Not really.

Standalone ratios are very good and not a concern.

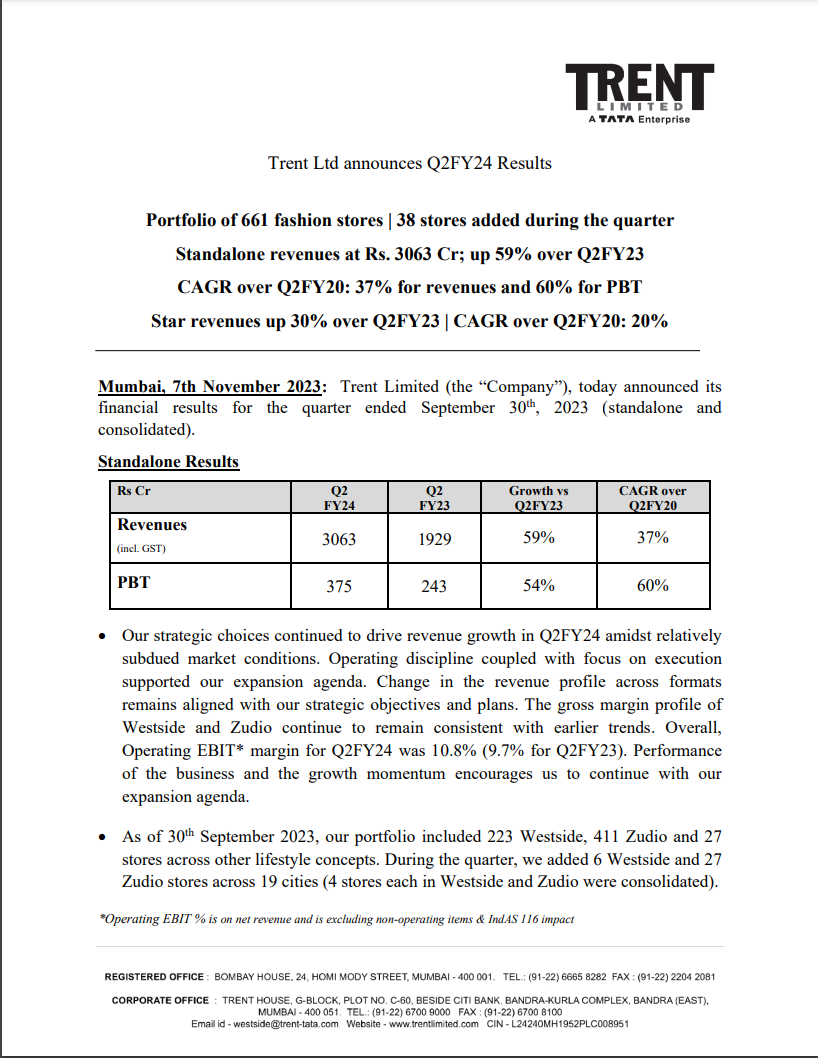

Standalone Results:

