Business Overview (private market database platform) -

Founded in 2013, Tracxn Technologies is data platform for private companies. It currently provides coverage for 20 lakh company profiles (vs ~10 lakh as on FY20).

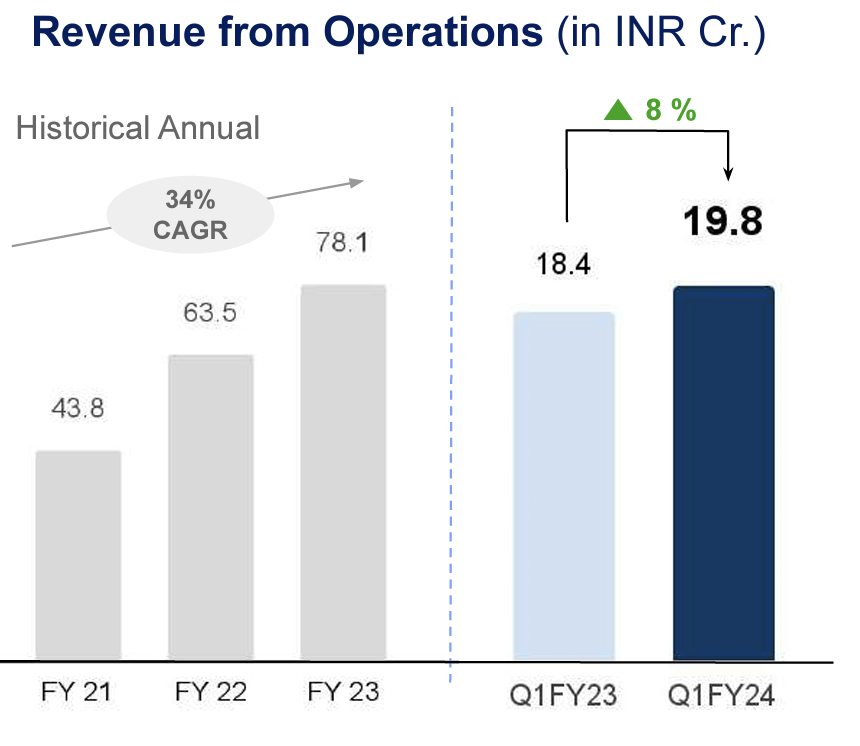

Its total customer base as on date stands at 1190 customer accounts, with 3 users per account (3400 users). Average pricing per account comes at Rs 6-7 lakh (for 3 users). Of ~Rs 80 crore of ARR, ~70% comes from international clients and ~30% from Indian clients.

Overall customer accounts have grown at ~23% CAGR over FY20-23, from 640 accounts in FY20 to 1190 today. At the same time, Tracxn has been able to take ~8-10% price hikes pa over this period, resulting in revenue CAGR of 30%. However, due to slowdown in private markets, customer account growth has slowed in recent quarters (~2-2.5% QoQ increase).

Who would be a typical customer? Key customers would be private equity investors, investment bankers, government agencies 7 corporates. IB & PE investors account for ~55-60% of the customer count. As per a Pitchbook report, there are ~10k active VC investors globally, 5x of what it was a decade ago!

