Transpek-silox:

Hope this helps ![]()

1 Like

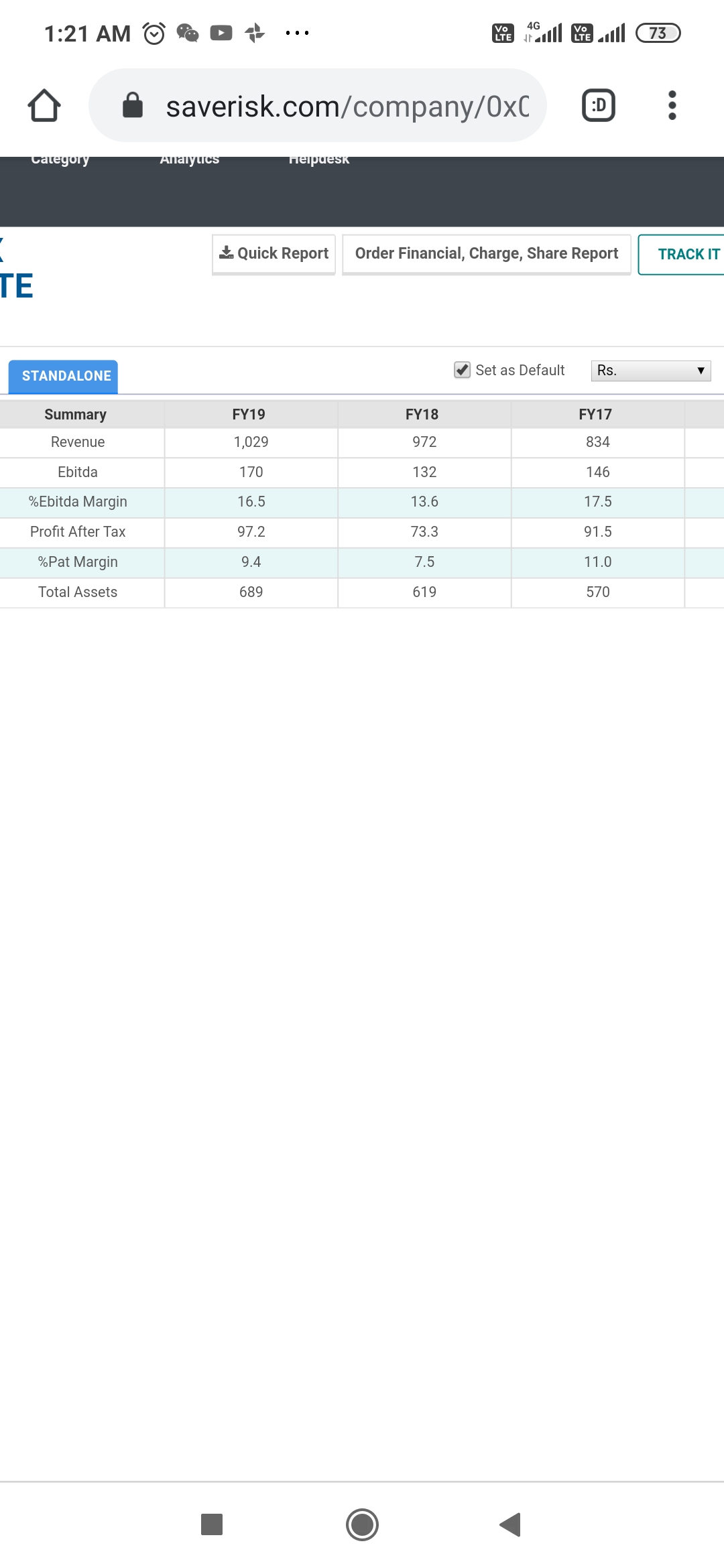

Above is pnl statement for Transpek Silox industry private limited

1 Like

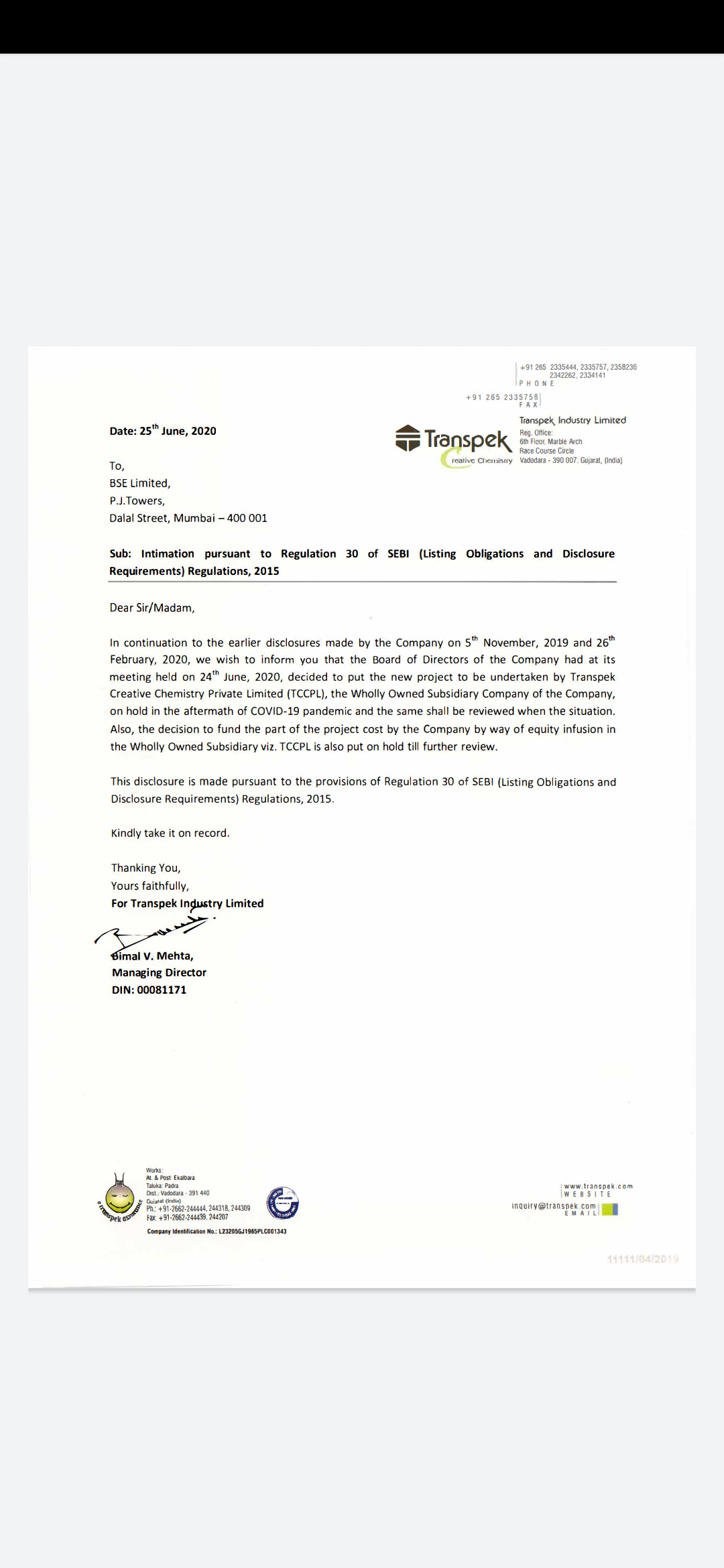

Operations resumed partially.

TranspekReOpen.pdf (1.1 MB)

Some export hv happened during lockdown too. I think co will emerge stronger

5 Likes

Hi,

Try to look at larger picture. Don’t miss the forest for the trees.

There are so many promoters who siphon off money from the company and no one even knows.

To me here the promoters are honest in disclosing rather than hiding.