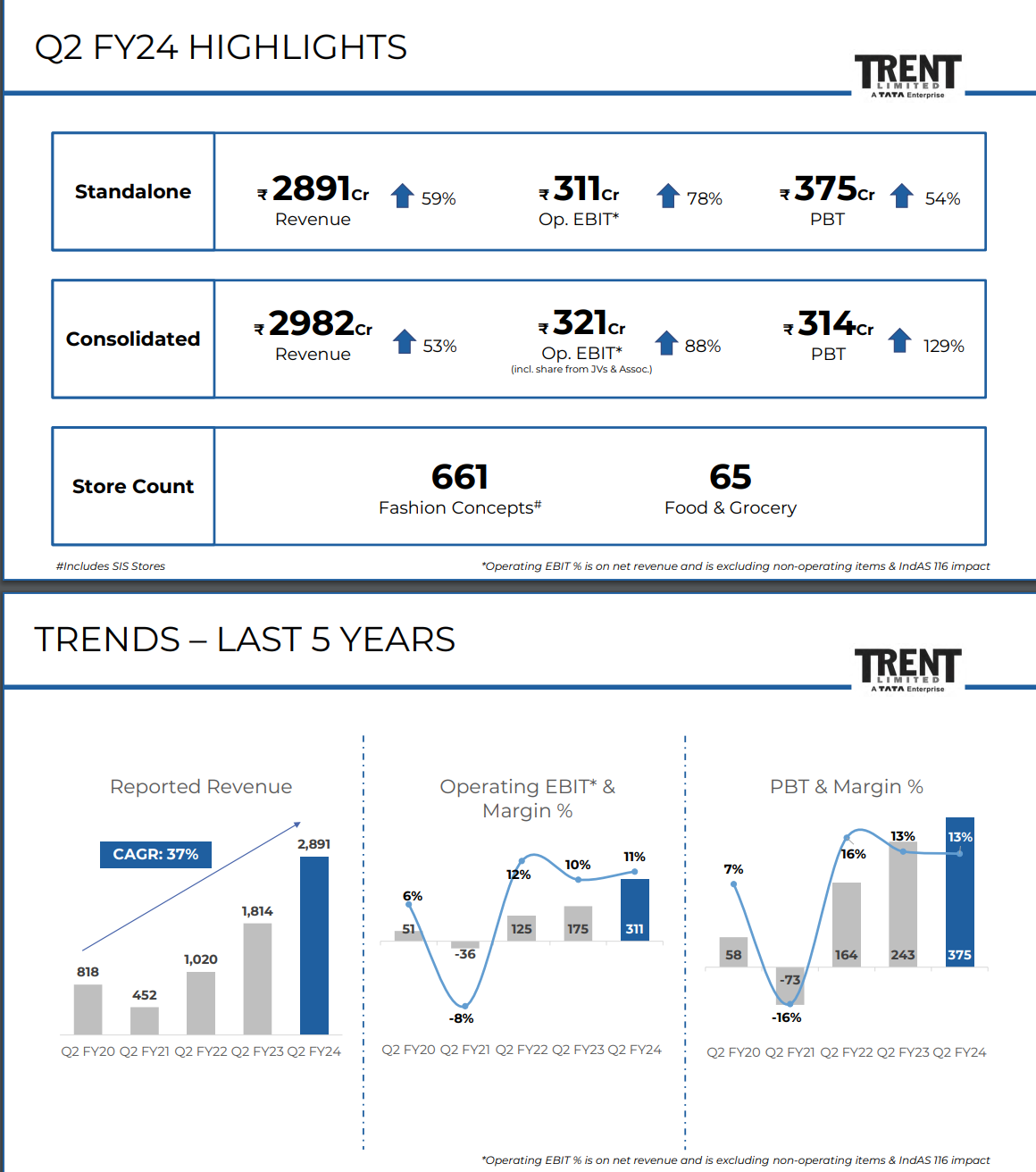

- Standalone revenues were at Rs. 3,063 Crore, a substantial 59% increase compared to the same quarter in the previous year.

- Profit Before Tax (PBT) for this quarter was Rs. 375 Crore, reflecting a significant growth of 54%.

- Over the past few years, there has been a Compound Annual Growth Rate (CAGR) of 37% for revenues and 60% for PBT, which is a strong indicator of the company’s growth trajectory.

- The Star brand’s revenues were up 30% in comparison to the previous year, with a CAGR of 20% since Q2FY20.

