This is my first jab at presenting an analysis of a company. Most of the data points are gathered from the internet and the company’s 2014-15 AR. I am awaiting the 2015-16 AR. I have ensured that there is no existing thread for Transpek in this forum. I am sure that many data points will be missing and hence the intent of the post is not only to garner views from the community but also drive learning for myself.

Transpek Industry Ltd

Market Cap.: ₹ 272.49 Cr.

Current Price: ₹ 464.20

Book Value: ₹ 154.58

Stock P/E: 12.80

Dividend Yield: 1.61%

Promoter Holding: 47.78%

Debt/Equity: 0.7

EPS for 2015-16: 36.24

Transpek Industry Limited was set up in 1965 initially for manufacturing Transparent Acrylic Sheets. Since then the Company has grown to become one of the leading manufacturers and exporters of a range of chemicals servicing the requirements of customers from a diverse range of industries - Textiles, Pharmaceuticals, Agrochemicals, Polymers, etc. Since inception, Transpek has evolved as a First Time Manufacturer of several products in India and also pioneered the development of the market for the same.

Over a decade of presence in the international market, Transpek has earned for itself a name for being a quality supplier. With its expertise in handling Chlorine and Sulphur, Transpek has indigenously developed process for chlorinated chemicals like Thionyl Chloride and Chloro Acetyl Chloride. The company is pioneer into Thionyl Chloride Chemistry and currently largest producer of Thionyl Chloride & Acid Chlorides in Asia, outside Europe.

The company has high focus on environmental protection and has the necessary ISO 14001:2004 certification.

The company product line contains multiple organic as well as inorganic products. As per the website there is a good pipeline of products under development too. This shows the companies focus on innovation. The strength of Transpek’s R & D is evident from the fact that the manufacturing technology for all of its existing products was developed in-house.

INDUSTRY STRUCTURE AND DEVELOPMENTS

Your Company’s product portfolio comprises of various products which are used in a very broad range of applications. Through Chlorination, the Company manufactures many Acid Chlorides and Alkyl Chlorides.These products have global market & many big multinational chemical companies use Acid Chlorides & Alkyl Chlorides in very large quantity.The Industry segment in which your Company operates is vast & hence there is good potential for growth of business.The products find application in agro-chemicals, polymers and plastics, pharmaceuticals, performance materials, organic peroxides, personal care and flavours and fragrances.

POLYMERS AND SPECIALITY PLASTICS AND PERFORMANCE MATERIALS

The market for Polymer and Specialty Plastics is continuously growing due to discovery of new applications of these materials. Your Company makes basic but key products for manufacturing Polymers & Specialty Plastics. Many world leaders in high strength polymer products source their critical base products from your Company.

PHARMA PRODUCTS

Due to extremely high quality of the Acid Chlorides of your Company, many Pharmaceutical companies prefer to buy key raw materials from the Company. Many Indian Pharmaceutical giants are customers of your Company.In the coming period, this segment is expected to register significant growth for your Company.

AGROCHEMICALS & DYESTUFF

The demand for Company’s products in Agrochemicals segment is expected to be stable during the year. However, your Company has been making efforts to increase the customer base & the products in this segment. Your Company has started manufacturing a new product which is supplied to a very reputed Multi-national Company.We do not expect any growth in the dye-stuff industries. Therefore, our Thionyl Chloride supply to this market is expected to be the same as compared to previous years.

FLAVOURS AND FRAGRANCES

Your Company has been gradually introducing new products in this segment. We expect this segment to grow slowly but steadily.

Transpek also has an investment in equity shares of Excel Industries Limited the market value of which is approximately 450 lacs.