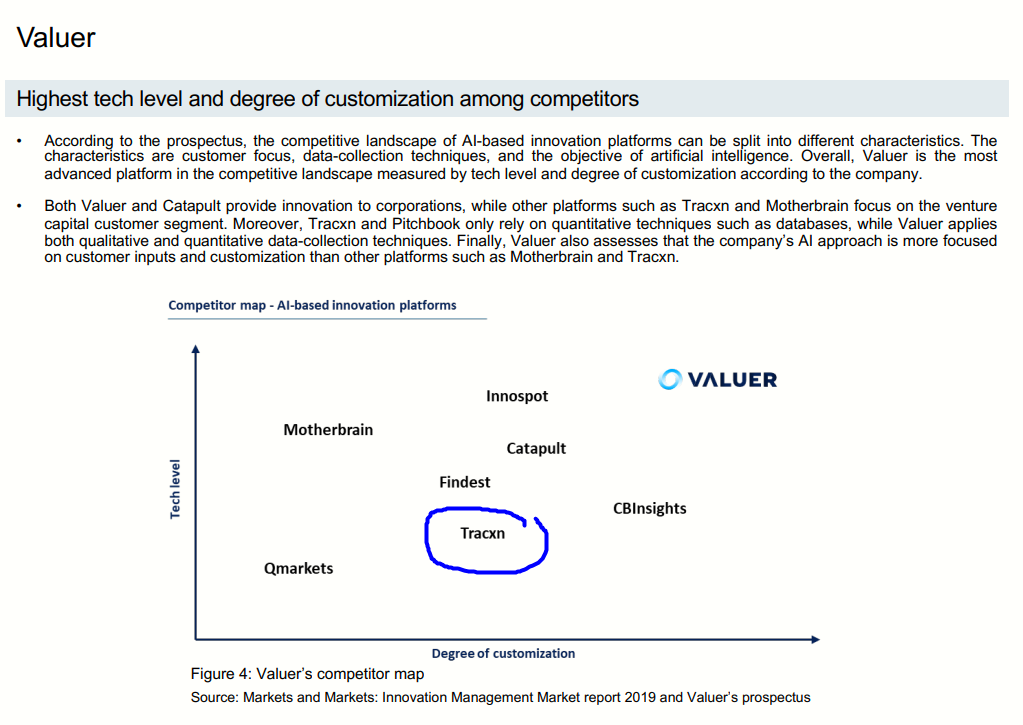

As per channel checks (ex-employee), (1) Quality of report & data accuracy of global player like Pitch Book is far better than Tracxn, however Tracxn’s subscription cost is far lower (cost advantage), (2) Tracxn has an edge in terms of profiling on Indian companies (data depth), hence even the global PE/VC firms have a subscription along with others like PitchBook, CrunchBase).

They operate with a team of ~800 people (450 data analyst, 220 sales & marketing, 80 product & tech)

Positives (growth in PE/VC firms, low cost, op leverage possibility)–

Growth expectations. Over the medium term, growth drivers are growth in PE/VC firms globally & in India.

Low cost advantage. Being based out of India, Tracxn has the advantage of low-cost employee. Despite quality of Pitchbook reports considered to be superior to Tracxn, Tracxn is far more economical (Tracxn subscription cost is 60-65% lower than Pitchbook).

Supposed to showcase operating leverage. Once a company is profiled, then the software uses web-crawling across a wide range of online data to update. Incremental human effort is limited to verifying the broad-level accuracy. Hence, the business model should yield operating leverage as more customers use the existing data.

Risks (Competition, Growth risks, weak S&M in past) –

Quality & detail of report of Pitch Book will be higher than Tracxn in global context.

FY18-22 they showed meaningful op. leverage as 75% of incremental revenue flowed to EBDITA. However, over the 9MFY23 as revenue growth has started to plateau (also impacted by slowdown in pvt market), op leverage has been much lesser (30% margin on incremental revenue).

Sales & Marketing aggressiveness was missing till now, but they are catching up by hiring more salespeople. Mainly use online channels including emails, social media, and search engine optimization.

Management Overview & Forensics (Good corporate governance, growth hunger yet to be tested) –

Founded by Ex-PE employees – Neha Singh (ex-Sequoia) and Abhishek Goyal (ex-Accel), backed by Flipkart Founders, Mr. Ratan Tata, etc.

Overall Corporate Governance is good.There is room for improving overall employee retention, as per an ex-employee attrition used to be higher than industry average.

Promoter Group Holding 35%, Institutions 30%, Public 35%

Valuations have started factoring in near term slowdown, medium term risk reward now more balanced

At the current scale, business is Rs 80 crore ARR, largely breaking even at current scale.

Ignoring the near term growth slowdown, fair case would be to build 25% revenue growth (mix of price hikes & account growth) over FY23-25, yielding Rs 140 crore revenue. Assuming 10% cost inflation, it would imply 60% op margin on incremental sales, yielding FY25 EBIDTA of Rs 40 crore, Rs 30 crore PAT.

At Rs 600 crore Enterprise Value (CMP Rs 66, Cash on Books Rs 60 cr), it would imply 15x FY25 EV/EBIDTA or 20x FY25 PE (reasonable for high op leverage which future growth will be expected to bring in).

Fair value for Tracxn depends a lot on how the execute on (1) Growth in overall revenue, (2) Extent of operating leverage. There could be near term pain given slowdown in private market, which is partially built in prices.