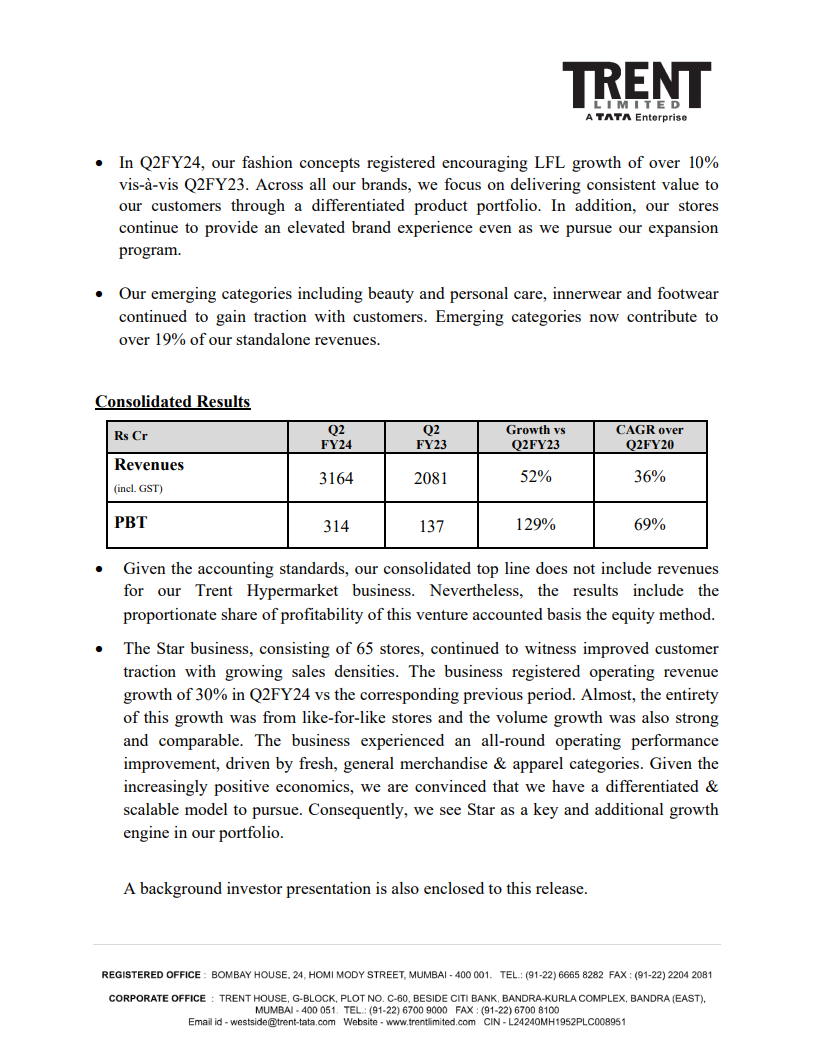

Trent Limited’s strategic decisions and operational efficiency have contributed to revenue growth, even in challenging market conditions. They have been focusing on expanding their store network and maintaining consistent gross margins. The Operating EBIT margin for this quarter stood at 10.8%, up from 9.7% in the same period last year, which is a positive sign. The company’s performance and growth trends support their plans for further expansion.

As of September 30, 2023, Trent Limited’s portfolio included 223 Westside stores, 411 Zudio stores, and 27 stores across other lifestyle concepts. In this quarter, they added 6 Westside and 27 Zudio stores in 19 different cities.

Their fashion concepts have seen strong Like-For-Like (LFL) growth, with a focus on offering consistent value and a unique product range to customers. Emerging categories like beauty and personal care, innerwear, and footwear have also gained popularity and now contribute over 19% of the company’s standalone revenues.

Consolidated Results:

- Consolidated revenues, which don’t include Trent Hypermarket business revenues, reached Rs. 3,164 Crore, marking a 52% growth compared to the same quarter in the previous year.

- The PBT for the consolidated results was Rs. 314 Crore, reflecting a remarkable 129% increase.

4 Likes

Visited the zudio store as was always intriuged by the growth and price point . Have been a frequent to westside .

I should say that Zudio will give tough competition to road side shops / vendors .

The fabric quality and experience of try and buy with a price point starting from 199 makes it connect to the indian consumer

I would put it that way that westside is for middle class and zudio stands apart for lower middle & middle consumers .

Bullish about the growth prospects

Been a very long term holding

6 Likes

But what about the obscene PE ratio? Doesnt it make you uncomfortable?

Its been a very long term holding and i am confortable holding it for next 10-15 years. I believe the company has a great moat and its not easy to develop a brand which is scalable. When it comes to PE yes it is expensive but my view is if economy grows and disposable income grows the companies like Trent Titan and other consumer focussed company with aspirational brand will continue to grow at higher double digit and that shud help company to grow at double digit CAGR.