1cr is a petty amount to be bothered off, if it were 10cr sure I would think it differently.

The promoters have created value in the company and after all that’s what matters for minority shareholders.

I am from Vadodara and I have heard good things about the promoters. I don’t see this as poor governance.

15 Likes

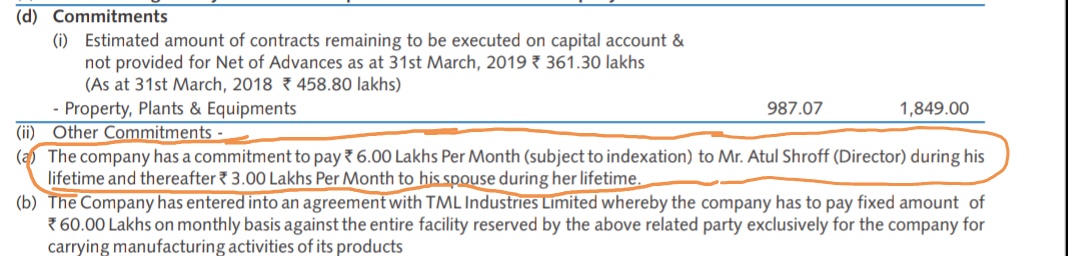

I think this payment to Mr Atul Shroff for lifetime and his spouse post his demise (if she survives him) is a sort of pension for a person who took the company to where it is today.