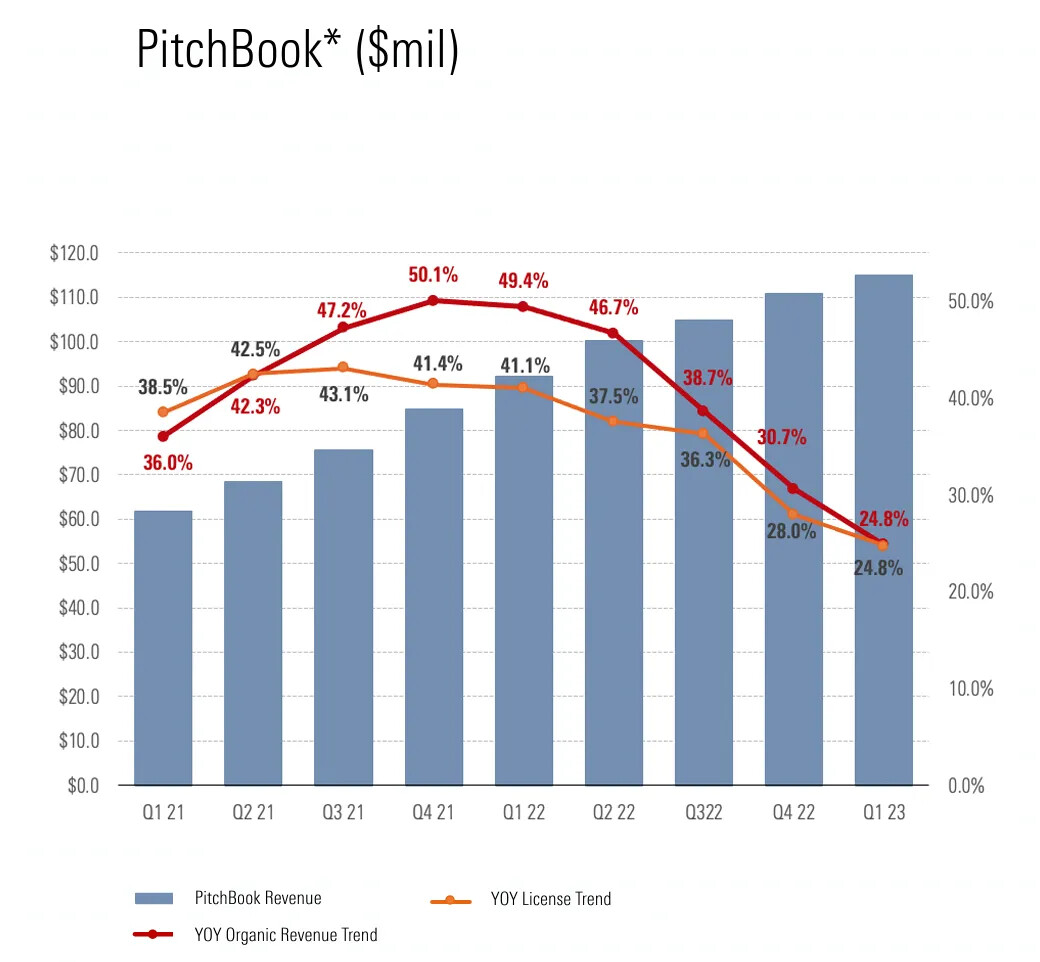

Pitchbook in FY16 had revenue of 30mn$, when it was acquired by Morningstar for 225mn$ (7.5x P/Sales). Tracxn today trades at 7.5x EV/Sales.

They are of good use to VC investors, they use it like we use screener for listed equities.

For PE investors, it has limited use case.

Cost of Tracxn is much lower than Pitchbook subscription, though PB has richer quality data globally.

There is no risk from Chat GPT or various AI tools, as the uniqueness of these software is the organized way of data, and it also includes data from MCA, etc. which an AI might not have access to. It is much easier to compare & filter cos in Tracx or PB than use AI tools for that.

I just watched their Q1FY24 earning call. I have been running a health tech start-up for 4 years now and very frequently come across various insightful data points and reports from tracxn.

Loved the analogy of tracxn being screener for VC firms (was my first thought too).

IMO one future growth driver for them (not mentioned much elsewhere) could be serious angel investors (individual/groups) who invest directly in startups/ sectors based on their research and insights via platfotms like traxcn (just like what we do today in secondary markets).

I feel we have already come a long way from mainboard stocks to SME stocks and AIF being mainstream for retail investors. Natural extension for this trend would be a way to invest in high quality/ high growth private companies/ start ups.

One more use case couple be to collab with data players of publicly listed companies (brokers, players like screener, moneycontrol, smallcase, etc.) to share some data tgrough APIs for comparing public listed companies with their private counterparts (e.g. Britannia vs Parle or Zomato vs Swiggy).

As their customer are generally crème de la crème and going ahead angels/VCs are going to grow much faster in next decade compared to the previous one. So TAM is only going to expand.

I genuinely feel that current funding winter and dull private market is the best time to research and accumulate such stocks.

Industry: Public markets are growing at 6% CAGR and private markets are growing at a double speed of 12%.