Having a relaistic expectation of return at this PE with holding period of 5 or more year may make it more comfortable to hold such companies

6 Likes

Curious to know about moat. Please elaborate as I see none among Intangibles [Patent or Brand], Switching Costs, Network Effect, and Low Cost Producer [due to location, key exclusive resource, or regulatory advantage].

I would argue and maybe unsuccessfully. Trent has a moat in the sense that 100% of their sales via owned sub-brands. Now these will not be household names. But they are integrated design to customer retailer a-la ZARA or H&M across both Westside and Zudio.

If we see their competitors i.e : Reliance Trends, SS, Lifestyle etc they play on shop in shop or buy and sell models. Maybe 30% of the products they sell are own brands. This impacts margins, ROCE and ability to change as per consumer demand. Look at the problems at SS when they try to push growth.

The play will be larger in future. There will be remote possibility of Tata Neu (entire e-retail) and Trent merging maybe in 10 years when Tata Neu turns breakeven or profitable. This scenario makes sense as it allows Tata Sons to increase shareholding percentage which is lower in Trent and bring entire retail play ex-titan into one company. Also provides exit to minority interests in Tata Neu.

Disclosure: Own it Via Family Account

4 Likes

Trent has a inhouse design and manufacturing and thats a huge advantage . I would suggest to visit westside / Max / zudio / pantaloons.

I have tried Max as thats nearest competition to Zudio but didnt like the quality ![]() . Have tried westside lower end tshirts quality is great ( persoanl view ).

. Have tried westside lower end tshirts quality is great ( persoanl view ).

The market size of Zudio and Max is huge if catered with right product + experience + value for money that itself i would call a Moat .

If you observe dmart or Titan they have harnessed on same thing ( experience + quality + right product )

Also westside + zudio has large format store which generally are hard to replicate as getting such huge space at certain location will eventually be not so easy.

I have tried experimenting visitng these stores and hence i find they do have a Moat at these times.

6 Likes

Folks (@hardik_shah1 @rahil_sayta ): Thanks for sharing your view generously. Your notes make it clear that the business offers good quality products at different price points [under different names] in an inviting shopping experience for all age groups. This is made possible due to inhouse E2E process. Extremely compelling setup for a customer.However, I am unable to make economic sense as an investor.

What part of the expenses will reduce with time to expand the OPM since every line item seems variable to my mind? Never ending need to keep stores fresh and the leased nature of the stores will ensure that both DA and interest expenses remain heavy and PAT remains lean. ROE/ROCE are yet to be respectable even though leverage[Tot. Assets/Tot. Equity] on the B/S is already 3x. Have you done any thought experiment on how unit economics will evolve with time?

Considering the prevailing valuation that too for an extended period of time, I am surely blind to the key aspects of the business. This is an attempt to remove my blindfolds with the help of folks like you who follow the business closely.

1 Like

Let me perfectly clear. The current share price is nuts. total nuts. Current price is definitely not a right entry point. At almost 8.5-9x 2024 revenue it does not make sense

I am riding the gravy train as far as i can.

Coming to the business.

Theoretically next few years will have higher spends and bring down FCF. But hopefully 4-5 years down the line, overall corporate and brand overheads are spread across larger number of stores, higher revenues resulting in better bottomlines. But this is not guaranteed.

DA and store refurbishments are always high with every retailer bar none worldwide. Its like obsolete machinery or replacement capex for any manufacturer.

On Finance:

A large portion of suppressed Net Income is due to IndAS regulations on how lease is treated. Even the debt on books is just majorly lease liability with just 450 crores of financial debt.

Would love your outlook on where i am going wrong on the business aspects of the company.

1 Like

Hardik- Thanks.

Over the years, I have realized that the market considers certain aspects that are not evident in the 1st look while valuing a business. However, such hidden insights are sensed by few who can think far ahead due to prior experiences. Hence, great businesses look overvalued on traditional units of measurements.

I was hoping to hear about insights that will disprove the overvaluation impression for Trent. As a customer, I like their offerings and am a regular visitor.

1 Like

Not an expert at numbers . Valuation wise there is no doubt its expensive and may remain so till growth keeps coming .

My understansing of business from a business perspective is with time per store economics may go up / sales per store .

