Of late I am writing this topic after going through multiple reports about the retail industry and different players in this industry. So you can find a nice summarized view of the industry and the reason I choose this company from the sector.

The Indian organized retail although undergoing constant disruption, one thing has remained steady but consumers’ affordability is on the rise and aspirations are growing more than ever. It is expected to get tripled by FY25 with a CAGR of 22% and 27% in F&B and Appreal segment respectively. Household retail spends, too, are shifting from traditional kirana shops to modern retail formats, which are gaining share due to better price offerings and greater convenience of shopping. To cater to this demand about 4000 retail store opening is needed as per Motilal Oswal estimate.

Indian retailers have seen healthy expansion in their store footprint, driving revenue and earnings growth. Unlike the previous cycle in the early 2000s when euphoric expansion in retail footprint led to a sharp fall in store profitability and eventual rationalization and downsizing, the existing retail expansion is far more measured and primarily fueled by internal accruals and not leveraged expansion. To reduce operating cost and drive an efficient working capital cycle, we see most companies focusing on (a) leaner store layouts, (b) cluster-based growth, (c) private labels and (d) membership-based model. This has led to an improvement in per store economics and an expansion in the EBITDA margin across retail companies over the last 2-3 years. The outlook on the returns profile has also improved significantly.

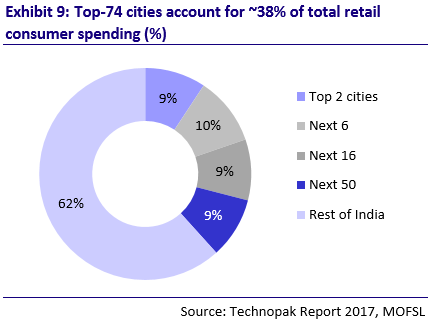

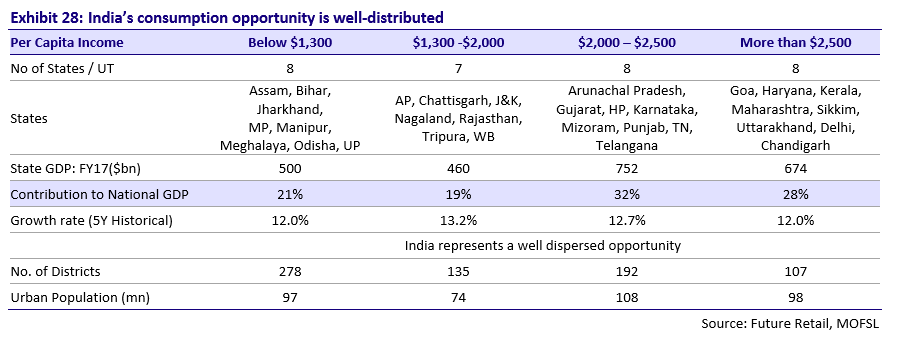

The top-24 cities (metros, mini-metros and tier-I cities) account for 29% of total retail spending, with the Delhi and Mumbai clusters contributing about 9%. Even the top-72 cities account for 38% of total retail consumer spending, which highlights the strength of rest of India that has 71% share. Major expansion in terms of retail consumer spending is expected to come from India’s tier-2 cities. This should benefit the value apparel category, which is a much attractive option for customers. Pricing difference between unbranded and branded apparel is ~4x, but value category products come with just 2x higher pricing. Thus, more apparel players are increasingly expanding into tier-2 cities to tap this opportunity.

