Ugro, Monthly - Trading outside of ~2 yrs downward trendline. There’s a nice narrowing consolidation in a symmetric triangle.

The business is very well covered in its own thread and deserves a read top to bottom as pretty much every aspect of the company from its formation, capital structure, vision, promoter background (his religare group CEO role also discussed in the thread) and co-lending model are discussed in great detail. I learnt pretty much everything I know from the thread and the resources in it along with the PPT and dhruva’s blog on ugro and incessantly pestering @nirvana_laha who understands the business better

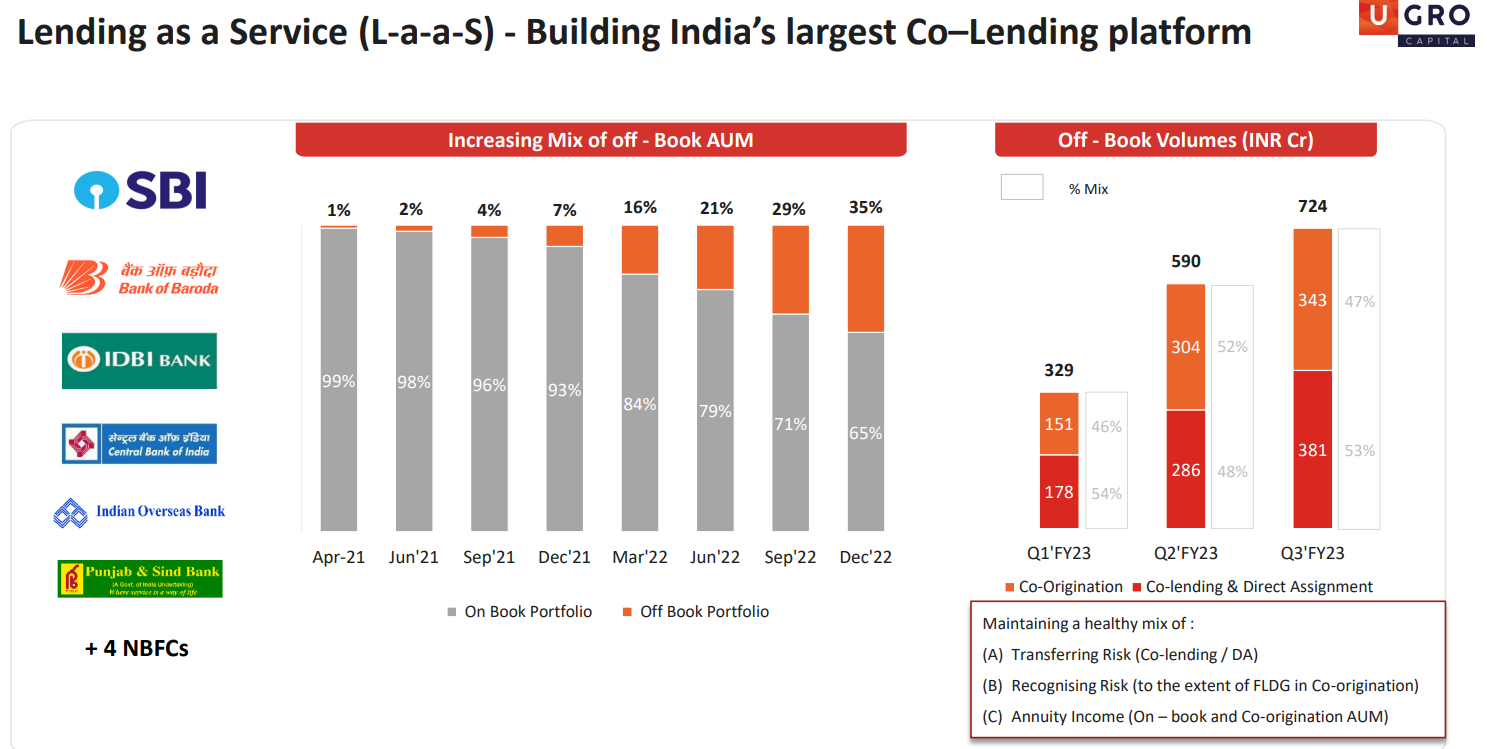

Some bits I think worth a look at from @Chins post. It is interesting that you can lend lower than your cost of borrowing and still make good return on the 80% of the off-balance sheet book transferred to the bank (in Ugro’s case SBI or Bank of Baroda).

