Trent is still in stage 2 and above all 3 weekly EMAs, 10 week EMa, 30 week EMA and 40 Week EMA…no sign of slowing down. Results are overall good. I will keep holding and riding till it doesnt give reversal signal.

4 Likes

Not commenting on technical as i still don’t understand them, But apart from revenue growth, results are not so good.

Anyway, have not yet decided whether to sell or not. Long Term story is intact so in two minds basically here.

2 Likes

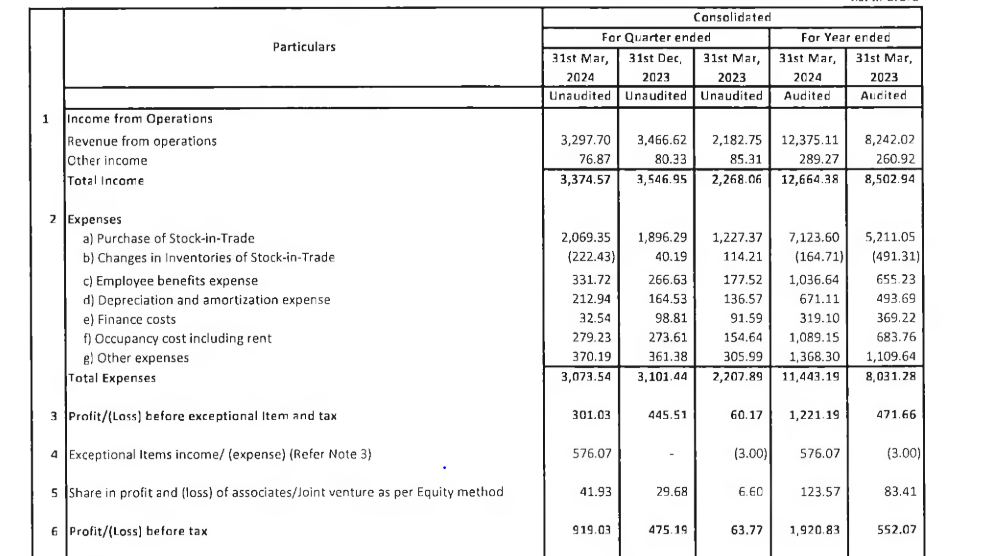

Results of Trent looked extremely good for me and I’ve observed people had a different understanding in the forum. So, here’s my take on the Q4FY24 results:

Consolidated results:

Revenue has increased by 51%.

PBT without exceptional items and tax has increased by almost 5x to 301 crore.

There’s an additional profit of 42 crore from JV’s(I assume it is from Star).

Focussing on exceptional item,

One time income: 543 croree

Tax: 137

Net income: 406 crore

Let’s try to calculate PAT without exceptional item:

Total income reported: 712 crores

Total income without exceptional item: 712-406 = 306 crores

Conclusion:

Q4FY23 PAT income: 45 crores

Q4FY24 PAT income: 306 crores - ~7x jump in profit without one time gain.

It looks like an fantastic results on all fronts.

Could others explain why do you think otherwise?

Disclosure: Invested

9 Likes

The business keeps delivering and stocks keeps on retaining its expensive multiples. Was just surfing through and came across MISBU a brand by Tata trent its in same concept of MINI SO. MiNi SO caters to luxuary need of middle /upper class from fashion accessories to small items of daily use . Difficult to explain a store visit to mini so may help.

I have visted miniso and items are not so expensive so you end up buying thr 49 & 99 & 149 ones and eventually total bill adds up well.

Its a great scalable model i believe it gives feeling of buying more at less. Excited with the concept of MISBU and growth potential going forward.

Invested since quite a a few years. No recent transactions

9 Likes

@rahil_sayta , Since you are holding for many years…Trent PE multiple goes higher and higher…so if tomorrow numbers dont match the expectations, and price start falling, what are your exit plans ? Have you formed any exit strategy and if not why?

Hi Mudit trent has been an amazing growth story for me . I havent yet thought of exit startegy for trent as i personally feel with country like india it has a lot of room to grow. For a conpany like trent where already a lot.of wealth is created personally i would be happy even if it doubles in 4-5 years.

For a company of size of trent a year or 2 of slow growth and may be i would look for switching though some part of gains could be given back in the process.

This is a part of largecap portion of the portfolio where i dont expect lot of magic. Though it happened by luck in last couple of years

7 Likes

Rahil, it’s the same here, I am able to find reasons to sell but have held off the sell button maybe for subconscious reasons.

Only trigger maybe 2-3 quarters of sub normal growth especially in STAR and Zudio.

Have you looked at slowing down of ZARA. H&M and Uniqlo are giving serious competition here. I mean Uniqlo with predominant online strategy is racing at a very fast clip and products are good.

