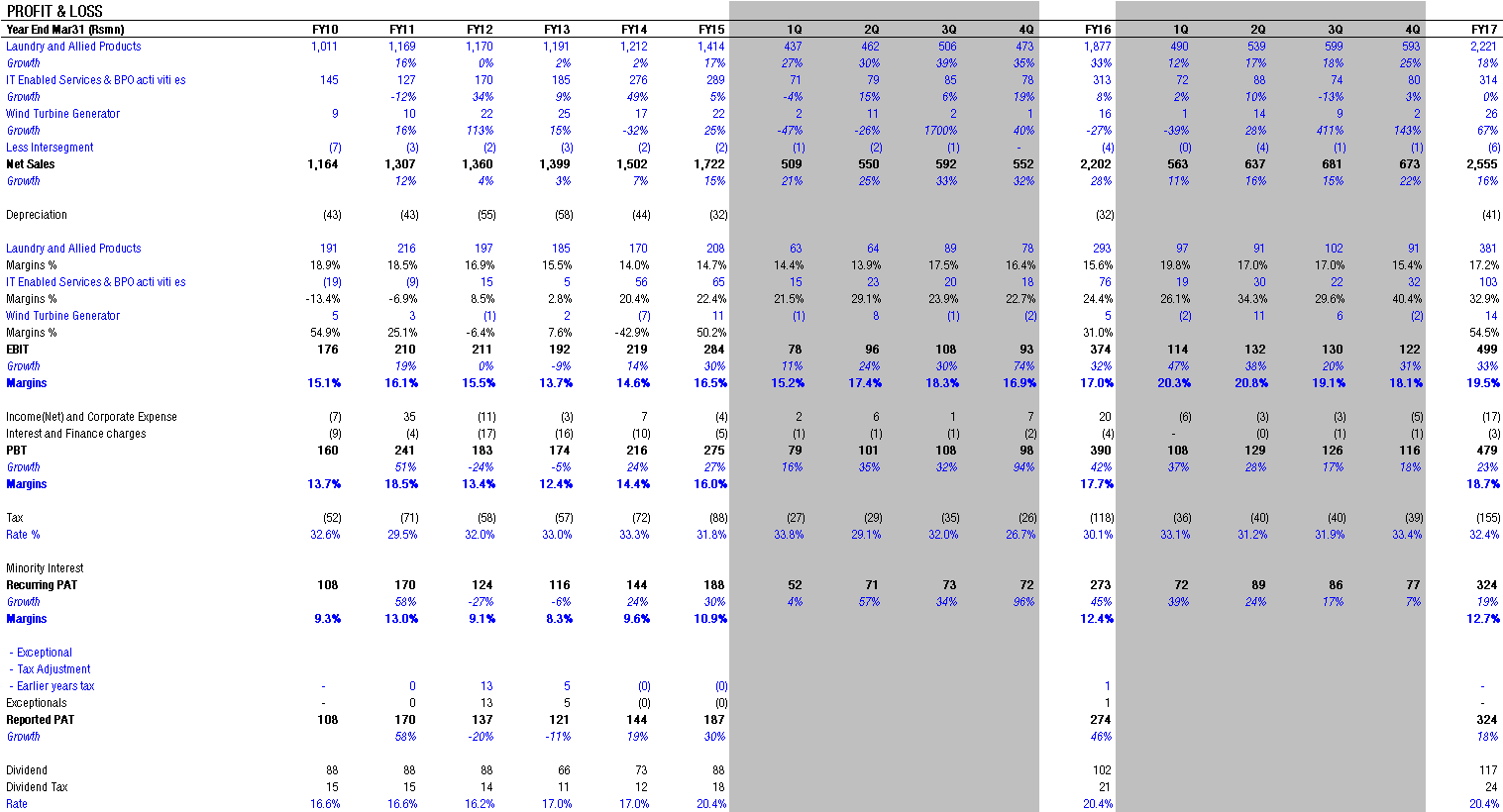

At current market price of Rs200 stock trades at 21x FY16 and 16.5x FY17E if I assume 30% PAT growth in FY17E (1Q PAT growth was 39% YoY). BTW 2QFY17 results are on November 12, 2016