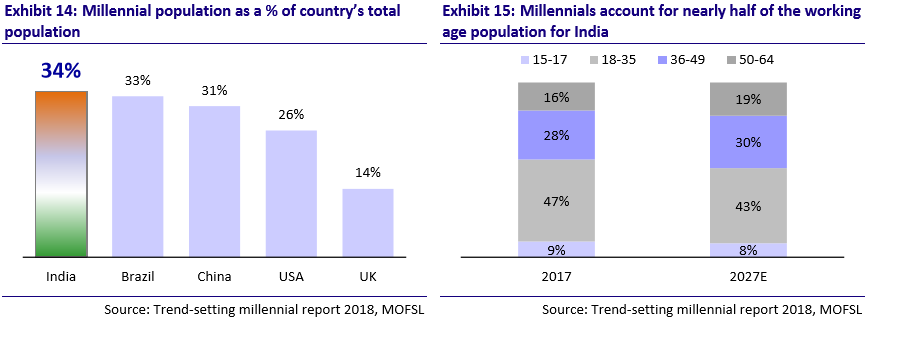

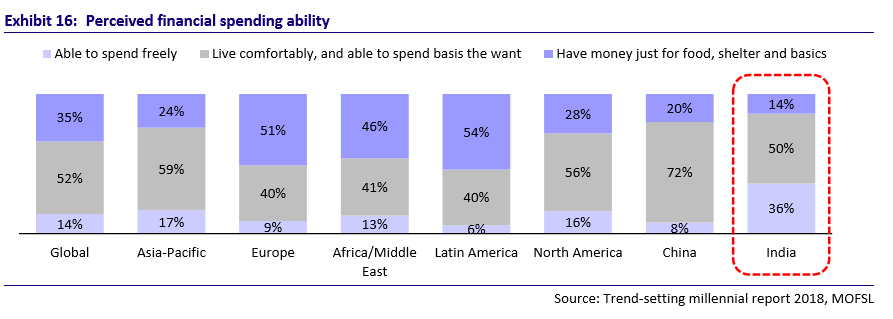

In absolute terms, India is blessed with the largest millennial population (age bracket of 18-35 years) globally. With a population of over 440m, the group constitutes ~34% of the country’s total population. Further, with a median age of ~26 years, India is one of the youngest major economies and is expected to stay so in the foreseeable future. This is in contrast to other countries such as the US, large European countries, China, etc, where the median age of population is higher and an imminent situation of declining working-age population looms the markets.

The Indian millennials stand out from the rest of the population in terms of better education, lifestyle choices, consumption pattern, significant need for convenience, and brand preferences. Millennials spend a high proportion of their incremental income towards eating out and entertainment (32.7%), apparel and accessories (21.4%), and electronics (11.2%) among others. Savings account for ~10% of the income. This indicates a shift towards a consumption economy rather than a savings economy, which was a predominant feature of the preceding demography. Millennials, with their low inclination towards savings and increasing spending capacity, provide brands with vast growth opportunities. With a high and growing millennial population, modern retail, organized apparel sector should get a push.

Households with annual earnings of USD5,000-10,000 have grown at a CAGR of 17% over FY11-16 and are projected to grow at a CAGR of 12% to reach 109m in FY20. Households with annual earnings of USD10,000-50,000 have also grown at a CAGR of 20% over the last five years. Increase in the number of households with annual earnings of USD10,000-50,000 will lead to an increase in indulgence spending by the group. This will lead to an increase in expenditure on consumption categories such as Food, Fashion, Luxury Products, and Consumer Durables. It is estimated that 23% of the global middle class will be from India by FY30.

GST has allowed business owners to start their business faster through a centralized registration process in which they do not have to worry about individual state requirements. With the implementation of GST, the movement of goods across states is becoming easier due to a standardized set of rules in place. Warehouses are not needed in every state and this will help companies reduce costs. Organized players with an all-India presence should benefit and inflows to the formal economy should increase. Digitization should allow businesses access to a larger market.

Organized retail – Huge runway of growth

Presently, the organized general merchandise players in India occupy 40-45msf area of retail space as per Technopak. This is estimated to grow to 60-65msf by CY20, that is, 14% CAGR over CY17-20 to cater to 21% organized retail growth, indicating 7% SSSG. Assuming a blended store size of 20,000, overall 1,000 new stores will be required over the next three years to cater to the growth in the organized retail market.

One of the key positives of the retail market growth is that it offers a strong and long runway for growth. With a high single-digit GDP growth, the retail space should continue to grow at 14% until FY25. This is assuming (a) overall retail market grows at 12%, at a pace of 1x nominal GDP growth, (b) organized segment continues to grow at 1x overall retail growth, and (c) SSSG is 6%. At 20,000sf blended store size, over the next eight years, to cater to the growth in the organized retail market, 3,900 new stores are required, highlighting the huge scope of growth for all retailers. This implies organized retail penetration of a meager 17% in 2025, highlighting the huge demand in the organized retail market.