Financial data companies focusing on public markets have created a revenue of $30B. Now private markets started becoming mainstream. Public market size used to be 18.3x of private markets in 2015 and it inched to 13x in 2020. (Ratio coming down is a +ve signal to private markets growing).

VC as an asset class is generating highest returns so far for endowment/soverign wealth funds. Allocations will always continue to the asset class for next 10 years.

In the private data players, Tracxn comes 3rd in terms of revenue after Pitchbook and Crunchbase (Crunchbase est $30mn+ revenue).

I loved the operating leverage angle in data business. This works out well when there is growth. Right now due to funding winter growth got stalled across geographies.

Cons:

Sales & marketing /Product pereception - not as strong as Pitchbook.

Market leader pitchbook is able to grow between 25-50% levels on a larger base of $240-430mn in last 9 quarters while tracxn is only growing between 25-30% at a small base of $5-10mn. Usually, growing on small revenue base is easier.

Tracxn folks always tell in con calls that they don’t do aggressive outbound sales and they use the funnel on their website to catch prospective leads. I don’t know the exact reason for subdued sales.

In other enterprise businesses like CRM tools etc,. folks would go for cheaper alternatives. In data business, folks will go for provider where quality perception is high. At this moment, Pitchbook scores high in this in this industry. Extending this, folks don’t switch to cheaper providers to save costs. In the VC/PE industry, opportunity cost and salaries are higher compared to what you save by switching from Pitchbook to Tracxn.

Disclosure: Have a tracking position but don’t see the tail winds yet. Tail winds could be revenue growth in the order of 15-20% YoY.

@harshitt1993@Sumanta_Das - From the DHRP and other online materials, I see very few global players. But, do we have any listed global players as private market data providers? One other question is, since the data sourced is openly available, what value-add does Tracxn bring to its customers against the competitors?

No listed peer is available. Yeah, you are right. Only 5-6 Players are available in this market.

Data is also available for public markets also. But we use platforms like screener, tickertape etc. Because they show those data in an organized manner. Also, it is difficult to get data for private market compared to public market. So, Private Equity investors have to use any platform for research.

2.Investing in scaling up organic traffic, press mentions, expanding coverage in financials and captable data sets, and improving paid customer engagement and account expansion

I have few questions. Requesting you or other informed members in the group to thrown some light upon.

Any idea why FIIs and DIIs have been selling during last 2 quarters? Together they have reduced holding by ~15% in 1 year. Even promoters have sold ~1%.

Is it correct to assume that Fed interest rate cuts would result in some increase in PE / VC funding and therefore may benefit this counter?

If Tracxn are taking price hikes per account, are competitors doing the same? Is there a point where the cost vs quality curve turns against Traxcn? Is cost effectiveness a permanent moat?

Does Tracxn have a moat when it comes to gathering information about Indian start-ups?

How much of the start-up friendly and favorable Government policies in fostering a culture of entrepreneurship real and how much of it is narrative? Any insights or data or articles on this would be welcome.

During the last concall, the promoters said that they have been buying the stock and they had data from NSE to support that. Possibly it was the effect of ESOPs diluting the shareholding.

Lower Interest Rates would result in money flowing outside US for better returns. So I think it would be safe to assume that lower interest rates would have a positive impact in the company’s business.

Tracxn has positioned itself somewhere in the middle of the price range in the market. There are a few companies which charge a lot more than Tracxn, and then there are a few smaller players who charge lesser than it. Considering that there is an increasing dependence on AI, I am not really sure if the company has a moat. I would love to know more about this, from learned members in this forum. Also, considering that Pitchbook (Traxcn’s competitor) is owned by Morning Star, I am not really sure if cost effectiveness would even be a moat in this case.

I have nothing to add here. Would love to hear opinions of other members.

Results came with low sales growth and massive fall in profits YoY as previous profits were inflated due to exceptional items and tax was paid this time.

My personal view. It’s a great company at current price level. It has the presence of operating leverage - Check the increase in revenue vis a vis increase in expense.

It has presence of fixed cost elements-like cloud hosting charge - which is constant (c. inr 2.5 Cr per annum) .

No doubt - results are subdued , but I personally think market has over reacted.

Trap is high valuation - optically it looks cheap, but it is not. Last year they have recognised Deffered Tax Asset of 23 Cr . Which resulted in high level of profit. ( refer note 8 of the annual report)

You say that it is great company at current price level but also say that it is a trap at high valuation. I think the PE is around 100 if we remove the 25cr of profit. Can you elaborate a little further as to how it is good value right now? Is there scope of exponential earnings?