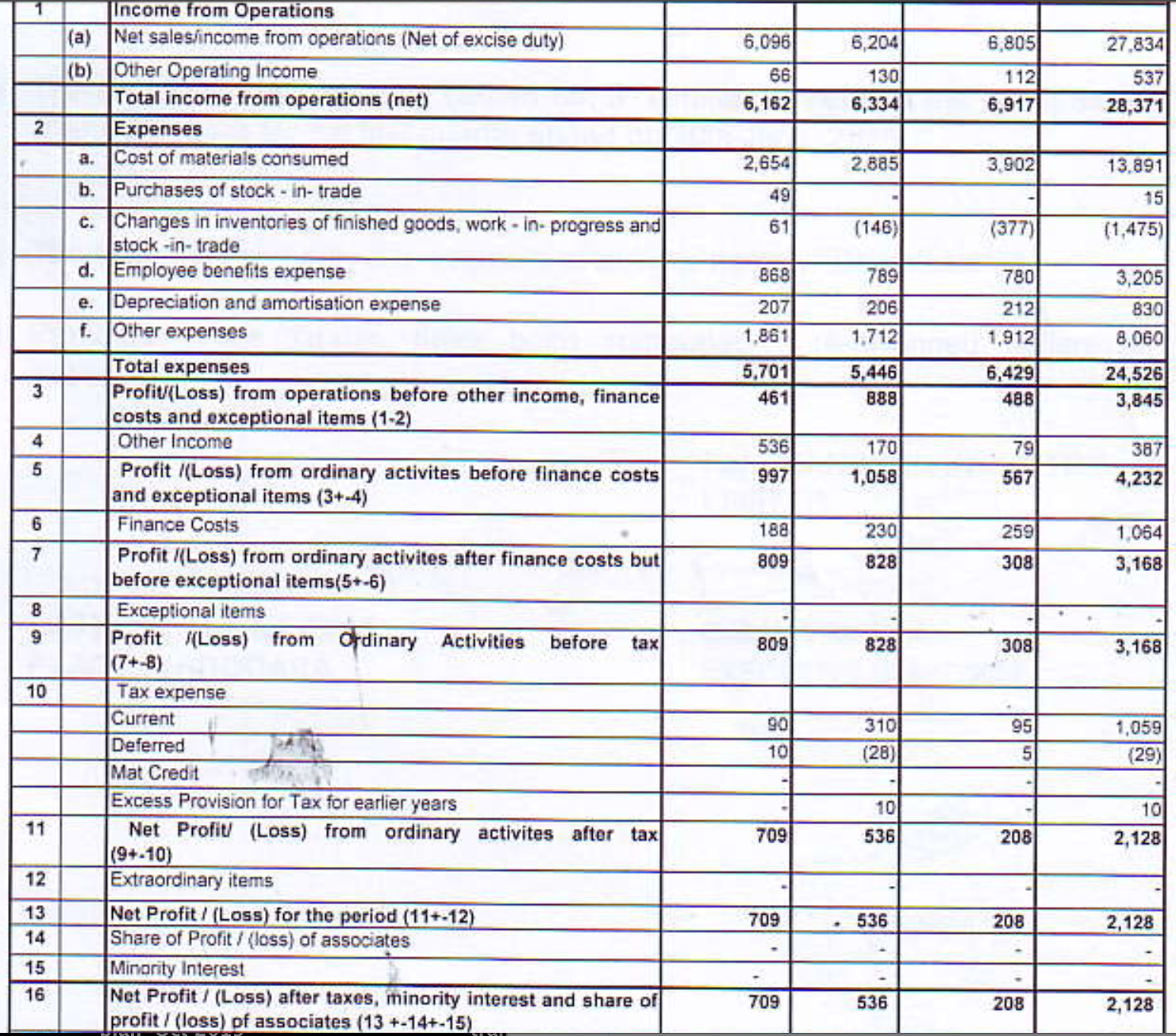

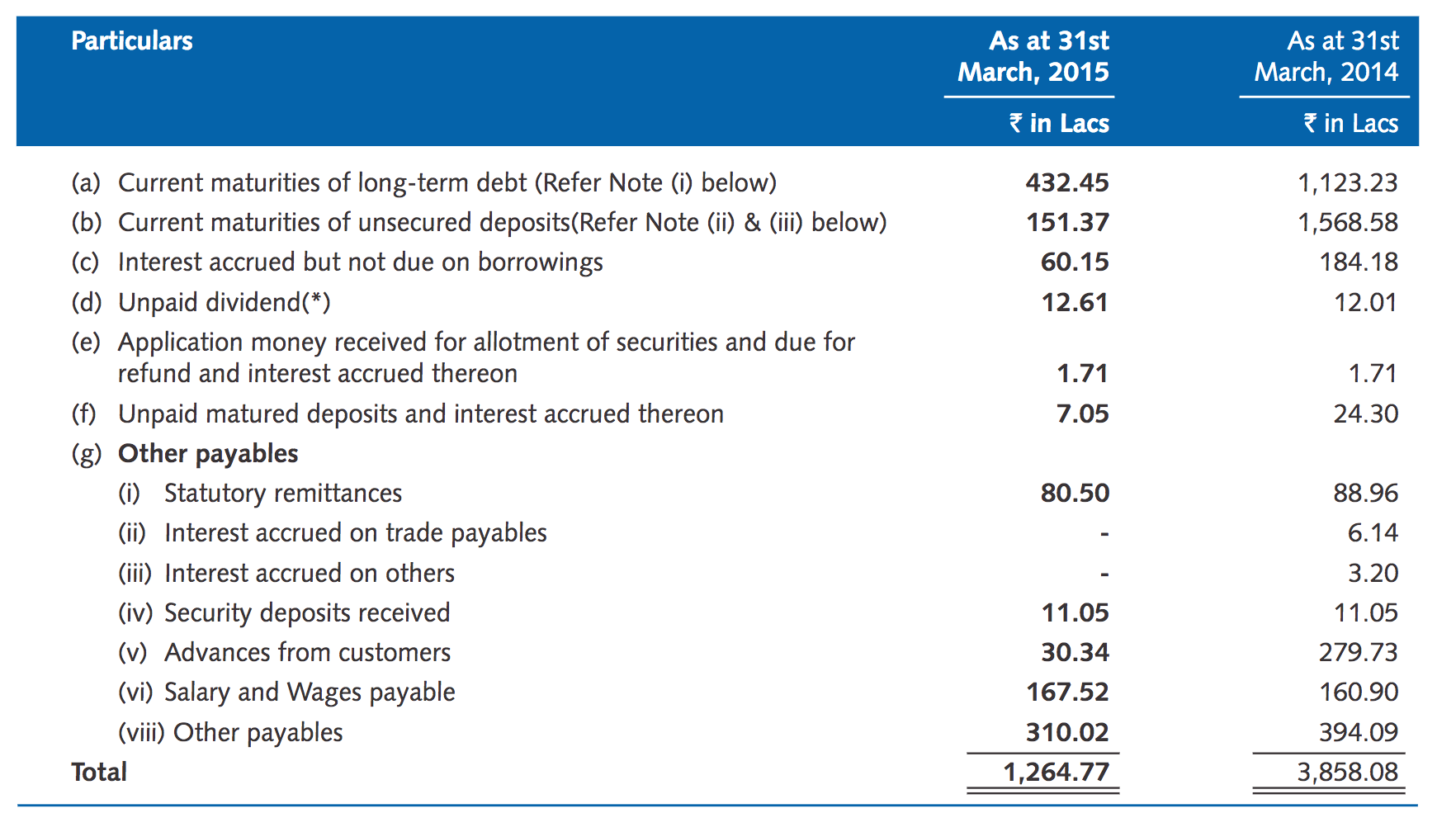

The company has reduced debt last year. Here is a snapshot.