In the helm of all the above mentioned factors it is quite obvious I will choose a company which satisfy my investment style. Although many organized retailers available in this apparel domain like Future Lifestyle, Shopper Stop, Aditya Birla Fashion etc. but I choose Trent mainly due to the below factors.

- It is a value unlocking story by restructuring it’s existing stores which is evident by it’s best in class SSG growth in the last year.

- It’s focus on store expansion to drive the revenue along with operating efficiency to improve the margin.

- Value retailing via Zudio brand which is poised to see exponential growth in next couple of years.

Trent mainly operate in 4 devisions:-

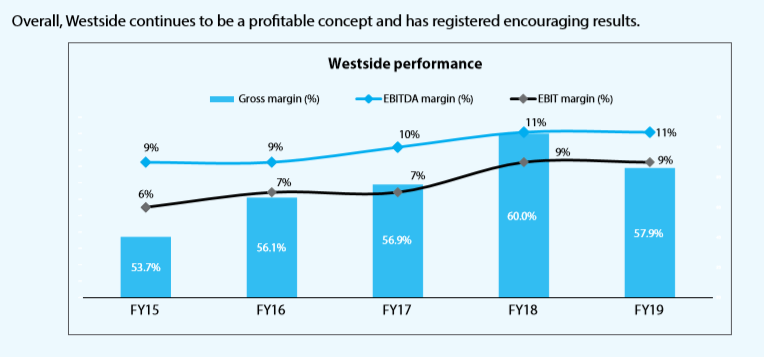

- Westside:- A premium to mid range apparel brand which contributes to 85% of Trent revenue and expected to grow at 17% CAGR.

- Zudio:- A value retail apparel brand which contributes 7-8% of Trent revenue and expected to grow at 50% CAGR.

- Zara:- Trent holds 49% stake in its JV - Inditex Trent Retail India Private Limited (InditexTrent). However, the operations of Zara and Massimo Dutti are controlled by Inditex (in entirety), whereas Trent has primarily been a financial investor. After the revival of margin in FY18 from the impact of countervailing duty, we can expect healthy 20% revenue CAGR and 16% EBITDA margin over FY19-21. With FY21E EBITDA of INR3.5b, Zara could garner healthy enterprise value of INR42b at 25x EV/EBITDA, ~33% of TRENT’s overall value. Over the next 5-7 years, this could increase to 3540%, considering the fast evolving market for premium fast fashion products and Zara’s strong product portfolio.

- Trent Hypermarket :- TRENT’s 50% retail venture, Trent Hypermarket (THPL), which runs the Star brand stores, was among the first to enter the food and grocery retail business. However, it is yet to become profitable – negative 7% EBITDA margin (FY19E). After operating in three different formats – Star Daily (~2,500sf store size), Star Market (~8,000sf), and Star Bazaar (~20,000sf), it is now focusing on the Star Market format. It has closed the loss-making Star Daily format and is tightening the SKU list for Star Market to improve store productivity. The launch of gross margin-accretive apparel line-up, Zudio, in all 12 Star Bazaar stores should further improve store turnover and profitability. They have built in 15 Star Market store adds annually over FY19-21 (company targets 20-25 store adds annually). This, coupled with 7% SSSG, should help THPL grow at 18% over FY19-21. The closure of loss-making Star Daily stores, the launch of Zudio and the focus on the profitable Star Market format should reduce EBITDA loss to 4% by FY21, enabling THPL to reach closer to breakeven.

Value Unlocking Story:-

Zudio has adopted a unique FOCO model, unlike the conventional COCO/FOFO model used in the industry. Therefore, a franchisee’s capex is INR15-20m for a store size of 6k sqft; in turn, a franchisee receives a fixed revenue share, while the company operates the store and retains the profitability. Typically, franchisees get ~16% revenue share and 12-15% IRR, while the company garners strong ROCE on merely one-month inventory capital.