In last year’s AGM, they mentioned that the contract they got from Dupont was because of efforts started many years ago and is not a flash in the pan kind of development.

The reputation of the Shroffs is impeccable and I would prefer someone to take a higher salary or officially take some kind of remuneration rather than siphon off money. Here in this case we atleast know how much is being paid whereas in case where money is siphoned off, we have no idea about it.

In most small cap companies, we would find something or the other to worry about if we dig too deep. It is up to us to figure out what is to be ignored and what is to be taken seriously.

The problem with Transpek seems to be a string of bad events which stops the company going fast forward. As soon as we are assured of positive developments, bad luck strikes them.

First it was the accident which queered the pitch and affected production for few weeks. After that there was concern about capacity of the company and that was addressed by capex announcement. Post that Covid struck and it seems strong growth and capex coming on stream is now pushed back by few more months.

43 Likes

Hi Folks,

I’m attempting to arrive at a valuation for Transpek. While I do understand that each one’s method can differ and hence valuations may also differ, I would appreciate it if anyone can share your valuation and/or point out to any gross errors here.

- Revenue from operations 2018-19 = 595 crore

- Given all that we know from the above discussions and information in the annual reports of the last few years a conservative estimate of growth is assumed @12% per year.

Note: As of Dec 31, 2019 there has been a drop in revenue of 5% relative to Dec 31, 2018. - 6 years out the revenue should touch 1200 crore. Considering an average OPM of 15% would result in an earnings of 180 crore.

- Using an earnings multiple of 15 would result in a market cap of 2700 crore.

So buying at today’s price of Rs. 1700 per share we’re expecting roughly, a 3x return in 6 years provided the story plays out as expected.

The question here would be how realistic of an expectation is this? Or how sure can we be of this scenario.

Disclosure: No ownership in the company discussed above.

Best regards,

Seema

3 Likes

I don’t think anyone can get valuations correct. It is extremely difficult.

There can be 2 scenarios playing out in the next 3 years:

Scenario 1 can be all good

At the current juncture transpek is more or less doing sales of around 2X the gross block. They are adding capacity in Vizag with a capex of 120cr.

Assuming this new capacity comes online in 3 years and starts to do sales of roughly 300cr (2.5X investment), and also assuming no more growth from current plants, one can come to sales of 570+300= 870cr. Lets call it 850cr.

Now transpek already has expanded its operating margins to 20 plus percent. It can expand further in a good scenario and go to 25 percent (highly unlikely).

So 3 years down the line in good scenario transpek has sales of 850cr and operating margins of 25%. That can translate to PAT of 125cr with 25% tax (other being depreciation and interest cost).

Roughly 15 percent CAGR on PAT.

Markets can value this PAT at 20 times, 25 times, 30 times or 35 times depending on the story at that time. Who knows. But lets say 15 times.

So we come to a Market cap of 1900cr and share price of Rs. 3300 (at 30 times the share price would be Rs 6600, and that is possible too)

Now in Scenario 2 all is bad

No growth and 1 times asset turn on the new capacity of 120cr.

So in that case we come to a Sales of 570+120= 690cr.

If we think all bad is going to happen, lets also assume operating margins to come down to 15%.

In that case the operating profit would be 103cr and PAT can be 50cr (25 percent tax rate, higher depreciation)

Markets also don’t like falling margins and can derate the PE multiples so it can go to a PE of 10 times or Price to sales of 1.

So in this scenario the Market cap can fall between 500cr to 700cr roughly (share price of 900 to 1200)

At this point I don’t know which scenario is going to play out.

One has to take small position and see which way things are going and built conviction as every quarter goes by.

There is a 40 percent downside and 500 percent upside. Beyond 200 percent is all luck and nothing to do we the smartness of the investor.

I have personally taken small position 2 percent of PF and will see how things play out.

29 Likes

@jshah17umd Thank you so much for your views. Definitely helpful.

1 Like

Video featuring Transpek Industry on CNBC Bajar from a couple of years ago.

Note:it is in Gujarati & gives a good overview of the companies business,facilities and people involved.

4 Likes

Results

EPS at 130+ -Annual

Borrowing reduced

Q4 OPM improved

Inventory built up in Q4

3 Likes

Does anyone have an idea of what the company spent Rs.120 crore on in FY18 and what did it contribute to capacity?

@hitesh2710 mentioned that the Company is running on ~85% capacity so is this because the Rs.120cr was just maintenance Capex or this Capex is still in progress and yet to be commissioned?