This model appears to be good for all stakeholders from the customer, Ugro and the co-lending bank (SBI or BoB) as customer is able to avail a loan which otherwise would have been difficult, Ugro earns a fees outside of its book for the reach and the bank can fulfill its priority sector lending obligations if any.

The question I tried to answer over the last few days is if there’s a moral hazard. Since the underwriting standards are agreed with the bank, and the Ugro is board-driven, odds are low. Still co-lending with a ICICI will be very different from a SBI in terms of agreed underwriting standards I would presume.

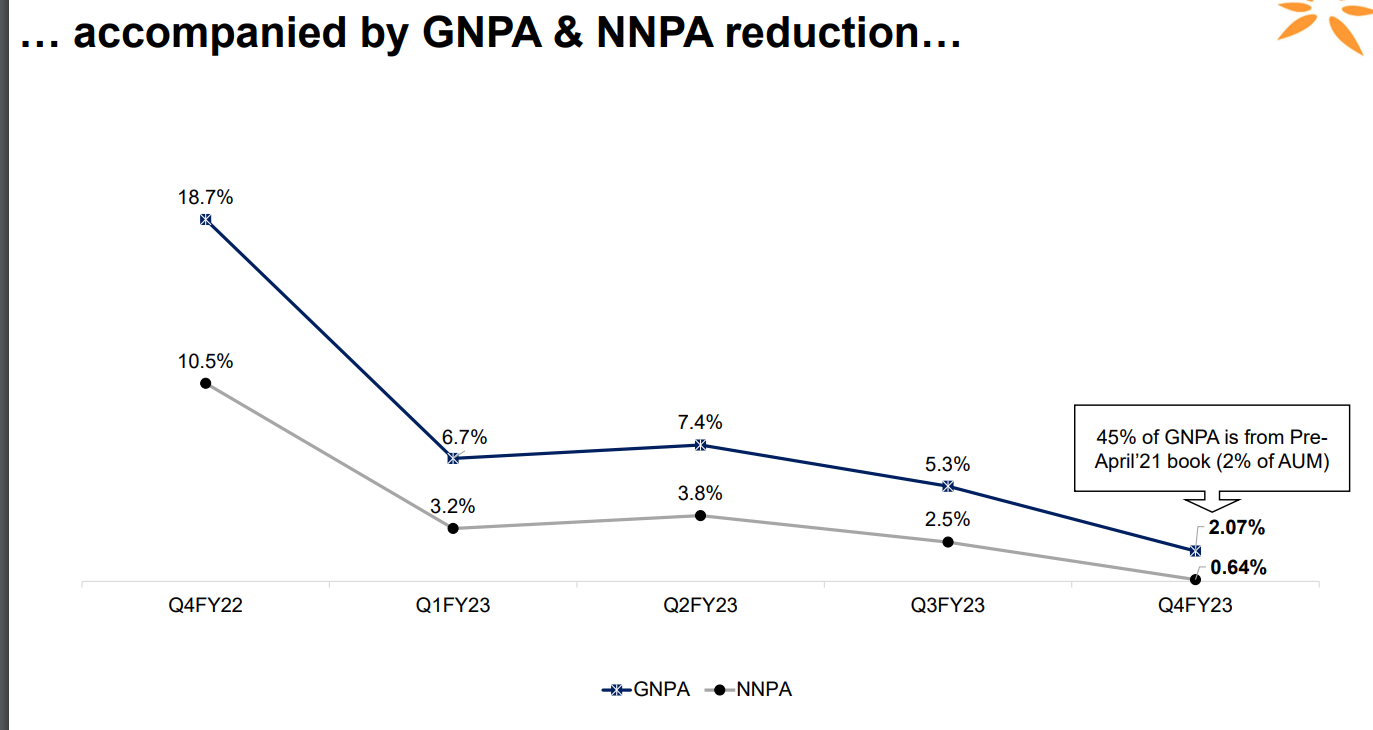

The company seems to be doing well in terms of the targets for co-lending book and AUM. As of Apr, off-book portfolio is already 40% and is expected to be 50% by FY25.