Zudio made its debut just two years ago. Since then, it has expanded to 40 standalone stores with revenue of INR1.5b in FY19. While currently Zudio’s revenue is insignificant in TRENT’s overall consolidated revenue base of INR26.3b, we can expect it to grow tremendously in the coming years. According to my estimates, Zudio will see 70/80/100 store adds in FY20/21/22, taking its total store strength to 290 by FY22. Also, we can expect Zudio’s revenue to hit INR14.5b by FY22. Thus, Zudio is expected to contribute 26% to TRENT’s overall revenue; contribution toward EBITDA is also expected at similar level. However, the estimates are conservative and still below management’s target of 100 store adds annually, which would take Zudio’s total store count to 340 by FY22, ensuring stable 6-7% EBITDA margin. Note that our estimated average revenue/sqft of ~INR8k is much below the like-to-like INR14k/sqft indicated in the company’s Annual Report 2019 .

Why Choose Trent over others:-

-

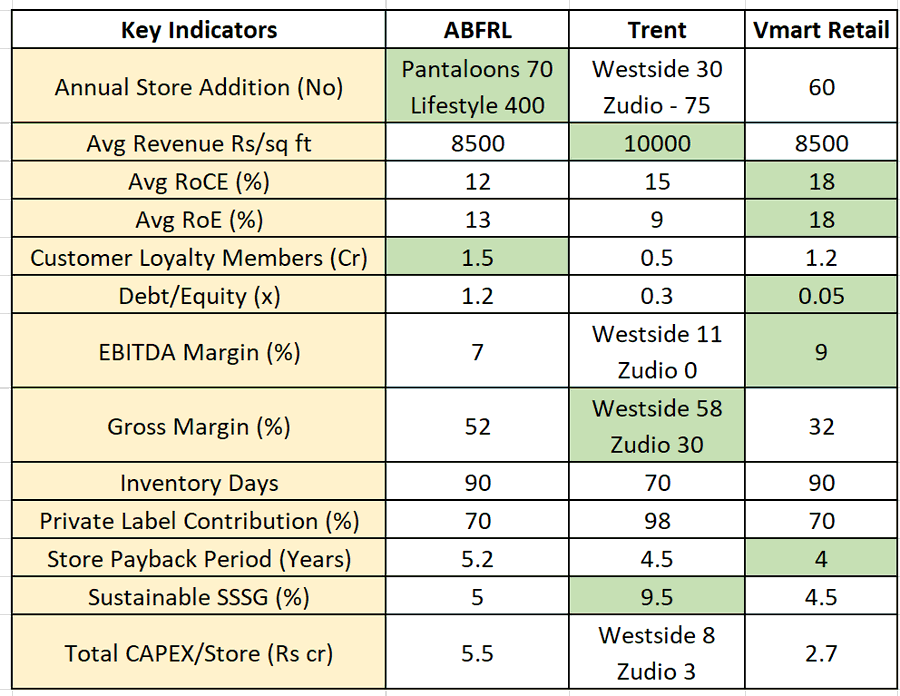

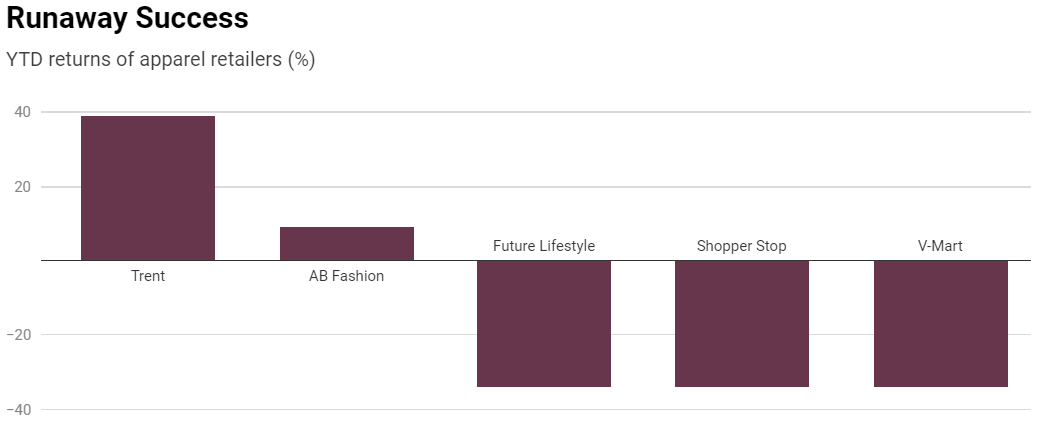

Trent Ltd. outperformed its apparel retail peers this year as its revenue rose the most and it opened a greater number of stores. Shares of the Tata Group company have risen nearly 39 percent year-to-date. Among peers, only Aditya Birla Fashion And Retail Ltd. has gained. Others, including Future Lifestyle Fashions Ltd., Shoppers Stop Ltd. and V-Mart Retail Ltd., tumbled.