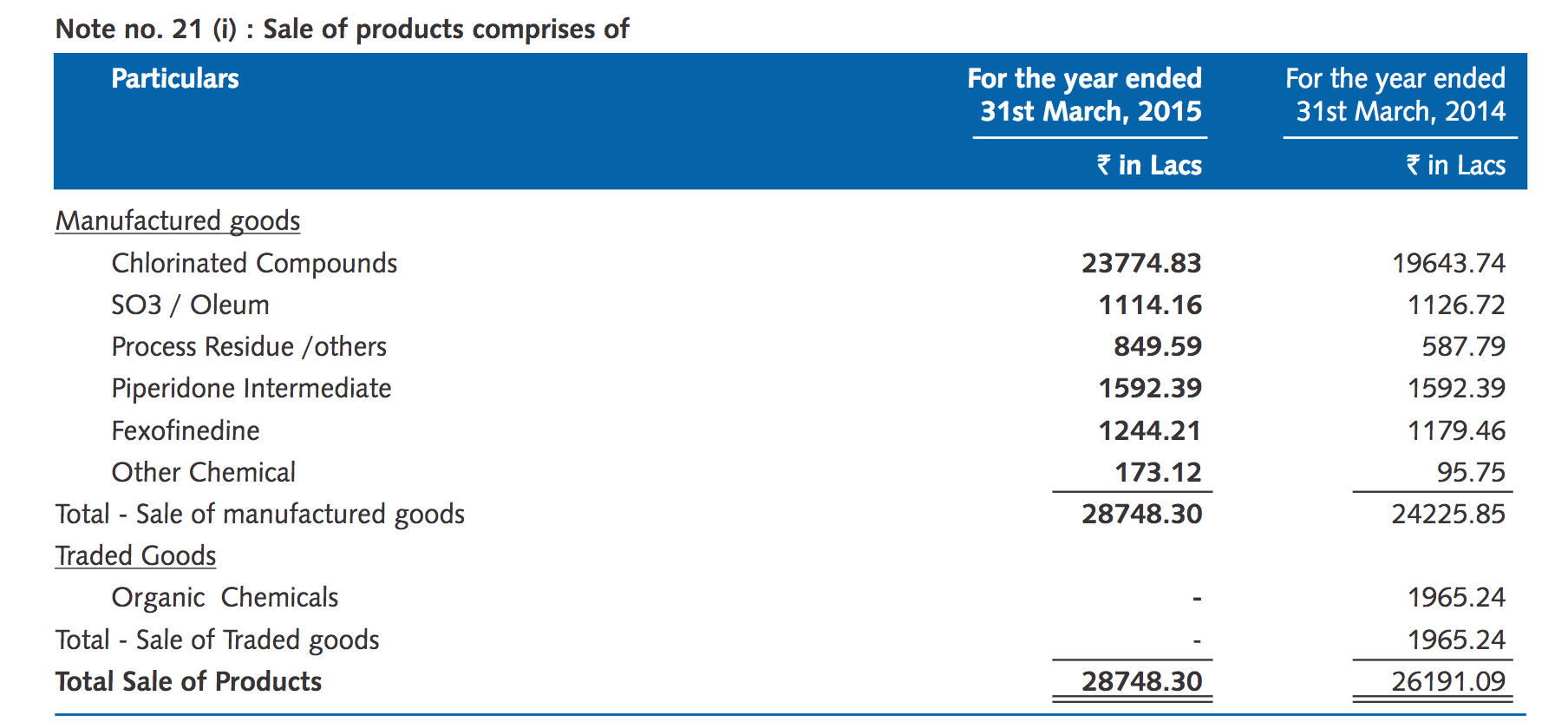

Here is the bifurcation of the sales as per products for last year

