Wow! This is the best which one could have researched and presented! Appreciate the way you look into such details.

Almost 61% CAGR is really good. If this continues with similar pace, very soon Tata Unistore stake would look very meaningful in their balance sheet. Please correct me if wrong.

I am just trying to think if this stake in Tata CliQ, along with the emergence of Super App is something meaningful for Trent/ big value unlocking in due course of time or not…

If we assume Trent has 10% ownership in Tata Cliq, they think fair value is 2000 Cr. and Trent’s ownership of Tata Cliq is currently worth 0.5% of its market cap.

One has to first ask what Tata thinks fair value is. From some news articles, Tata Cliq had a revenue of 226 Cr. in FY20, so Trent’s valuation was at 3.84x sales (Fair value of 86.98 Cr.), ignoring intangibles (Loss making, so can’t use any other metrics). If anyone finds information for FY21, we can compare that too, but one can ballpark this to roughly 520 Cr. in revenue if the FY21 valuation is still at 3.84 x sales.

If Trent’s holding value in Unistore is to be meaningful, Tata Cliq would have to increase revenue to over 3000 Cr, and that would result in a carried value of some 1200 Cr, or 3.24% of Trent’s market cap.

To be honest, I haven’t followed Unistore or Tata Cliq, but I wouldn’t be surprised if there was a multifold jump in revenue ever since the pandemic, and other e-commerce players are trading at much higher multiples, so one can say that Trent is being incredibly conservative with their estimates of fair value.

Although not directly comparable, but one of listed consumer tech company Zomato had FY21 revenue of approx. 1600 cr. With a mcap of 1Lakh 4K Cr, it is valued at approx 65X its FY21 revenue.

From what I read about Tata CliQ, they have been following a more sustainable towards profitability business model unlike other marketplaces.

Cannot agree more that with a mere 3.84X sales, the valuation of an upcoming market place from the house of Tatas, with a synergy of Tata ecosystem & upcoming SuperAp, is extremely conservative.

Even Indiamart in B2B is a 25000 Cr mcap company with revenues of approx 660 cr, it is a 37X revenue!

Trent is expanding its store aggressively, any views on it? Will it lead to more expenses to run new stores? Pls share your view for short term and long term. Thanks.

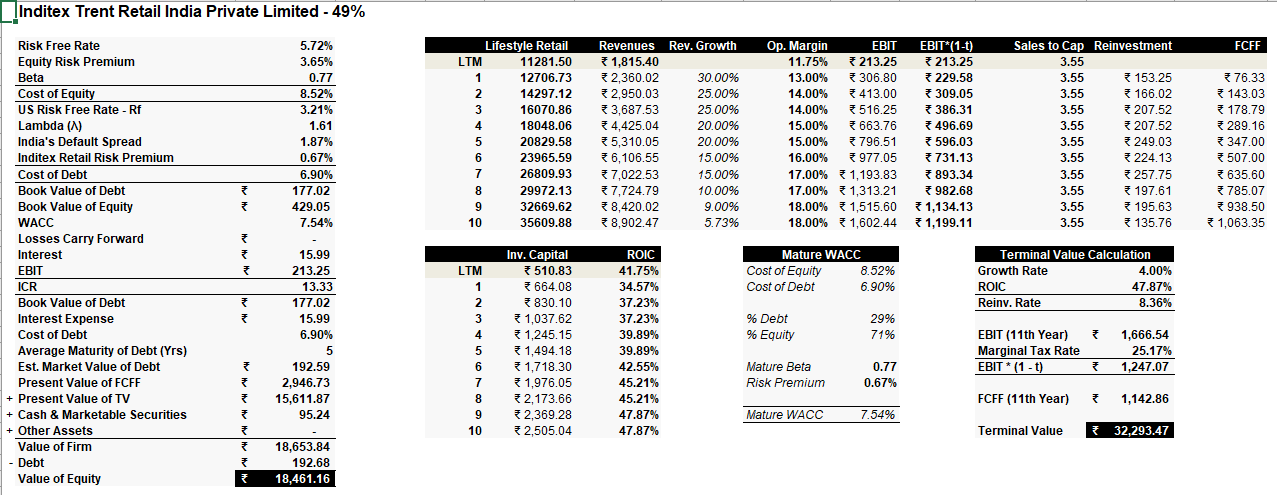

I did an Intrinsic Valuation of Inditex Trent Retail India Private Limited - an Associate of Trent Ltd to run Zara stores in India. They have 49% stake in the associate. Surprisingly, I found out that Inditex (Zara) generates about 35% of value in Trent Ltd, in other words, Zara is a big reason why people are high on Trent Ltd. Is it true? Right now, in terms of Trent Ltd.'s own business, they are earning less than their cost of capital.

Disclosure: Not Invested and not planning to invest either.

Recently I was amazed by the crowd inside a Zudio store with young people flocking and billing counters completely clogged. Guess they need faster billing process/counters etc. to match the demand…in short, Zudio was looking like the Dmart of fashion…no doubt its 1/4th of Westside in short span.

The beauty of a resilient group, management is such that what they built in 25+ years, they replicate in next 5+…

Disc: Invested & Biased. No buy/sell recommendation

Even, management has mentioned that they have not yet find the best ideal / suitable model for Zudio (offering low prices while still making profit) and they still are experimenting.

Tata has also launched their own saree store. Through it is still in trial phase and has very limited store count, it seems they are trying every category (which is a good thing IMO)

If zudio revenue mix will be more in future then margin may decline as westside have more margin than zudio but management is more aggresive towards zudio hence volume will be more than westside which may lead to margin contraction. We can assume good topline growth but less bottomline growth.

Thanks for the attached article. It really boosts my confidence in the business. I have investment and expects it give good return in the long term 3-4 years. Thanks. Samir Ghosh

Its a good read and a simple yet effective way to look at high PE companies…

Big IF as per my personal experience is the management. Here it is the House of Tatas while in many other retail, ecommerce firms it was just hype.

I had been eyeing Trent ever since 2012 onwards all the way around 100…didnt pick it up because of high valuations as I was a novice. Finally didnt miss it at 500 and was able to top up at 1000…still feel the bucket was just half full…

Disc: Invested hence highly biased. Not a buy/sell recommendation. Views only for academic purposes and I can be wrong in all my assessments.

Valuation of trent can be done by considering price/sales instead of PE ratio. If we check the history, then it is clear that it is trading near 5 years mean P/S ratio and its peak P/S ration was around 14-15.