Inventory build is due to COVID issue & has been there for most of the cos…

From the screener.in i could UPL holds below 3-companies but it seems all those seems not traded now,any other UPL holding or past record which you can share ?

Jun 2016 Sep 2016 Dec 2016 Mar 2017 Jun 2017 Sep 2017 Dec 2017 Mar 2018 Jun 2018 Sep 2018 Dec 2018 Mar 2019 Jun 2019 Sep 2019 Dec 2019 Mar 2020

Advanta 57.38

Chemiesynth(Vapi 30.00 30.00 30.00 30.00 30.00 30.00 30.00

Nivi Trading 4.01 4.01 4.01 4.01 4.01 4.01 4.01 4.01 4.01 4.01 4.01 4.01 4.01 4.01 4.01

Yes. They are cousins.

2 Likes

Change in inventory is close to INR 20 crores while the net profit for the period is only 24 crores. This along with the recent halt in CAPEX plans points to some negative news which we may not know at this point in time. Company is available at cheap valuation of 7x at normalized PE but the problem is lack of growth drivers for the future. Waiting for AR of 2020 to get more clarity.

Disclosure: Invested 3% of PF

3 Likes

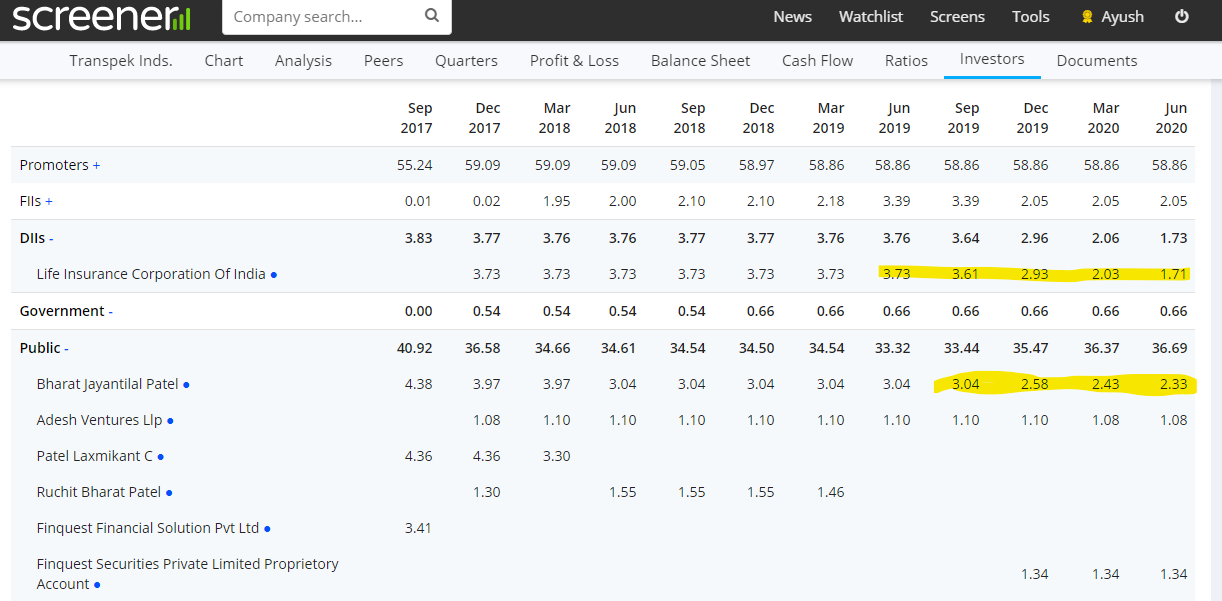

It seems LIC selling shares…there holding down to 1% now in this quater share holding pattern. Hence not able to move i guess. Unable to understand hold on capex…may be cleared in this year AR

1 Like

Yes, LIC and one of the other key shareholder seems to be selling

Selling of LIC may not hold much relevance as this must be their very old holding and selling might not be for specific reason. Unfortunately they still hold about 1.71% and this may remain an overahang till absorbed by the market.