Trent’s revenue grew 32 percent in the first six months of 2019-20—the highest among its peers—while its operating margin was 17.7 percent, according to its exchange filings. The company is well placed in the Indian fashion retail industry to outperform, led by its focus on fast fashion and value fashion, Antique Broking said in a recent report. -

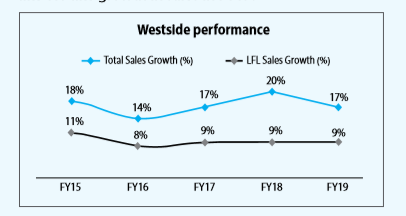

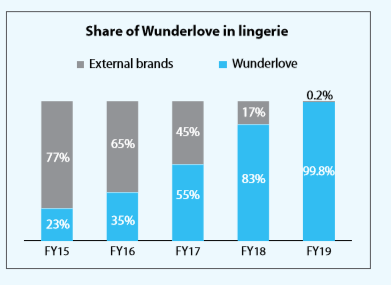

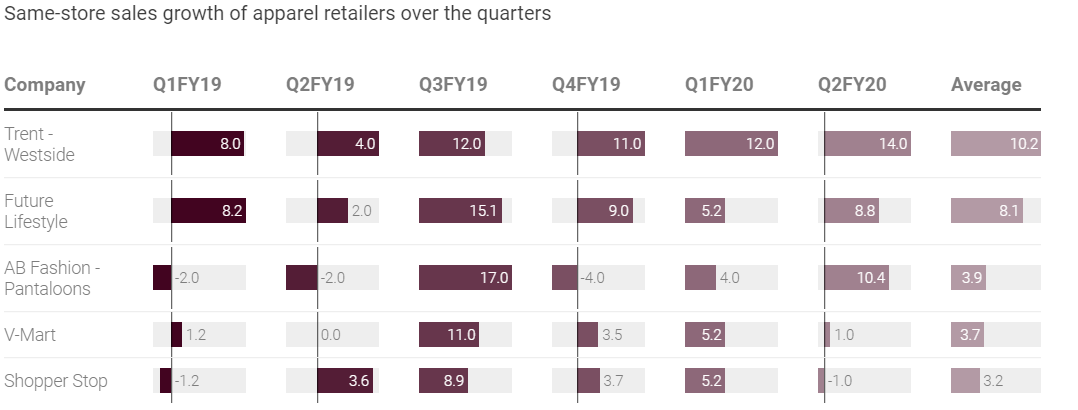

Nearly 85 percent of Trent’s revenue comes from the Westside store chain, with the subsidiary’s growth boosting its performance. Westside’s same store sales growth—or sales growth at an existing location that has been in operation for at least one year—has not only been the largest but also the most consistent in the past six quarters, according to Axis Capital. Its six-quarter average of the metric is around 10.2 percent. Westside is also the only company whose same-store sales growth hasn’t declined in the same period. That, according to Edelweiss, could be attributed to the company’s focus on private labels and enhancing the shopping experience. Westside, according to the brokerage, derives nearly 97 percent of its revenue by selling private brands.

