What is your read of these reviews on Glassdoor?

Culture needs to be improved a lot. A lot of people exit the company in a short tenure and its not a sustainable way to build a business. The promoters need to take note of this and take remedial measures about the same.

For instance, read the Glassdoor reviews of their competitors like CBInsights, Pitchbook, etc - the numbers are green and it speaks volumes about how the company is run today.

4 Likes

Pitchbook is part of Morningstar.

If you see morning star’s results, they publish pitchbook’s revenue separately.

1 Like

I am reproducing my blog post on the company here

Business Model

The company provides a database of unlisted companies. Such a database is valuable to private market investors, M&A teams of big corporate houses, etc. They charge their customers an annual subscription amount for each license. Other than this they also allow their customers to access their proprietary database with APIs.

Founder and Management

There are two founders, Neha Singh and Abhishek Goyal. They started the company in 2012 and both themselves were employees at VC firms before that. So they understand the pain points pretty well. They hold about 35% equity in the company as of date.

Product

The company is constantly adding to the database that they have. For example they have private company data for about 50 countries. But now they are going deeper. They also have the cap table data for private companies in about 15 countries. So the company is trying to ensure that they have more and more structured data about all private companies of the world. My opinion is that going ahead the company will use more and more tech to better organise the data that they have and also to collect more data. I don’t think the founders are hard core techies themselves. But they do have a 70 member tech team. In this company’s case I am not sure though who is obsessing about improving the product day in day out. In the long term that is the biggest differentiator for small companies. That someone is really obsessed with the product.

Distribution

They have 70% of their revenue coming from outside India. Right now they do not have sales teams on the ground anywhere in the world. Instead they depend completely on inbound sales. So anyone who comes to their website and asks for a demo is then given a demo over a video call and then it is hoped that the lead would convert. Also once they sell one license to an organisation they try to increase the number of licenses sold to that organisation over time. This product has some network effects. For example the more customers they get the more they understand what other kinds of data they should collect. And the more data they collect the more kind of customers get attracted to them.

Brand

The company constantly does brand building by releasing reports. For example you might have seen many media reports about the current state of private market funding in 10-minute delivery. If you look at the source it is usually mentioned ‘Tracxn’. So the company is basically trying to put out a lot of information for free and then the company is hoping that that information will reach the right target audience who would then come to Tracxn and ask for a demo. But even if very few people actually come to them to ask for a demo, so many free reports and media mentions are bound to build a brand for Tracxn over time.

Financials

The revenue growth is totally dependent on global interest rates. If they come down then private market activity goes up and the company sees healthy growth in revenue. Otherwise the company sees low growth in revenue. Most of the capital expenditure or fixed cost expenditure needed has been done by the company. As a result we see huge operating leverage playing out with every rupee of additional revenue earned. The company is claiming that going ahead 50% of all additional revenue should go towards EBITDA. The company is completely debt free and has about 70 crores of cash on its books and this number keeps going up quarter on quarter.

Bull case

The private market would pick up since public markets have been doing well since March 2023. Fed would start reducing interest rates over the next couple of years. Thus the company will start throwing up lots of free cash. Also, the company will discover inorganic growth opportunities and put its cash to use. Hopefully such acquisitions would be accretive to the bottom line. The company can also discover adjacencies to its current business model. For example they might be able to convince companies all over the world that they are a great tool to identify vendors. For example if you are a SME and are looking for distributors in a new geography, Tracxn can be the platform through which you carry out your research. Or public market investors will start using AI/ML models which need a lot of private market data too and therefore the company will start finding more API customers for its database. Or may be organisations can start using the Tracxn database to identify sales opportunities. For example an IT hardware vendor who is looking to identify fast growing small companies in a particular city in India. If any of these adjacencies play out then we will see huge operating leverage since the cost of serving an additional customer is negligible for the company.