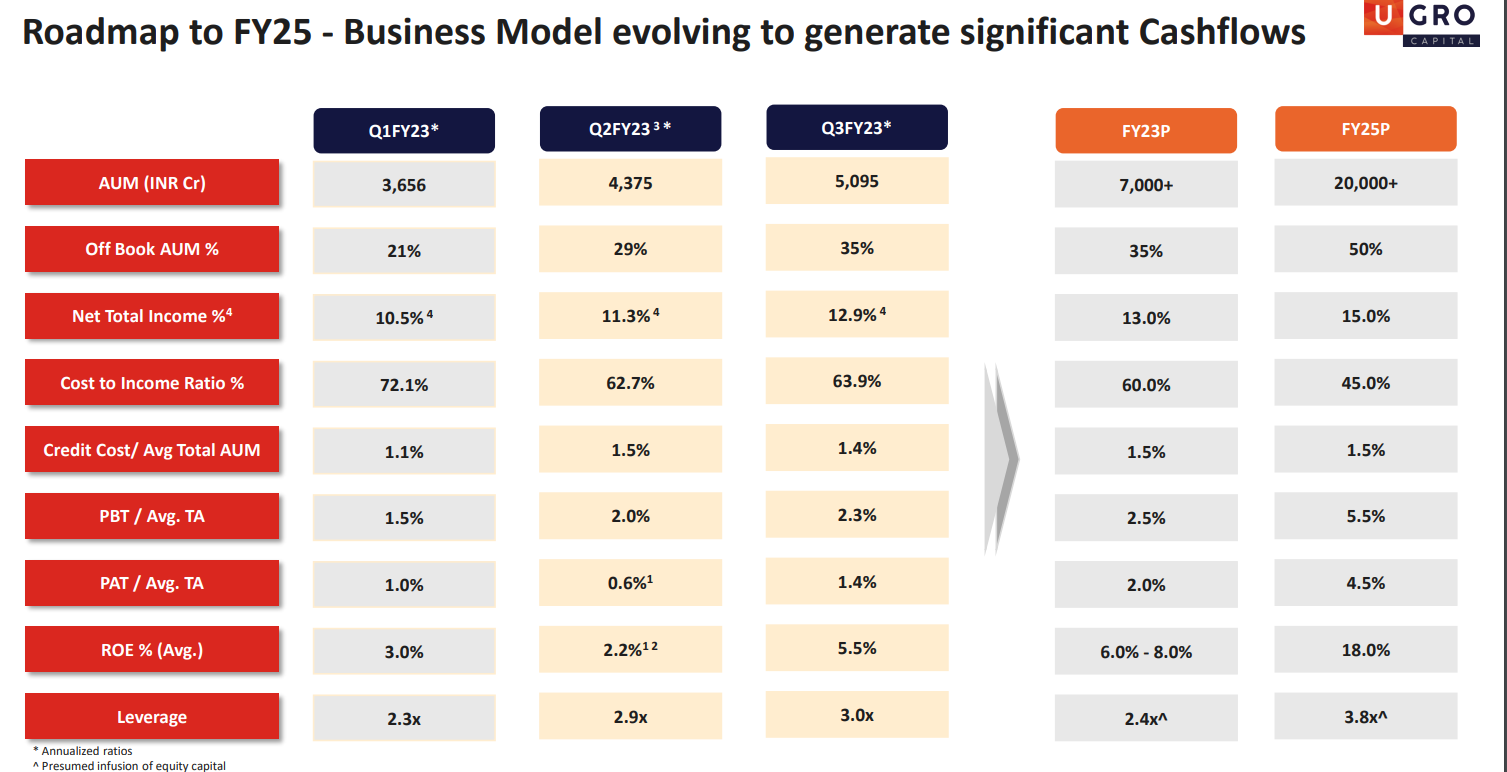

The thesis is fairly simple then that the RoE should trend up in the next two years exponentially towards 18% levels as all the hard work done by the business in the last 2-3 years is at its payoff period. The valuation today doesn’t factor it and I believe book value can get to 2000 Cr in 2-3 years (currently at 1350 Cr) and being a mature business by then with lot of expertise in underwriting in 8 sectors and its sub-sectors could trade at 2.5x book or at about 5000 Cr market cap, implying there’s a chance to make 2-3x here in ~2 years.

Risks:

- Underwriting hasn’t seen cycles and is an unknown

- Co-lending partner banks like SBI/BoB may not have very sound underwriting principles

- Unsure of the length of co-lending partnerships. Any closure and non-renewal can put the AUM targets and growth at risk (Long as NPAs in co-lending is lower than SBI/BoB’s I dont see why they shouldn’t renew)