Disclosure: Invested from lower levels

2 Likes

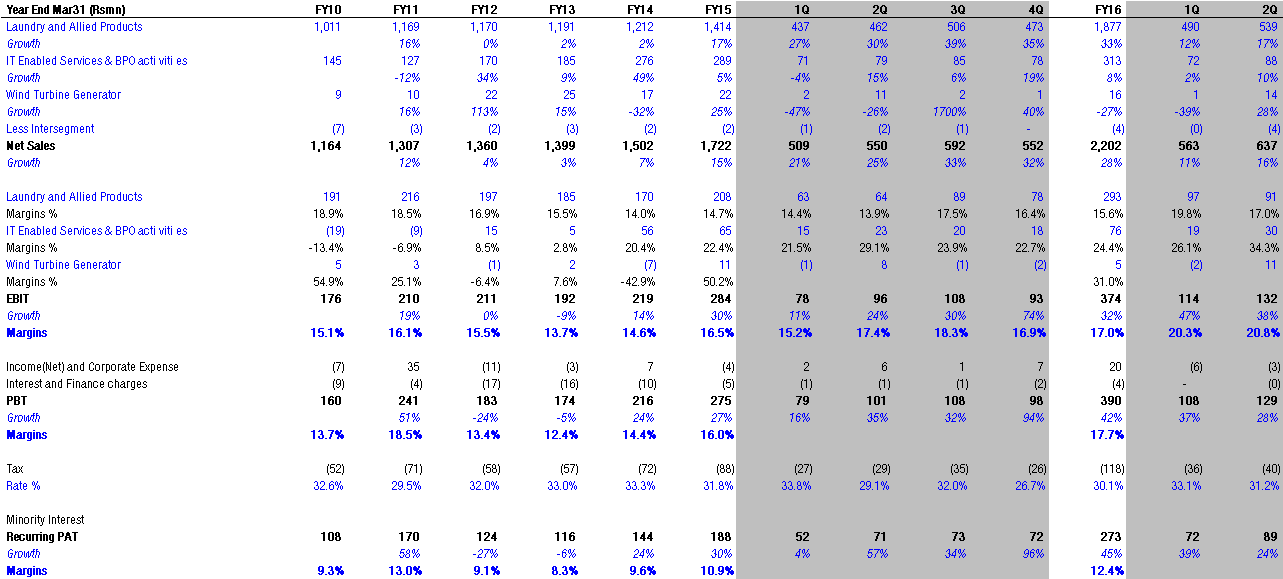

Another solid quarter by the company. PAT up 24% YoY. If company delivers same PAT as 2Q in 3Q and 4Q one can expect EPS of Rs11.6. Stock at current market price of Rs156 trades at 13.6x FY17E.

1 Like

Definitely good results !!

I would like to understand more about their Gujarat plant. It has been in pipeline for sometime now but they haven’t really decided on what to manufacture there. Also it is not clear what is the exact status of this plant?

Could someone help me with this? Thanks in advance

Disc: Invested recently around 160 levels

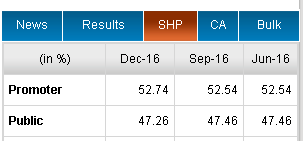

There is no information about Gujarat Plant but promoters have increased their stake in last qtr which is a good sign.

Disc:Invested around 175

Yes promoter stake has gone up again in December quarter

1 Like

From Dec 2016 till now, they have bought 39,020 shares while have sold 61509 shares through market transactions

Can you please share the source of this information

Quarterly results are decent.

However they seem to have restated last year’s PAT in 3Q to 77.9mn was 73.4mn reported last year. Because of that headline growth looks muted at 10% v/s actual 17%.

If 4Q PAT is same as 3Q then FY17E EPS will be 11.6 which trading at 14.5x FY17E

1 Like

Ultramarine also has a significant stake in Thirumalai Chemicals worth 180crs.

2 Likes

yeah - so its actual worth has gone atleast 5 times on that investment in last 1 year itself.

they are actually cross holdings even Thirumalai has a stake in Ultramarine, so you should not take it on face value

I really dont understand what’s so special about their business which helps them clock 25% RoE as this is a classic B-B company and more so faced with some great brands as customers who will have all the bargaining power - can someone please enlighten why this kind of return ratio should be sustainable.

Or is the stock price growth only due to 20% holding in Thirumalai Chemicals.