Bear case

The Fed would keep interest rates higher for longer. As a result private market activity will continue to remain subdued. Also, more and more private market companies would realise that the only sustainable way to access capital is the public markets and therefore we would need to list much earlier in the company’s life. In this case the company’s revenue would see tepid growth. And therefore the company would sort of stagnate.

P.S. My internal blogs/drafts for this post are below.

Disclaimer: The views expressed in this blog are personal. I may or may not hold investments in the stocks mentioned.

Saturday, 3 February 2024 at 9:25:40 AM

I started studying them yesterday. I had some interaction with the founder Abhishek in 2011 when I ran my own logistics company. He was trying to do something in the beauty space similar to what Nykaa is today. He was very encouraging and helpful to me at the time. He had worked in VC firms or VC backed firms for a few years before starting out on his own. His CFO then Prashant is the same guy who is his CFO now in Tracxn. So he is one of those good guys who also end up doing well in business.

Now let’s come back to Tracxn. What do they do? They are a website which is useful for the purpose of research. What kind of research? There are two kinds of companies. One who are publicly listed and once who are still privately owned and hence not publicly listed. Now there are big companies which collect all the data on publicly listed companies and then they allow anyone to research through that data. Think about Bloomberg. Any stock analyst working at an investment firm globally would rave about the ‘Bloomberg terminal’. He would say that it is so easy to get the data from the terminal. You would push him and counter that all data is freely available on the internet. Why do you need to pay a hefty subscription fee to Bloomberg to access the same data. And he would tell you that you are not being sensitive to his business model. An analyst has his brain and his time. He needs to use both to figure out what to buy and what to sell. Sorry I missed money. He also has a pot of money which he wants to invest on behalf of his clients. Wait. Before we go ahead let us understand who his client is.

And this takes me back to the long running theme of digitisation. Look earlier may be 50 years back, holding capital was a huge moat. There were very few people in the world who were not working class. What is working class? These are those people who have to work for money to buy bread. If they don’t work they will not have bread to eat. This is separate from the capital class. Who is the capital class? These are people whose money works for them and brings them so much money that they have a choice whether to work themselves or not. The capital class will always have bread to eat. They own lands from which they collect rent or they own stocks from which they get dividends or they own fixed deposits from which they get interest. Now as the money supply has increased in the world over the past few decades, the capital class has benefited. Because the value of their assets has gone up. But the capital class always looks to recycle its money/capital back into the economy so that the capitalist can make even more money. As a result money keeps coming back to the asset classes that the capitalist is most comfortable with. This means that land and the public stock market keep getting a lot of money back from capitalists. But once a capitalist has too much money he starts experimenting with new asset classes. For example he might dedicate 2% of his net worth to buying art. Or to buying crypto. And then the capitalist will keep observing how these asset classes perform over a long period of time. Some of these asset classes will not make him any money. For example he might invest in an ICO and then lose all his money. But sometimes the asset class works and makes the capitalist a ton of money. And then the capitalist just keeps pouring more money into that asset class. And other capitalists learn from him and they also start putting money into that asset class. And over a period of decades a new asset class is born. Entrepreneurs also start building for that asset class since they now know that they would have the backing of capitalists for the same.