7 Likes

Transpek has Sales CAGR more than 15% over any period and a big rise in 2019 year.

ROCE is averaging around 11% only. When we double click, we find that it operates with low margins. The capital turnover ratio is not high and that causes the ROCE to be below the teens but it has improved to be around 14% in 2019. ROCE prevents this from being a coffee can stock

SSGR is 15% and the company has a debt to equity of around 0.46. A prudent banker would give a loan of 278 Crore to Transpek which is around 33% of its market cap, and the company has around 18% of its market cap as cash & investments. So this is a fundamentally strong stock and the owners could look to take it private if they wanted to by taking more debt on the books

Accounting checks came out clean. Only concern was the variation in receivables days

Company has a earnings yield of 8%, which is a high margin of safety. It is trading below its average P/E of 16.8 and 14.5 for 3 and 5 years respectively. Company has generated 3 INR of value for every 1 INR of retained earnings

Company market cap is increasing because of earnings and not P/E expansion as we see over 3 and 5 years

I see that Ayush has invested in the stock. Another reason to buy

Good stock to invest

Disc: Hold 100 shares at 1490

13 Likes

Bharat J Patel is one of the directors of Finquest Securities. So I guess its more of an internal transfer.

1 Like

But if you see Finquest Securities shareholding its not increased…so doesnt seem internal transfer

yes current overhang seem to be because of that only…1.7 ~ 95k shares…hope it ends fast and new journey begins…also AGM in sept can clarify there growth plans

Consolidated Financial Results for the first quarter ended 30th June, 2020 on Monday, 10th August, 2020

There is 500M capex reduction in dupont though not all reduction might impact transpek but dupont also idled some of the prodcution facilities which transpek alone was contributing too .Would be interesting to see the Q1 result on the impact .

7 Likes

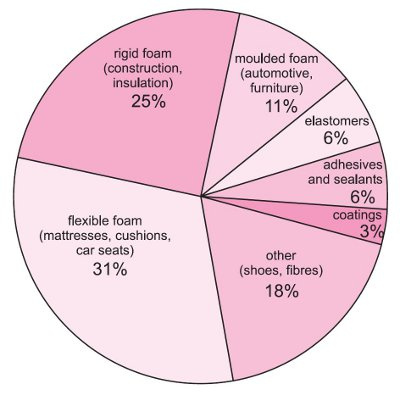

While i was researching in tyre segment found the interesting part on airless tyre which maybe the future for tyre sector :

I have posted my article & research papers here :

How does Transpek benefit from this? Airless tyre uses Polymer to make these tyres : in case of Transpek they are mainly into leading manufacturers and exporters of a range of industries such as - Textiles, Pharmaceuticals, Agrochemicals, Polymers, etc.

Will the opportunity play now? No because the airless tyre are a concept and been implemented by Michelin and are not in production or a hot cake. It will take time for market absorption before that polymer distributors can play a major role in these things - we need to keep our eyes wide open for such great opportunity who can be a next great player in tyre industry (example of a veteran MRF)

Video of Airless Tyres by Michelin

Main ingredient : polyurethane (Foam)

Polyurethane uses : Artificial Leather, seats, tyres, shoes, electrical equipment

4 Likes

Wow! 09-10 AR has same ~3.73%

The buyerside support is coming from Safir Anand (and other HNI’s) who could be holding more than 1 percent as per his tweets.