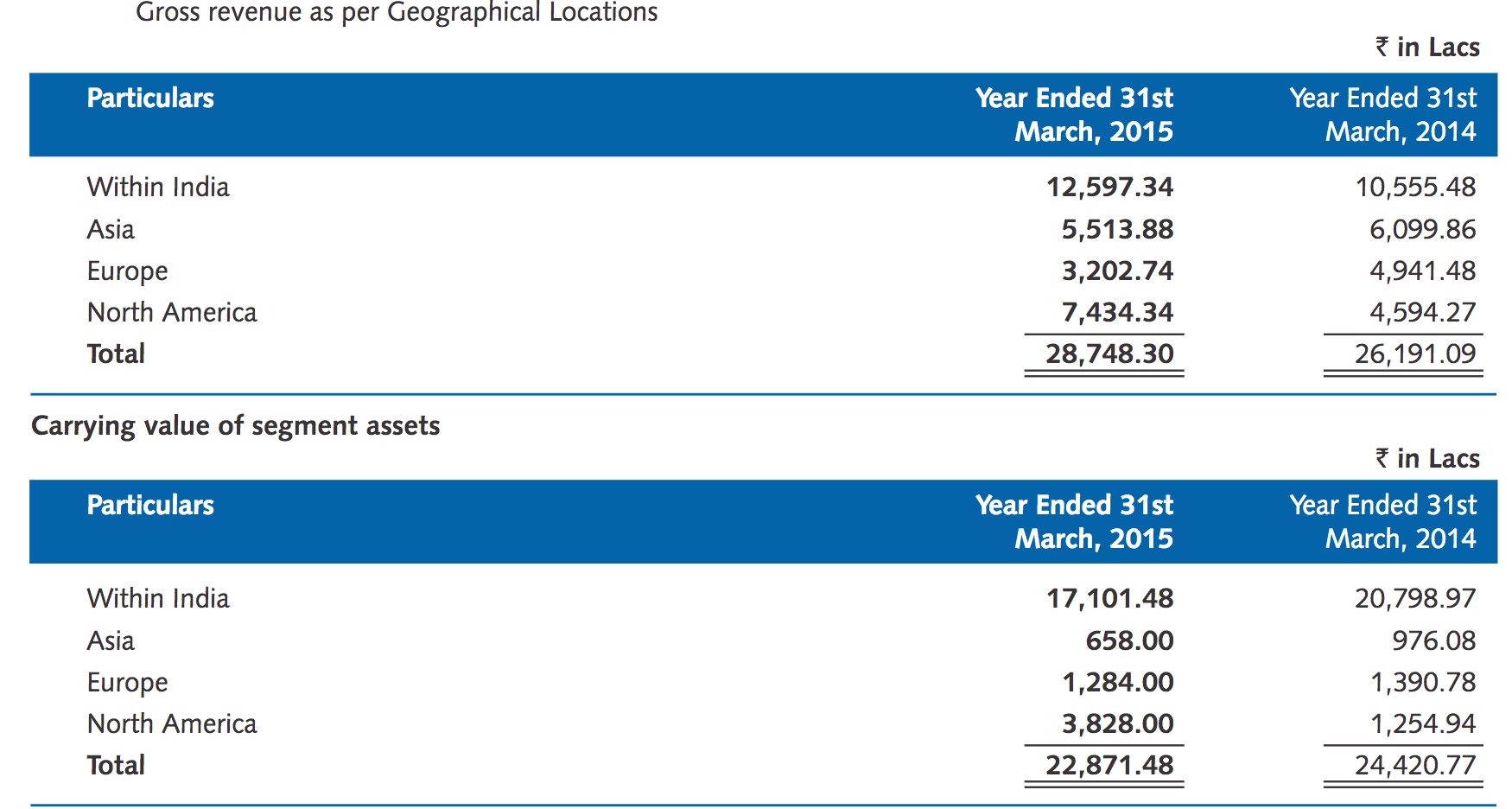

Here is the bifurcation of the sales as per geography for last year.