One such asset class is private markets. This is basically a company which has not been listed on the stock exchange. About 50 years back if you were starting your own business you were going to borrow money from friends, family, bank, etc. Or you would work for 20 years in a job and save some money and then start. Now there is a lot of capital which is available to support your business in addition to these traditional sources. And that is the private market investor. This is the capitalist who now wants to allocated a small percentage of his net worth towards startups. Or companies which are making good revenues but are not public for some reason. May be they will become public in the future and that is when the capitalist would make a lot of money in the IPO. And that is why this asset class attracts capitalists. I think there is one more reason behind money being attracted to private markets. Earlier the capitalist was one of the few people who had capital. So he could get into a business which solved a real problem but required a lot of capital. For example he could open a textile mill. He knew that even if the business does not work out the underlying land in itself will keep going up in value and as a result he will not lose money on his investment. Also, he knew that very few people have their own capital to buy so much land and machinery. Even the bank would be very sceptical about lending so much money to anyone who is not a big capitalist. So therefore the capitalist found a moat: his own capital gave him a huge advantage over the small entrepreneur. Because of digitisation that advantage has eroded significantly. Now the capitalist does not only need money, he also needs skills to compete with an entrepreneur who is highly skilled. This entrepreneur can build something online since the real estate cost of online is so cheap. You just need a cloud server. And suddenly you are making life more difficult for the capitalist if he wants to take on a skilled entrepreneur more head on. So the capitalist has been forced to compromise. Instead of fighting the skilled entrepreneur the capitalist partners with him. So the capitalist goes back to his role of financier. He is the most comfortable with that. He has been doing it for centuries. And the capitalist is well diversified across entrepreneurs. Even if one entrepreneur does not work out, the capitalist would make tons of money due to the efforts of the other entrepreneur. And this particular entrepreneurs also gets a good deal in return. Instead of putting up collateral or pleading with banks, he gets patient capital from someone who can teach him a thing or two about the psychology of money. Also this entrepreneur himself will become a capitalist at the end of his entrepreneurial journey. This entrepreneur would also start diversifying his pot of gold as he starts making money. Think about start up founders like Sachin Bansal who also invest heavily in other startups. So I hope I have now established why the private market is here to stay.

Sure you might see contraction in the private market. If interest rates continue to remain very high for the foreseeable future then private companies will have no option but to come to public markets quickly. Public markets allow any company to tap a huge pool of savers. Even small capitalists (who still remain working class themselves) can participate via mutual funds. But public markets put a lot of constraints on the entrepreneur. He cant afford to show multiple bad quarters and therefore would have to keep taking some short term decisions. So the net effect is that even after high interest rates private markets will not disappear. Their growth might get constrained. But they will continue to exist and grow and will continue to get a larger market share of capital as compared to the public markets.

And this is the bet that Tracxn is taking. Unlike Bloomberg which majorly serves customers who need data about public companies, Tracxn is working to give data on private companies. So obviously they are of a lot of use to VCs and PEs. And Tracxn does not do this just for the companies in India. They do this for companies in more than 50 countries. So if you are a German investor and only want to invest in German companies, you can come to Tracxn and get started with your research. Tracxn is taking advantage of the increased digitisation in the world. Data about private companies which was not available digitally till now is now quickly getting digitised. And all Tracxn needs is an API call to get the same data into its database. So they are constantly working to figure out new data sources in the world and then they are trying to get that data into their servers. So think about a country like Indonesia. May be they have a government department which is the equivalent of Ministry of Corporate Affairs in India. This department would get annual filings of all private companies in the country. May be these annual filings would also have the cap table of the company. They would for sure have the financials of the company. Now if you are a private investor in Indonesia how can you get access to the same data. Sure you can go to the website of the Govt and try to get this data. Or you can build your own web crawler to access such data. But that involves a lot of technical skill and time. Why would you not instead pay 7000 USD annually to a company which gets you all this information in a clean manner? Let’s come back to the life of an investor or analyst. What is his raw material? It’s the capital he has access to, his brain and his time. Now how would he make the most efficient use of this raw material? He would look at all possible sources to save his time. He can get access to more capital and to more brains (by hiring more people), but he cant create more time. Therefore an investor goes out of his way to save his time. He would take flights to travel between cities, he would pay money to ensure that a dinner reservation for a particular time is available, he would buy a clothes dryer instead of hanging his clothes out in the balcony. And thus Tracxn should be seen as a time saving tool for him. Tracxn helps him research companies quickly. And the platform keeps adding more capabilities. They currently cover about 2.5 million companies and they claim to add roughly 12,000 companies a day to their database. They allow the user to customise his dashboard as he seems fit. They are doing all they can to help the investor cut through the noise and get to the signal. Both the founders of Tracxn were in private market investing in their previous jobs. That is why this is a problem they have keenly felt. It is a pain point they deeply understand. Their independent directors today come from the same industry.