3 Likes

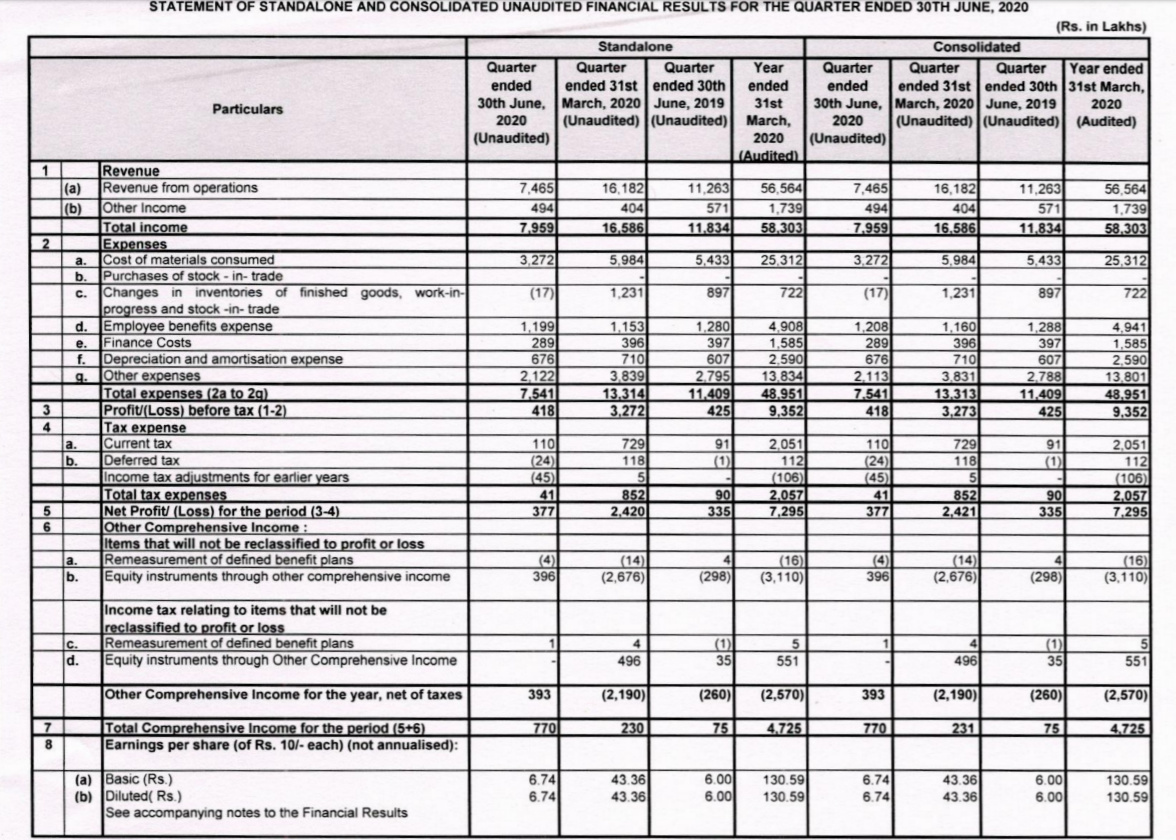

Results are out, while sales are down 33% from 118.34 Crs to 78 Crs profit is up 12% from 3.35 Crs to 3.77 crs.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=fbdbb3bf-19d3-4b4e-be34-d65af843464d

It appears that the PAT last year was particularly low and this is not a trend for June qtr.

Any views comments on whether this is a good result or bad ?

Q1 19 had 40 days of production ( more info in thread above) due to accident issue.

Q1 20 had lockdown issues and plant probability operated at lower capacity initially and roughly overall 60 days of production.

In light of lower base YoY, results doesn’t look good though margins were maintained/improved.

Capex is still on hold, best case under constraints is revenue rate of last year or thereabouts going forward.

Valuation are reasonable but growth is missing for one or another reasons. Lot of volume action in counter over last few weeks.

Given sector tailwinds, some growth delivery may trigger upside, wait got pushed by another Qtr.

4 Likes

Disruptions were there in FY 19 and 20…the results are more or less as per expectations…will wait for sep results

Market & stock performance all across is currently divided by - Stocks impacted/Not impacted by Covid19

Till any clarity comes from management/annual report/AGM its safe to assume Transpek is the impacted one based on 3 factors highlighted below:

- Capex Scrapped

- Kevlar/Nomex not as critical to Dupont as Tyvek where they have increased production, and decreased elsewhere

- Revenues deeply impacted

Last point needs to be tracked in next 2 qtrs to understand if the impact is due to plant shut down or lower demand from key client.

Discl - Tracking, No holdings

5 Likes