1 Like

Trent has an ROCE of 22%.That’s a fantastic return and not only that, it outpaces the average of 17% earned by companies in a similar industry. The trends I’ve noticed at Trent are quite reassuring. The data shows that returns on capital have increased substantially over the last five years to 22%. Basically the business is earning more per rupee of capital invested and in addition to that, 183% more capital is being employed now too. So I am very much inspired by what we’re seeing at Trent thanks to its ability to profitably reinvest capital.n summary, it’s great to see that Trent can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. And a remarkable 1,105% total return over the last five years tells us that investors are expecting more good things to come in the future. So given the stock has proven it has promising trends, it’s worth researching the company further to see if these trends are likely to persist. However my worry is that TRENT has a high level of non-cash earnings.

Disclosure-I am invested for more than 20 years and my levels of buying were very low, levels, made a mistake of selling 500 shares @ 600 during covid and recovered my capital. This stock has become a Major portion of my portfolio 60%+ and that is my big worry. Suggestions on trimming down are welcome as I am in a dilemma.

4 Likes

It also happened because of the business understanding of different segments, the building of business base for many many years and excellent execution of the management & promoters…

curious back in 2004 ans earlier what must have been the reasons for your buying? I wish you were in this forum early to share your insights. 20 years back if I am not wrong, Trent was not a good performing business and likes of big bazaar, Pantaloons was the talk of the town…Also was Trent a high PE stock back then also or must be in Red with no profits?

If you could share When was your first entry and how did you build your position? Was it in lumpsum one time buy & forget or a conscious gradual building of position? Also when was your last buy? It seems your average buy price is around Rs 25!

Would be good to know your thoughts as would like to learn from those who catch such multibaggers much much before their time and results arise.

1 Like

Thanks for your comment. Actually I was a share holder of Lakme Ltd and the Brands were sold to HUL and a lump sum was distributed to the share holders. The management created Trent with remaining money from the sale proceeds. All shareholders of Lakmé were given equivalent shares in Trent I invested lumpsum received in Trent, then there were rights issue in 2005 and 2006 and I built my position then, after that there was no addition. I recovered my investment by selling some quantity during Covid. I always had faith in Mrs. Simone Naval Tata, a Swiss-born businesswoman married to the Tata family. I was fortunate to meet her in person twice. She was the main architect of successful brand Lakme. She had great vision of launching a female centric fashion retail business in India in early 2000 when nobody even thought of that. I actually thought of selling my position during 2008,but those days it was difficult to sell as the shares were not in DMAT, the procedure was cumbersome for person residing in a tier 2 town. The time was full of gloom and I stayed away from stock market for next 3 years. Fortunately for me I did not sell any of my share holdings by sheer luck. The stock was already a multibaggar & became 6x during 2003 to 2006. I am old school type and I don’t sell any of my stock as long as the business model is intact, and I am not in need of money. Only exception was during Covid, as I built a big corpus in my savings account for emergency hospitalization to take care of 4 persons responsibility. I have seen 2-3 bear markets and experienced that if a business model is good eventually, you beat NIFTY in the long run. The problem I face is of position sizing during a bull run so as to have a downward protection of gains before the cycle turns. This problem I am facing again. Like most of us, I am unable to predict, when the cycle will turn and analyst are bullish on earning growth of Trent. I keep things simple ( I have limited knowledge) and track ROCE performance in the long run and if it goes down I reasses the business model. Please share your suggestions on position sizing.

10 Likes

For position sizing i had met some one who had a few crs of shares ( 80% ) of networth he was CFO when he retired. Stock was at 100 and came down to 20 due to debt and macro headwinds .

Inspite of being worked so closely he coudnt see it may be thats true for HDFC bank as a stock and share holder ( disclaimer a long term holding for me )

From that time my learning was nothing should be so substantial as a part of my portfolio that loosing 50% of that or stock not moving (time correction ) affect my portfolio in negative way.

Personally if a stock is a very high allocation for me i will have a hawk eye will use fundamental +technical to take a call on it .

@hardik_shah1 uniqulo is good brand and so is H&M . I feel zara segment is quite different (luxuary wear ) .

You will hardly get daily wear or casual wear in zara .

I think there still exists a gap where there is a segment above westside which is not captured which H&M very well captures .

This could also be a big opportunity if westside can capture this space with good quality and not very high price. Slowdown of westside i feel is because of trying to place product between the 2

So lower strata will not buy from.westside and affluent (rising middle class) will want to be more aspirational and go to higher brand.

Management has been very sharp lets see how they can steer the growth going forward

2 Likes

What I have seen is all zara and Uniqlo operate in range of Rs 2900-6000 for men’s shirts and trousers across varieties. Products worth 8000 are zara originals which you would call premium.

H&M is on lower side I agree.

Rest of your analysis I agree. But building an brand positioning and brand value in consumer minds is extremely difficult. Changing it is even tougher. Probably they need a third brand besides zudio and Westside to capture that space.

Hi Rahilji, Thanks for your comment on position sizing. Right now I do not have a investment idea with good valuation, as valuation are sky high, though I am trying to evaluate SGMART’s business model, it is a tech-enabled premier B2B one-stop shop that provides a wide range of construction-related solutions. , but I don’t find much data, I welcome suggestions from the group. it is at PE of 71+. I am considering to start selling Trent slowly and park the money in NIFTY 50/Debt fund(50+50) till I find a good business model with good valuation. I will start reinvesting in Trent in case there is a big correction . I do not find any negatives in Trent, except high level of non-cash earnings. I may be biased, please share if you have noticed negatives or other risks in Trent. I am unable to discover a better Idea than Trent with good valuations right now.