There is one more reason why I think their platform has value. And that is AI. The more cleaned up and accurate data that you feed to an AI model, the better is that model’s predictive ability. Tracxn has a 170 people tech team. I am not sure yet how are they incorporating AI into their platform such that their users are able to work even more efficiently. Think about a Tracxn AI assistant whom I can ask to give me a list of the top 10 companies by revenue which are registered in a certain PIN code in India and which work in the restaurant industry. Now if the Tracxn AI assistant can understand this query in natural language and can then without hallucination give me a great answer, then I dont mind paying them 30,000 rupees a month. Think about how much money a competent research assistant would charge for this monthly. Also Tracxn allows API pull out. So if I am building an AI model which needs regular updated private company data then I can just go to Tracxn and pay them 30 lakhs a year and pull out data from their database to feed clean data to my AI model. As the use of AI grows in everything, clean data would be a constant requirement and that is where I think Tracxn can be a great source. And not just private investors. This kind of data would be needed by universities and other companies too for their sales and marketing. If you are a SaaS CEO then the whole world is your potential market. But how do you know which customers would be the most relevant to you. Tracxn can be a great source to get that search started. Right now I think more than 50% of their usage and revenue would be coming from the investing community. But I think in the future the wider world may find use cases for Tracxn.

On the financials too the company is hugely profitable. Why do I say that even though the EBITDA margin is only around 10%? I say that because of operating leverage. Any future revenue would mean that 50% or more of it will go towards EBITDA. And therefore over the years we should see this EBITDA merging ballooning. Their cost of serving an incremental customer is negligible. And therefore all that revenue hits the bottom line straight.

Let me now cover the biggest risk I see. The biggest risk is that they are unable to increase revenues. Their DRHP claims that the total annual revenue that data companies in the private market space are making today is 1.3 Billion USD. Tracxn’s annual revenue is 20 million or so. And the industry itself is growing at 7% in USD terms. With rupee depreciation we can say that the industry is growing at 10%. So this is not a high growth industry. How would then the company grow its revenue? One option is that they pull business from their competitors. This is always a difficult task. Nobody gives up their revenue. If the final customer only wants to use one such data company then they would need very strong reasons to switch from their existing data provider. Price cant be the reason. Their users don’t have a problem with paying a high price because as a percentage of their overall cost budget this is miniscule. So how will Tracxn pull away customers from competitors is a mystery to me. Another way of increasing revenue is to capture more and more of the new customers who are available. Here the company is trying. But the problem is that theirs is an inbound sales model. Tracxn puts out 14,000 reports annually in the public domain and then they hope that people would find enough value in their reports and then come to their website and ask for a demo of the platform. This is the only way that they do sales right now. They do not have the muscle to instead go out there and sell to the purchasing manager for a private investor or for a university. And they haven’t shown any inclination as of now to build that muscle. They seem content with trying to generate leads for inbound sales. Another way for them to increase revenue is to find other use cases of their data. For example can they build something like an Angel List where private investors can also do deal management? Or can they build a revenue based financing model? I am not sure which adjacencies they can build into their business. May be they can start organising match making between academia and the research needs of capitalists? I don’t know. I haven’t read anything which shows me that they have started finding this new set of customers.

This is my read of the company till now. I am reading more about them and will update soon in the next internal blog.

5th February at 8 PM

So after having all available concalls of the company I have come to the realisation that this is a deeply cyclical business. We are right now at the bottom of the cycle and things should improve from here. The private markets are at a 10 year low in terms of deals happening or funding happening or fees being made by investment bankers. As interest rates begin easing or at least as they stop increasing, we should see a pick up in private markets. The drop in funding or the negative growth rate in funding has come down to around -25% from -44% last year.

So as the market starts recovering (and this could be a slow and uneven recovery), we should see more revenue as more customers start increasing their licenses with us or more customers start using us. I think the company has also realised that inbound alone is not a great plan to generate sales. They have finally mentioned on the latest concall that they will start some sort of feet on street activity and they will see how it impacts their customer additions. I think it will take the company some time to build up this muscle and that is fine. May be it will take them a couple of years to do that. Till then they will ride the coattails of the private market picking up.

