A lot of has happened since last post on this thread. Stock has corrected by ~ 40% from Feb highs.

We need to assess impact of Corona on Business models of Westside, Zudio, Star and Zara

Fixed Costs in lockdown period

- Most stores would be Franchisee owned, hence contractually the fixed costs of rent, electricity have to be paid by Franchisee. MOSL report after Q2 FY20 also states that for Zudio the rent and electricity are to be paid by Franchisee.

- Fixed cost for Trent would be

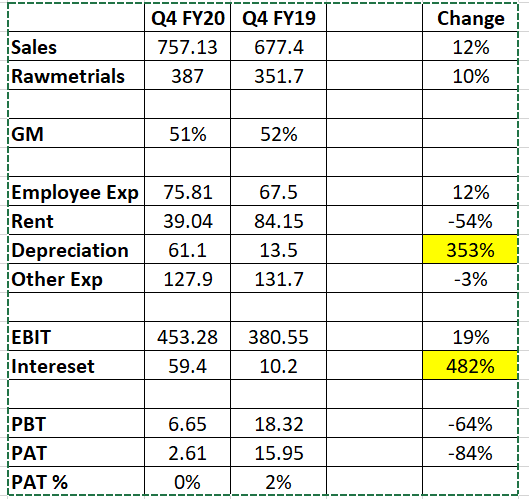

Employee cost - FY20 9M: Rs 269 crores

Rent and Interest on cash basis (Pre Ind AS 116) in FY19 was: Rs ~ 350 crores

Other fixed cost taken conservatively would mean annual fixed cost of Rs 750-800 crores.i.e. Rs 65-80 crores of fixed cost per month on cash basis.

Franchisee subvention in lockdown period

Depends on industry practice as there is no precedent. Logically, should not be there but possibility exists. There is a higher chance that the Franchisee would reneg the lease rentals with the Landlord.

Time taken to resume to 100% operations

This is a very tricky aspect. 2 Days back, Bill Gates said in an interview to CNBC that vaccine for coronavirus will take around 18 months plus after that to produce that for 7 billion people and vaccinate them is going to take even more time. One has to take a judgement call here so as to whether only lockdown will be enough to get rid of coronavirus in India and when. Most stores are located in Maharashtra which is the hardest hit state and other metros which one would assume will be the last to come out of lockdowns.

After lifting of lockdown also people would be fearful and brick and mortar stores would be adversely affected atleast till the virus fear has been completely eradicated.

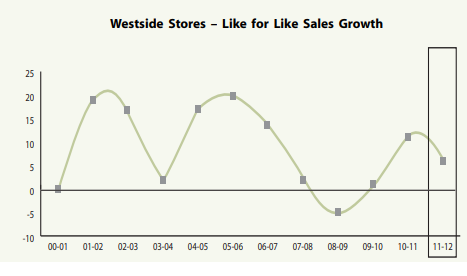

Even after the virus fear is over, IMO it will take time for the stores to reach current SSG growth rates

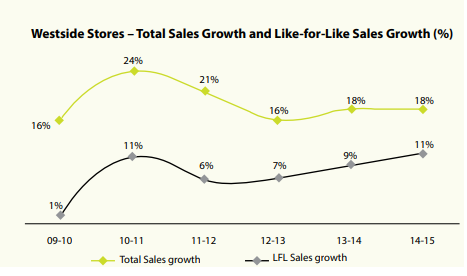

For eg,In past downturns, SSG has fallen in line with reduction in GDP growth rates in 2009 and 2012 and recovery has been gradual.

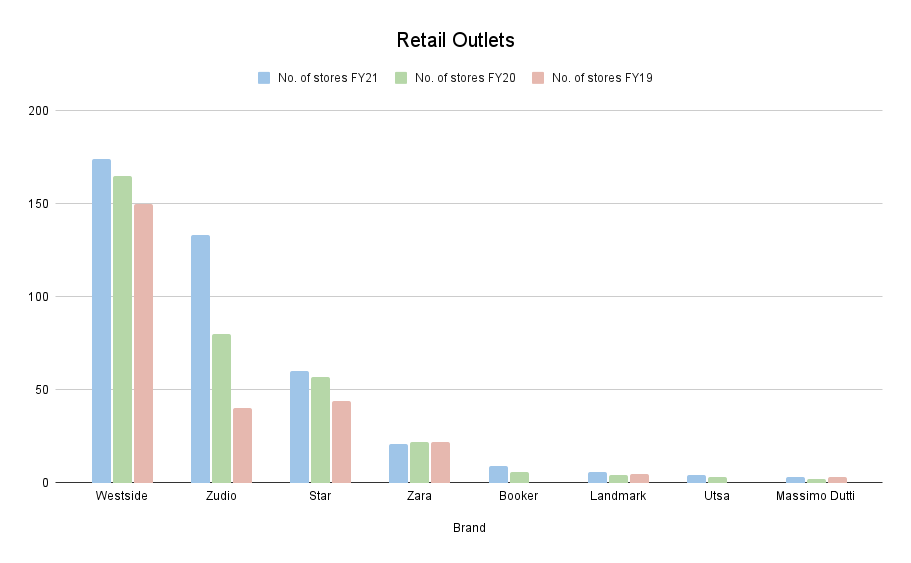

Needless to say, management would not be inclined to add stores in the near term, delaying the expansion.

Growth rates factored into the lofty valuations earlier will undergo large changes.

All in all, extreme headwinds for the apparel retail industry as a whole esp for brick and mortar. Although Trent stock has been more resilient compared to more than 50% drawdowns seen by FRL, FLFL, ABFRL and Shoppers Stop.