-

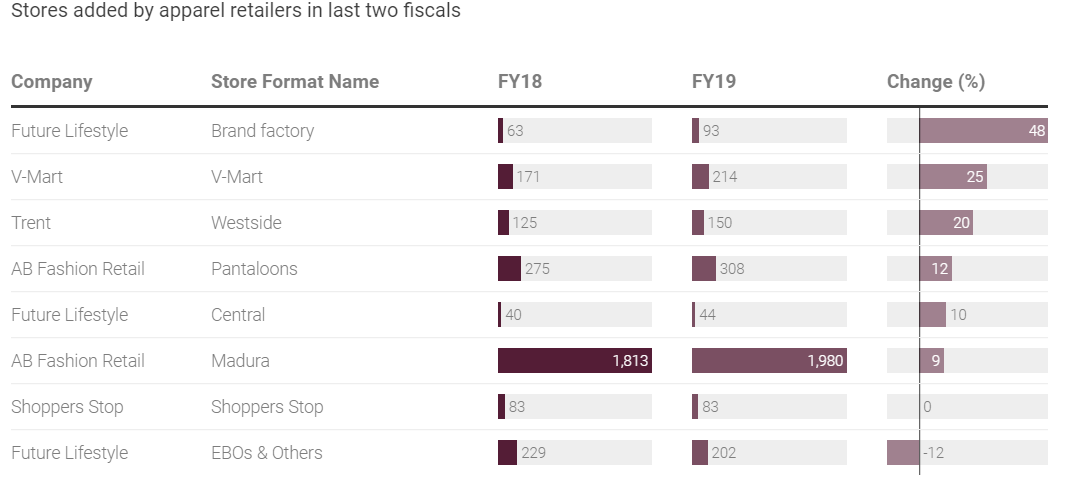

Trent’s Westside format added stores at a steady pace and has, according to data on its website, as many as 158 stores across India as of March. Only V-Mart and Future Lifestyle have added stores at a greater pace, Edelweiss Financial Services Ltd. said in a report. V-Mart’s expansion has come at the cost of its operating margin, the brokerage said, while Future Lifestyle’s grew on a low base. Edelweiss and Motilal Oswal Financial Services Ltd. expect Trent to open 30 to 35 stores in the Westside format in FY20. Trent recently acquired retailer Zudio from its joint venture Trent Hypermarket Pvt. Ltd., which had 40 stores as of March. CLSA Ltd. expects Trent to “aggressively” increase the Zudio store count to 120 by the end of the ongoing fiscal. Zudio’s products are priced at Rs 999 or below and the store owns all the brands that it sells. The store’s revenue grew 31 percent on an annualised basis over the past three years to Rs 204 crore as of March, according to CLSA.

-

Trent holds 49 percent stake each in joint ventures with fast fashion giants Zara and Massimo Dutti, which operate 22 and three stores in India, respectively. The two retail brands are owned by billionaire Amancio Ortega’s Inditex Group. Both the ventures, according to CLSA, are financial, and not strategic, investments. Trent in its annual report said that revenue from the Zara JV grew at an annualised rate of 15 percent between FY15 and FY19 to Rs 1,438 crore. Massimo Dutti India, which launched in FY19, posted revenue of Rs 63 crore in FY19, according to the report. Trent is yet to respond to BloombergQuint’s emailed queries on its growth prospects and store additions.

Valuation:-

Trent is the most expensive apparel retailer, with Edelweiss indicating an FY20 price-to-earnings ratio of 82 times. That’s at a 50 percent premium to second-placed Aditya Birla Fashion. Analysts expect Trent to rise the least. The company, according to Philip Capital, is likely to maintain its premium valuation because of its rapid store expansion.

Westside/Zudio should see higher pace of store addition at 105/250 stores cumulatively over FY19-22E. Also, we can expect TRENT’s consolidated revenue/EBITDA/PAT to register CAGR of 29%/62%/62% on pre-Ind AS 116 over FY19-22E and EBITDA margins stabilising at 10.1% by FY22E. With strong contribution from margin-accretive private labels (over 90%) and faster execution capabilities of new launches, TRENT should witness healthy growth. While the recent fund raise is expected to have a near-term impact of equity dilution on earnings growth and RoIC, over a three-year period, the dilution could drive accelerated growth. Our SOTP-based TP of INR605 values Westside and Zara at 30x EV/EBITDA and Star at 2x EV/sales on Sep’21E. Due to Zudio being currently loss-making, it has suppressed Westside’s earnings. But, we can expect valuations to normalize as Zudio turns profitable over the next 3-5 years.

Discloser :- Invested hence views might be biased. Opinions are welcome.