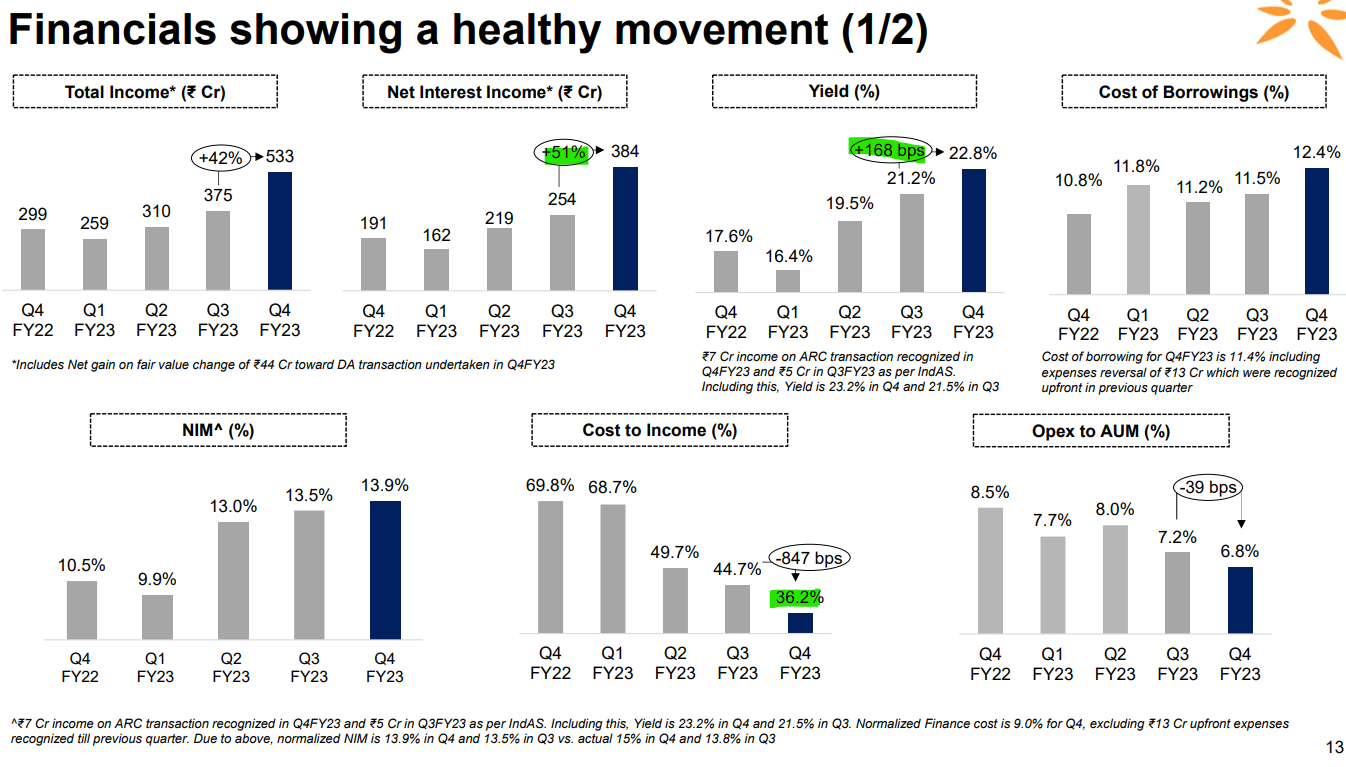

- Cost-to-income is high but as per management guidance should trend down from here as most of it is front-loaded

- DBZ has completed exited and their exit kept the price under pressure for 1.5 yrs. Any other PE exiting will be a risk

- Market may not see past promoter’s past at Religare even if evidence points to the contrary. These perceptions though change with price

Spandana, Monthly - Sideways consolidation for 8 months and this month could be the breakout month. On the weekly it has already closed at its highest since Sept '21.

Fundamentally a similar play as Ugro - the business has been undergoing a change under new management and most metrics are trending up since they took over. Unlike Ugro where good RoE is in the near future, here its already underway with recent quarter RoE at 14% and it should trend higher from here.

The quality of the book hasn’t been better

Cost-to-income trending lower, NIMs trending up, yield trending up (management guiding for 25%). Pretty much everything going right and seems to be in a goldilocks scenario here.

Unlike Ugro most things are already in place here for a re-rating of the P/B. I believe book value should grow to 3600 by FY24 end and a 2.5x P/B can make this trade at 2x current valuations. These are simplistic estimates to get a rough idea of the upside. Risks here are the usual MFI political risk and the underwriting risk but the valuation offers a lot of comfort for the bet.

These bets I think are fairly similar to the IDFC First bet. The rate cycle I think should favour this sector going forward. Hoping for the best.

Disc: This is not a sector I have any expertise in so these bets are a way for me to get out of my comfort zone and explore. My thesis could be completely flawed, so please do your own research. I have positions in Ugro from 175-195 levels and in Spandana around 630-640 levels - both taken this week