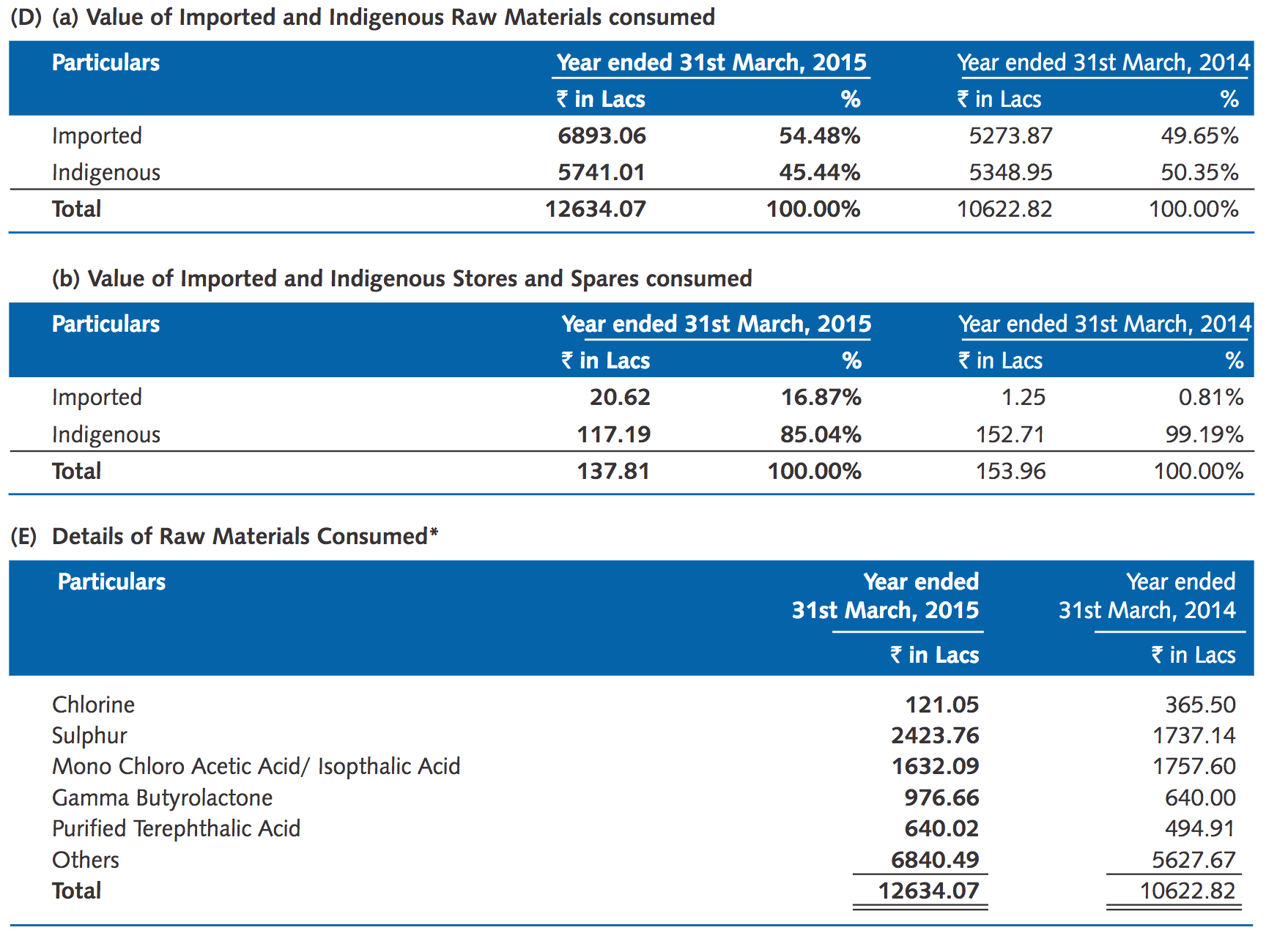

Here is a list of raw materials consumed during last year

Opportunities

Chinese Anti dumping duty will have positive effect on Indian Chemical companies

Management is conservative and has good focus on innovation.

Stock is trading at a PE lesser than peers.

Threats

I am not sure how much top line addition will result from the products which are under pipeline.

The companies growth philosophy is simple. Increase customers for existing and new products. Need to understand their strategy wrt the same.

Disclosure: Invested (10%)

Request senior members to provide their views and guidance.