After all this reading I think the moat of the company is in mapping companies to the exact industries they belong to. Each company that comes into their database is very granularly labelled to make sure that it is being defined well and therefore anyone in the world looking at thousands of companies in a particular area can narrow down to this company fairly easily and quickly. Basically they are using humans to label data so that AI can easily make sense of that data. They are able to do this better than their competition because they have access to cheap and well trained labour in India.

They also keep understanding from their customers what more can they do which would meaningfully make the product more engaging for their customers. So they have a good set of customers who are sort of helping them co-create their product roadmap. I think in a few quarters from now we should see increased adoption of the product in the target market. The current set of customers may find that with AI and ML the platform has become really good in monitoring whatever the user wants. At the same time those industry players which are currently being served by the competition would also start using us. They would not leave the competition. I am sure that they really have deep integration with the competition in their everyday workflows. But then there would be something unique in Tracxn which would help them figure out something new. And then they would decide that it is worth paying two companies and Tracxn will become the second company especially because Tracxn is so cheap for them to use. So it wont hurt if they buy a single license and then take things from there. And may be public market investors would also start figuring out something useful in Tracxn. Let me illustrate with an imagined scenario. You are a public market investor and you are invested in a small public company which works on a niche area and which the management of the public company claims is a very fast growing niche. Now you need to validate the claims of the management. How do you do that? Especially if there are no listed companies around. One way is that you find the few private companies operating in the same niche and in the same geography and you try and speak to them and validate the claims of the public market company. This is just my imagination right now. Let’s see if something like this starts happening two years from now.

So the company will continue to plod along but somewhere along the line they will hit a big use case which will resonate with a ton of users and that is when we should see hockey stick growth in the revenue of the company. And since this is a company with a huge operating leverage so EBITDA growth would be even faster than the revenue growth.

The basics of the company are covered. They keep their employees happy. At least the top management. They do appraisals throughout the year basis the joining date of the employee and they also offer ESOPs constantly. They see ESOPs as a currency and they can afford to do that now since they are now publicly listed.

They have a good clean management.

The downside could be that the company starts degrowing as the private market pick up is indefinitely delayed. And the management starts taking reckless calls with the cash that they have accumulated. For eg paying themselves fat salaries or issuing lots of warrants to the promoters or making acquisitions which would not be immediately bottom line accretive. So that is the risk to which I dont have an answer right now. But this seems like a good buy to me at the current price.

So I am going to buy this company as soon as I get my next exit from all the portfolio stocks that I currently hold

23 Likes

Hi Aadhar,

Thanks for sharing the detailed post and insightful thoughts.

I have a question on the possibility of scaling top line with cutting interest rates and more funding flowing to private market. Is tracxn’s top line proportional to private equity funding or number of customers deploying the funds? In other words, if interest rates reduce, and as more funding flows in, it may be coming from the same set of customers who already have accounts with Tracxn. So they do not need to open more accounts. Therefore, while funding may grow, Tracxn’s top line may not since number of individual PE / VC firms may not increase. More funding in PE space may simply come from most of Tracxn’s existing customers. So, while there may be some increase in the top line with easing interest rates, do you expect a big jump?

By the way, your bull case optionalities do seem real business cases and wish Tracxn management is thinking on those lines.