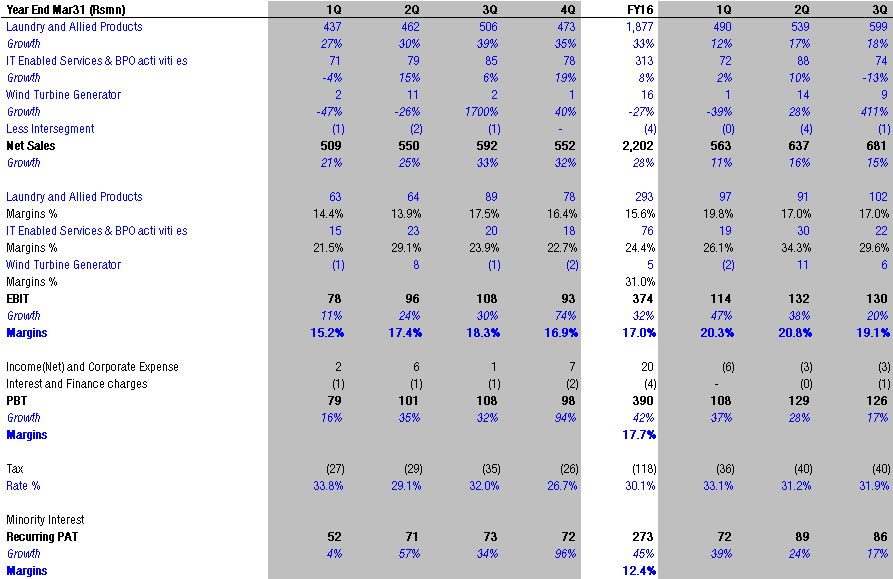

Seems like decent numbers again from the company for Q4.

Hi @vnktshb . I have been following this thread from some time and all the metrics continue to be strong. How do you compare it with Poddar pigments? I am wondering whether there are some tailwinds in the industry which have been helping companies in this segment.

Appreciate if you have any insights.

I have been invested in both Poddar and Ultramarine from last 1 year purely based on the strong metrics and understanding from VP forum.

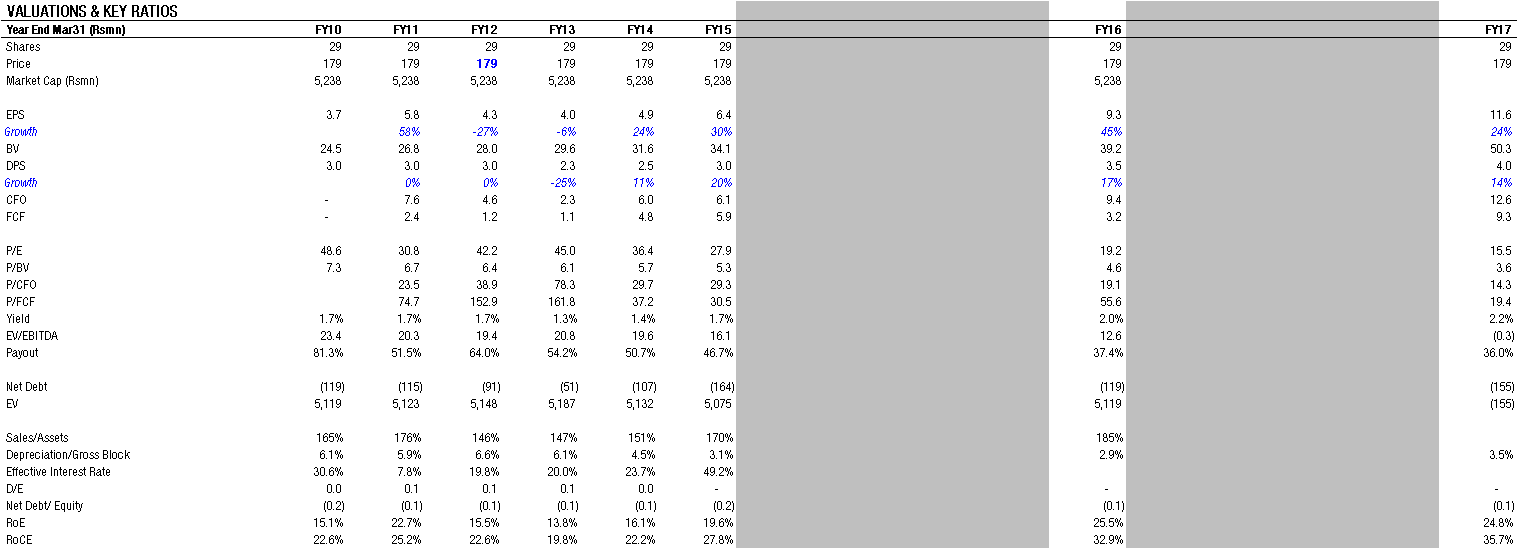

This company has been a steady performer in past several years. It has great balance sheet, comforting dividend, also its 20% stake in Thirumalai Chem. But what I am not sure of its future outlook. What are its expansion plans ? What is it going to do about its non core IT business etc. Is the management hungry enough ? The company has no presentations, con calls and their AR does not give much insights. At current valuation of 17 PE. It looks fairly priced ? May be growth oriented chemical companies like Bodal/Aksharchem look more attractive ? Curious to know what other investors think of the story at this stage ?

disc: invested at lower levels