Trent down 5.8% today. Is the market anticipating a bad result? any comments

Its a overall matket fall. Most momentum stocks are down

Let me ask you a question - Had you been worried about position sizing and kept hawk’s eye at it - Would you have let it become 60% of your portfolio? The fact that it became 60% of your portfolio signifies that you are so far comfortable with that amount in absolute terms as a part of your total NetWorth. Pls correct me if I am wrong.

Personally, Trent has become my almost top holding, currently in competition with Tata consumer with almost 15% of portfolio each. Would I be worried about my position sizing if any were to become 60% of my stock portfolio…would depend on factors such as what does the remaining 40% constitute and how much my stock portfolio forms a percentage of my total net worth along with my liabilities etc.

Its not a straightforward answer in case of such high quality, top promoters company. Had it been any other second rung momentum stock, decision would have been super easy. Also, factors like - which sector stock it is that has reached 60%…an FMCG may not fall as much say a retail company if things go bad…and also do I need the money or can ride the troughs if I believe in the company etc. etc.

Decision is never easy and I feel there is no rule. It depends on various factors. Lastly, I may not be eligible for advice as I haven’t reached that stage yet with a single company rising so high in my portfolio that it breaches the 40-50% mark of the overall stock portfolio! I think I may have chosen “peace of mind” as a criteria to decide the upper limit rather than any mathematical model.

Disc: Not a buy/sell advice. Views are personal and only for academic purposes. Not eligible for any advice. I can be wrong in all my assessments

3 Likes

Thanks for your reply, Trent was at 1700 level last year July and was 35% of my portfolio. In last 10 -12 months the the momentum was so strong that the stock more than tripled from its last July level. It was difficult for me to exit as I wanted to ride the momentum, Trent has almost doubled my entire equity portfolio in just 12 months. This is a pleasant problem to have. I am 59 and have 55% in equity. Normally I keep only 45% in equity and 55% in debt funds, but this excess in equity is thanks to bull run, I am going to rebalance slowly to make it 50/50. The problem is when to start reducing Trent. I am not in a hurry as I already have my expenses covered by interest income on Debt part of my portfolio. I have experience of my equity portfolio going down by 60% and then recovering back. I plan to go passive when I reach 70.

7 Likes

Your logic seems good. It may be pre budget profit booking by those anticipating changes in LTCG on 23rd July.

1 Like

Each individual sell decision merits its own specific industry/business cross-examination, let me share some generic insights from my little experience base - perhaps some of these may resonate with others as well. Markets are inherently forward looking - even in bear markets. So 1-year forward is the base rate. In bull markets like current, 2-year forwards become the optimistic norm - such as what we are experiencing now for most businesses. I have seen I don’t get too worried when valuations are within 2-year forwards. When valuations exceed 2-year forwards and start approaching 3-year forwards, I will find myself uncomfortable and perhaps sell.

Forward PE of Trent Ltd for next 5 year -

Current Share Price: ₹5,835.45 (as of July 31, 2024)

Current EPS: ₹40.39

Assumptions for Future EPS Growth

Given that Trent Ltd. has demonstrated strong earnings growth, we can use the historical growth rates to project future EPS. The company has shown an average earnings growth rate of approximately 60.8% per year over the past few years . For our calculations, we can assume a conservative growth rate of 40% for the next few years, considering market conditions may vary.

Using the assumed growth rate of 40% for the next five years, we can calculate the projected EPS for each year as follows:

- Year

- EPS = Current EPS × (1 + Growth Rate)

- EPS = ₹40.39 × (1 + 0.40) = ₹40.39 × 1.40 = ₹56.55

- Next 4 years- Similarly year 2,3,4 and 5th EPS is projected as ₹79.17,₹110.83,₹155.16 and ₹217.22

Forward P/E Calculation- Year 1: 103.93,Year 2: 73.66,Year 3: 52.63,Year 4: 37.56,Year 5: 26.87

What I have seen is as long as the growth keeps coming, the stock price does not correct much. We saw this in many many cases, Astral, Mayur, Poly Med etc.… At most the correction is 10-15% due to extraneous factors. The business looks overvalued, but the business growth is intact. So, the idea then is to not second guess the market. I don’t know if 200+ PE is high or low. The market may decide to give it 200+PE, like it did to Infosys at one time. The approach, I am contemplating is because I am 100+x up, I will put a trailing stop say 30% below the high price I have seen. If my thesis is correct, it will not correct that much from the recent top, but reverse and continue it’s upward journey. And I will keep revisiting my stop upwards to that 30% mark.

The only practical problem with this approach that I may come across is what to do when the stock just flat lines and does nothing. Like PI some time back. Then the SELL decision may be based on my understanding of their next 2-3 year growth prospect. My knowledge is very limited and I am biased so Please Comment on my thinking direction. Disclosure-Please note there is no buy and sell recommendation on any the stocks mentioned above. I am invested in Trent for 20+ years

3 Likes