4 Likes

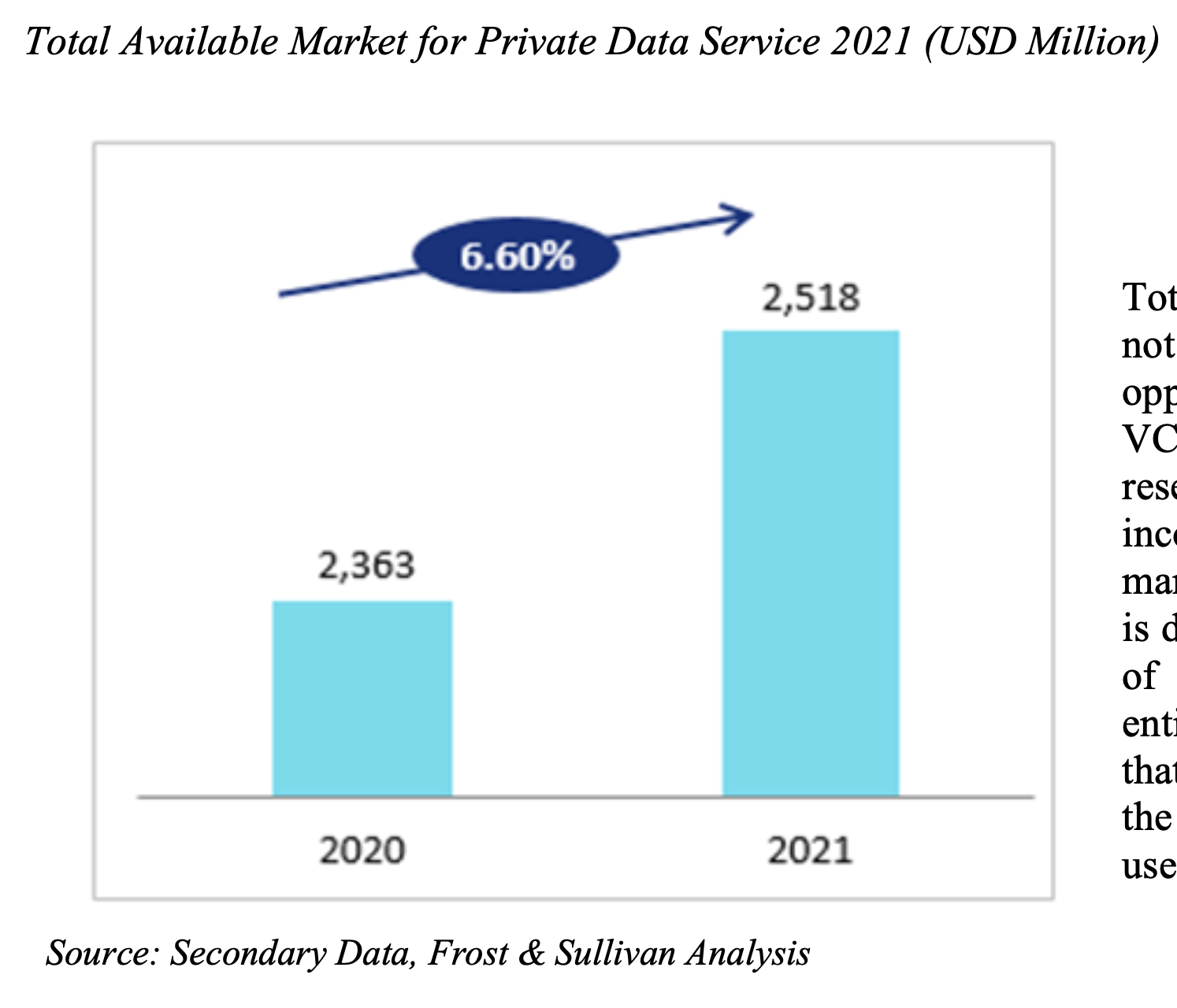

Please refer to the RHP of the company. I am attaching it. Go to Page 133.

As can be seen from the below image the total revenue that private market data providers can earn annually is in the ballpark of 2.5 Billion USD. Tracxn’s revenue share in the market is less than 1% of the available market.

But I think your question was specifically asking about the number of customers available to capture. Look at the screenshot below. It mentions that as of now the penetration of data service providers in the industry is 50%. This means that Tracxn has 50% of the market available today and these customers are not using any data provider at all.

Please do note that these estimates should be taken with a pinch of salt. I am trying to figure out another data source which can validate the size of this market.