Also most of retailers open up multiple store close the ones with lower economics and over a period of time you get good output.

Also lot of cross sell & spend per customer goes up over period may be economics of business may improve

Note : this is my understanding not an expert but a observation from a pure dhando perspective

1 Like

Thanks Surender, Great Conversation. Forcing me to relook and again delve deep into the business. I agree that market may keep companies at significant overvaluation for long times. But in this case difficult to sense or consider that it is fairly valued at this price point. I honestly do not have any idea or special insight that may answer your query.

Off Tangent:- The sports retail sector gives a fair example of what you mean by hidden insigts. 50% CAGR growth across companies as mentioned below. Did anyone anticipate and understand how to adjust this kind of growth. There are various aspects that are difficult to analyse as retail investors. This maybe the type of hidden insight or anticipation that market has that we don’t.

Sportswear brands ride the athleisure wave, double India biz in two years (business-standard.com)

1 Like

This article explains Trent’s high PE

4 Likes

Today Trent has jumped 20% in a single day. Reason being given is spectacular results. But results have been like this before also. Now after this result, PE will reach where?

2 Likes

Look at QoQ Pat Growth in this year. There is acceleration. But more than PAT, it is store openings of Zudio and like to like growth in STAR that is reflecting in the share price.

They have printed 26% same store growth in STAR which is extraodinary.

IS it overvalued. Absolutely, but it compared to peers, its the only growth retail play of size available. The only other option is Reliance(Rel Retail Sub) and Titan. All other plays are smaller, look at SS and Spencer, unable to grow.

3 Likes

It’s not just the size. It’s the quality and execution chops they have delivered.

It should keep on getting re-rated, on every result.

2 Likes

2 Likes

Trent Limited Financial Summary FY 2024

Standalone Financial Results:

- Revenue from Operations: INR 11,926.56 Crores (a significant increase from INR 7,715.19 Crores in FY 2023).

- Total Income: Increased to INR 12,277.49 Crores from INR 8,126.89 Crores in the previous year.

- Net Profit: INR 1,435.82 Crores (up from INR 554.57 Crores in FY 2023).

- Earnings Per Share (EPS): INR 40.39 (compared to INR 15.60 in FY 2023).

- Dividend: A proposed dividend of INR 3.20 per equity share.

Key Ratios:

- Debt to Equity Ratio: Decreased to 0.39 from 1.40.

- Net Profit Margin: Increased to 8.75% from 7.30%.

- Current Ratio: Improved slightly to 2.68 from 2.63.

Assets and Liabilities:

- Total Assets: INR 7,458.08 Crores.

- Total Liabilities: Reduced to INR 3,010.89 Crores from INR 5,241.18 Crores.

- Net Worth: Increased to INR 4,447.19 Crores from INR 3,079.94 Crores.

Consolidated Financial Results:

- Revenue from Operations: INR 12,375.11 Crores (previously INR 8,242.02 Crores).

- Net Profit: INR 1,477.46 Crores (compared to INR 393.63 Crores in FY 2023).

- Total Comprehensive Income: INR 1,490.29 Crores.

Key Ratios:

- Debt to Equity Ratio: Improved to 0.43 from 1.68.

- Net Profit Margin: Enhanced to 8.51% from 4.85%.

- Current Ratio: Stabilized at 2.75, slightly up from 2.71.

Key Financial Moves:

- Exceptional Gains: Significant exceptional gains were recorded due to reassessment of lease terms and related security deposits.

Auditor’s Report:

- Deloitte Haskins & Sells LLP provided unmodified opinions on both standalone and consolidated financial results, affirming the reliability of the financial statements presented.

This summary encapsulates Trent Limited’s robust growth and improved financial health in FY 2024, reflecting a strong performance trajectory beneficial for current and potential investors.

6 Likes

Q4 profits are entirely other income due to revaluation of leasing and rental costs. Its just Balance sheet change. No actual Cash profits. Result otherwise is good at topline and mediocre in the bottom line.

Disc: Invested in Family Portfolio at much lower levels. Now have to reevaluate seeing extreme bullishness in counter not backed by profits. Probably a sell and rebuy at lower levels.

3 Likes