I see the returns on this Capex have been reasonably productive with higher sales and ROE ROCE at 20-25% but good to know if the Company can push higher volumes without Capex for the next 2-3 yrs.

@hitesh2710 Hitesh bhai, as you said earlier something or the other going wrong for the company and growth isn’t materialising. Given the conservative management, should we not read too much into this? or the company might see headwinds on contract (like Aarti industries had) and hence they have kept this project on hold for now.

appreciate your thoughts.

Halt of cap-ex plan. Surprising !!

Given that coming is running at or more than 85% capacity and there is good growth across players in the sector given China issue, it is strange that company has postponed the cap-ex.

I raises doubt on demand for the company in one of the best periods of the sector.

Do suggest if I am reading it wrongly.

My understanding…

Weaknesses

(1) High dependency on single client

(2) That too in two chemicals

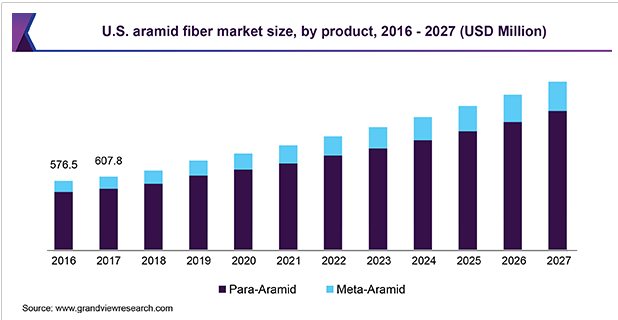

(3) End products are meta & para aramid in which US customers sales are stagnant since few years

(4) US customer procures these two chemicals from 4-5 or even more companies. (Transpek has take or pay agreement - how it structured - I don’t know much)

(5) Softness in product prices due to crude related issue (which are temporary I hope)

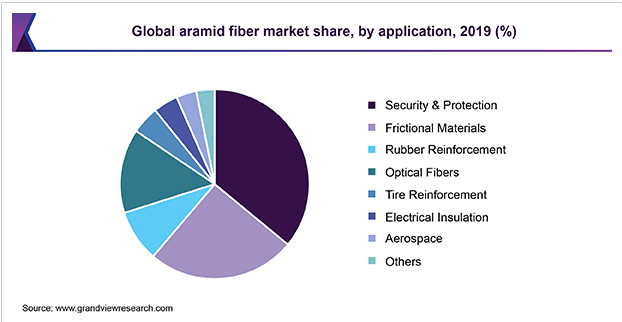

Strength

(1) End use of aramid well diversified

(2) Aramid market itself is growing (But kevlar and nomex stagnant, which might show some growth going forward)

(3) One more such long term order can change fortune (as hiteshbhai called it Dark horse)

15 Likes

Thanks to everyone who collaborated to the thread. Have been reading to try and understand the business.

Sir, thanks for the insights. However, I am a bit confused as to how did you deduce the above?

(If you’re referring to the report attached below; Page 36, Annexure 7, why did you consider only the first process and not the subsequent ones such as Ether Amine, Friedel Crafts Chemicals, SACL etc?)

http://environmentclearance.nic.in/writereaddata/Online/TOR/10_Mar_2017_103022463JSIRTKAPAnnexure-AdditionalAttachment.pdf

Sir, request you to explain what exactly is meant by the term ‘consolidate’ in this context

Also, since not much transparency is there in Transpek’s business, as investors we are ‘hoping’ for some triggers like more long-term contracts, ability to move downstream which will help to add more value to the products (since most of the company’s products are intermediates) and also increase margins, right?

2 Likes

In broader view, one of most imp fact, IMO would also consider sector tail winds which is making entire sector getting re-rated, which somehow isn’t reflecting in Transpeck, partly due to one or other company specific event( mostly out if company control)over last 3-4 Qtrs, latest being expansion plan on hold.

We can see many stocks getting into FMCG valuations zone( PI Ind) and market just seem to be in tango with pharma and chemical…party seems to be just getting started.

With lots of demand chasing limited supply, Transpeck should do well too, need one good Qtrly performance and positive outlook by mgmt…

Lots of data points on company fundamentals thread above,

Invested, Counting on upcoming Qtrly results

4 Likes

From the New feature on Screener.in - Shareholders details can be easily accessed. One name that caught the eye for Transpek was that UPL Limited holds 0.74% of Share Capital and is classified as Promoters.

UPL Limited has a very respectable track record and history of creating value to all stakeholders for last many years. Are the Shroffs of Transpek in any way related to Shroffs of UPL ? Could not figure out any other way by which UPL could be classified under promoter category.

2 Likes