RHP_20221004195631.pdf (6.8 MB)

1 Like

Just wanna share some of the questions and still thinking about these. Tracking the company

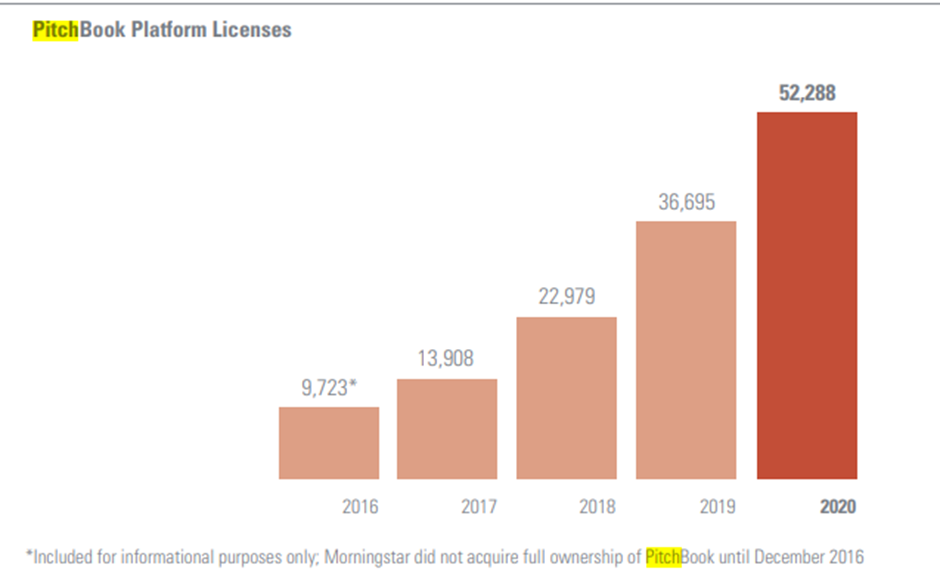

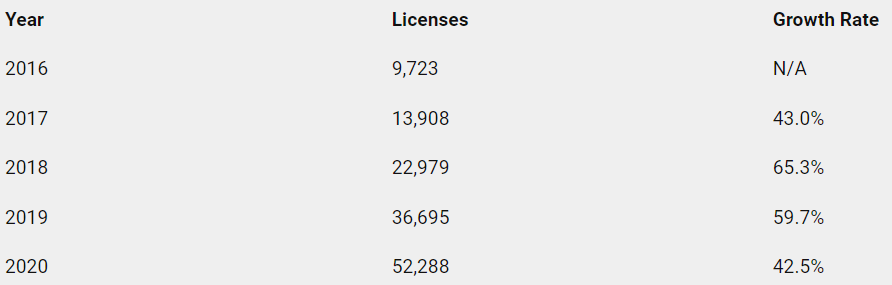

Morning Star acquired pitchbook in 2016.

License growth for Pitchbook

Revenue from 2016 to 2024. Approx

i have some questions like for such a small company. Does Market really matters?

2. They started hiring huge sets of employees and started reducing them. Why? Do they doesnt know how many are required to do?

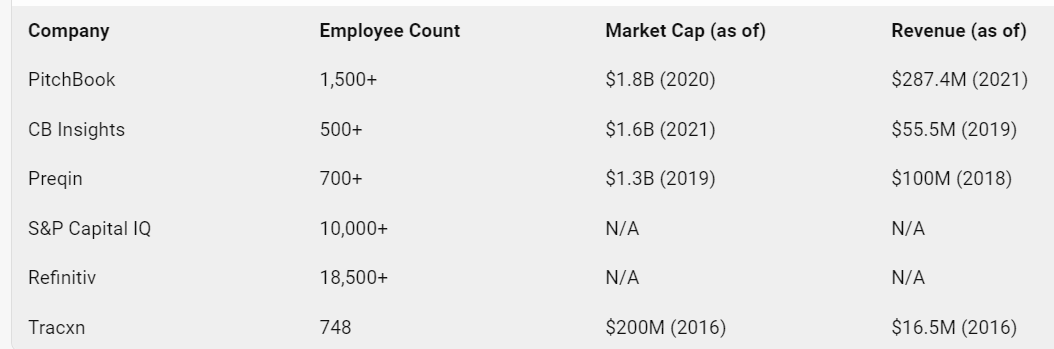

3. We Can check the employee count of Pitchbook Vs Tracxn Vs Other Peers ?

Am trying to give a sense of idea that. Promotors are the key players in the game. Please do deep analysis before take a share in Small companies

6 Likes

Being an ex employee of Tracxn, I have noticed that the biggest problem for tracxn has always been a subdued topline growth. # of new clients addition has always been too slow and likely to remain like that unless they start some ancillary services also.

10 Likes

Can anyone help me understand what could be the reason for slower growth in customer addition than the competitors? Ideally for a company with such a base should show higher growth? Are they lacking in the value provided to the customer?

2 Likes

Thanks for detailed note and appreciate your blog material. I have following questions

- is there any indication or metrics published on Tracxn customer satisfaction survey, whether their customer able to derive business value / outcome out of their subscription fee

- what is % of customer renewals or renewals revenue on their existing subscriptions say if it is for 1 year or 3 years?

- Is there any plan on fine tuning public LLM with their data like you spoke about ML is need of hour ? Are they hosting their platform on any hyperscalers or colo datacenters

1 Like

Was trying to do some scuttlebut on this and was talking to my friends in PE industry. Looks like Tracxn has major issue with data accuracy and hence clients close the subscription or reduce licenses after sometime as the data is not v reliable.

6 Likes

I do not have any data metrics which talks about customer satisfaction. Check page 17-18 of the concall transcript below. They do mention about their customers raising thousands of feature requests to them using ‘My Analyst’. This I believe is a feature in their application.

879f6f33-8145-4950-b0a9-31ef787d1238.pdf (442.1 KB)

They have a renewal rate of 74%. You can read more about it in the below concall on page 18.

4db3b29c-e66c-47fb-a8dd-e0fc36697425.pdf (447.8 KB)

They have not specifically spoken about training any AI model with the data that they have. They use hyperscalers to run their application. I haven’t found any mention of colocation data centers.

3 Likes

I am not able to come to terms with their valuation, if i remove the one time tax benefit which they got in mar’23 then their normalized earnings come out to be around 7 cr (e) for FY’24 which at current price would mean a 200 PE multiple.

Any thoughts on the same?

I agree with you. For our analysis we should ignore deferred tax benefit that they will get in the future. I think they will generate about 10 crores of profit in FY24. I am also including the interest income they will generate from their cash reserves. That still gives us a PE above 100. I agree with you that they are very richly valued today.

4 Likes

Wonderfully put. I loved your clear thesis. Right now at a discount at 90. with a trailing PE of about 100. Our bet has to be on revenue growth. Right now its just margin improvement. But it can be a dynamite with revenue growth. Will study further.

1 Like

I see the holding percentage of the co founders are decreasing on quarter on quarter basis what can be the reason for the same

1 Like

That is from the dilution of equity due to ESOPs given to employees, as I understand.

1 Like

I have one of my friend working in some small startup working on same idea, but he says the revenue growth like his company with a total employee strength of 150 people within 4 years of business is profitable as well as doing revenue of 80 cr same as tracxn and they cater mostly to US and Europe markets and are growing more than 15 to 16 percent on yearly basis but if you see tracxn which is in business for more than 11 years have a very poor revenue growth with employee strength of more than 500 people ,any thoughts on this

1 Like

How can I check if possible can you explain

Interesting!

Wondering what would stop someone to take the data from Tracxn through memberships, re-format the data and present on a different website at lesser cost. I am not saying this may be happening in the case of your friend’s company but this example you gave projected this thought.

Is this kind of plagiarism stoppable?

1 Like