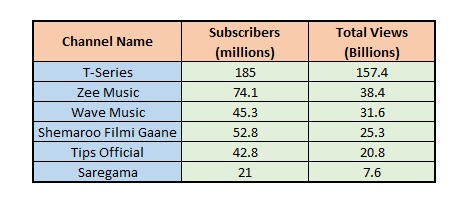

I also saw this huge difference in number of youtube subscribers for Saregama, Tips and other players. I was confused as to why Saregama with such a large catalog lags so behind tips in terms of Youtube subscribers and views as you have shown. The first reason that came to my mind is that Saregama is having a majority of catalogs that are very old. But if you see Saregama generated a revenue of 101 crores from music business whereas Tips did 27 crores. Having an old catalog can mean lesser revenue or viewership per catalog, but that can in no way mean lesser overall viewership.

So I was confused and I got an answer to this in Q2 concall.

So prior to 2001/2003 music video rights went to film producer/ negative rights owner and thats why Saregama has a lot of lyrical videos in their Youtube Channel.

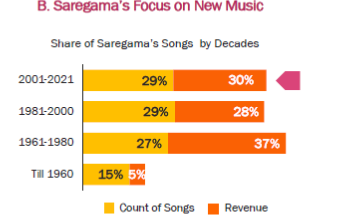

Lets have a look at the age of Saregama’s Library

So only about 30% of the overall catalog has video rights in Youtube. So I would say the viewership that we see is for 30 % of catalog for Saregama whereas for Tips, Zee and T series, the majority of catalogs below to post 2000 periods.

The data for streaming in mediums other than Youtube ( being visual) should be totally different which is evident from revenue difference.

Exactly! This means that we cannot expect Saregama’s YouTube channel views to increase by depending on old songs rather, we would need new content like “Pani Pani” song. But for riding the music streaming wave, Saregama is well positioned as there we don’t need videos.

Slight observation: When I had used YouTube Music a year back, there we click on music videos popular on platform. Therefore, if YT Music becomes the norm (like Sportify) Saregama could lose out on old songs as most popular ones are with the video.

I don’t think so. Because as per management’s statement there used to be two separate rights: Video(which definitely comes with its own audio) + Music alone. Therefore, if someone is playing the video then I think there is no need to pay but the industry has changed and now the music label gets both.

This is what my interpretation is towards Saregama’s management statement.

Yes, the music company has copyright if the music is shown with any other video, other than the original video. As per YouTube Copyright owners can set Content ID to block uploads that match a copyrighted work they own the rights to. They can also allow the claimed content to remain on YouTube with ads . In these cases, the advertising revenue goes to the copyright owners of the claimed content.

Thanks for sharing. However this is a 24 year old case with a 9 year old court judgment and the promoter has been acquitted by the courts rather than being convicted. This is a very long time in any person’s life and any person’s behavior / personality can go through massive transformations in such a long time frame. I would not make an investment decision based on this accusation solely given how far back in time this is.

Also, the promoters appear to be relatively minority shareholder friendly in terms of recent actions of share buybacks and regular dividends. They’re also conducting quarterly analyst calls mainly joined by small shareholders which could also be avoided by doing management meets with big PE firms / FIIs / AMCs.

However, if you do find anything else as well please do share that as that could be more clinching evidence for me in terms of the management character and reputation.

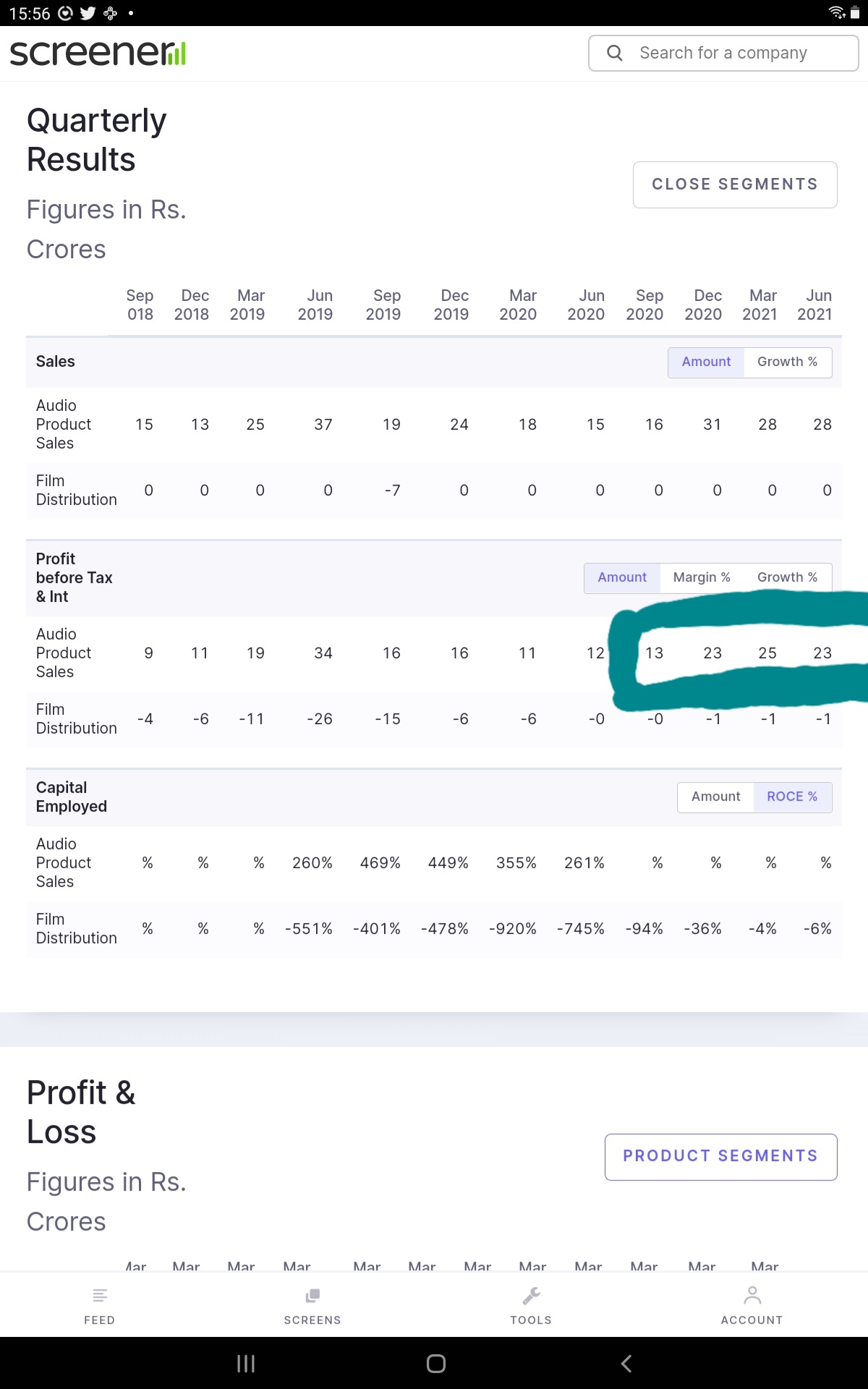

If you look at segment financials, the music business has more liabilities than assets. Capital employed in the demerged music entity will be negligible, ROCE at astronimical levels and growing.

Disclosure: invested

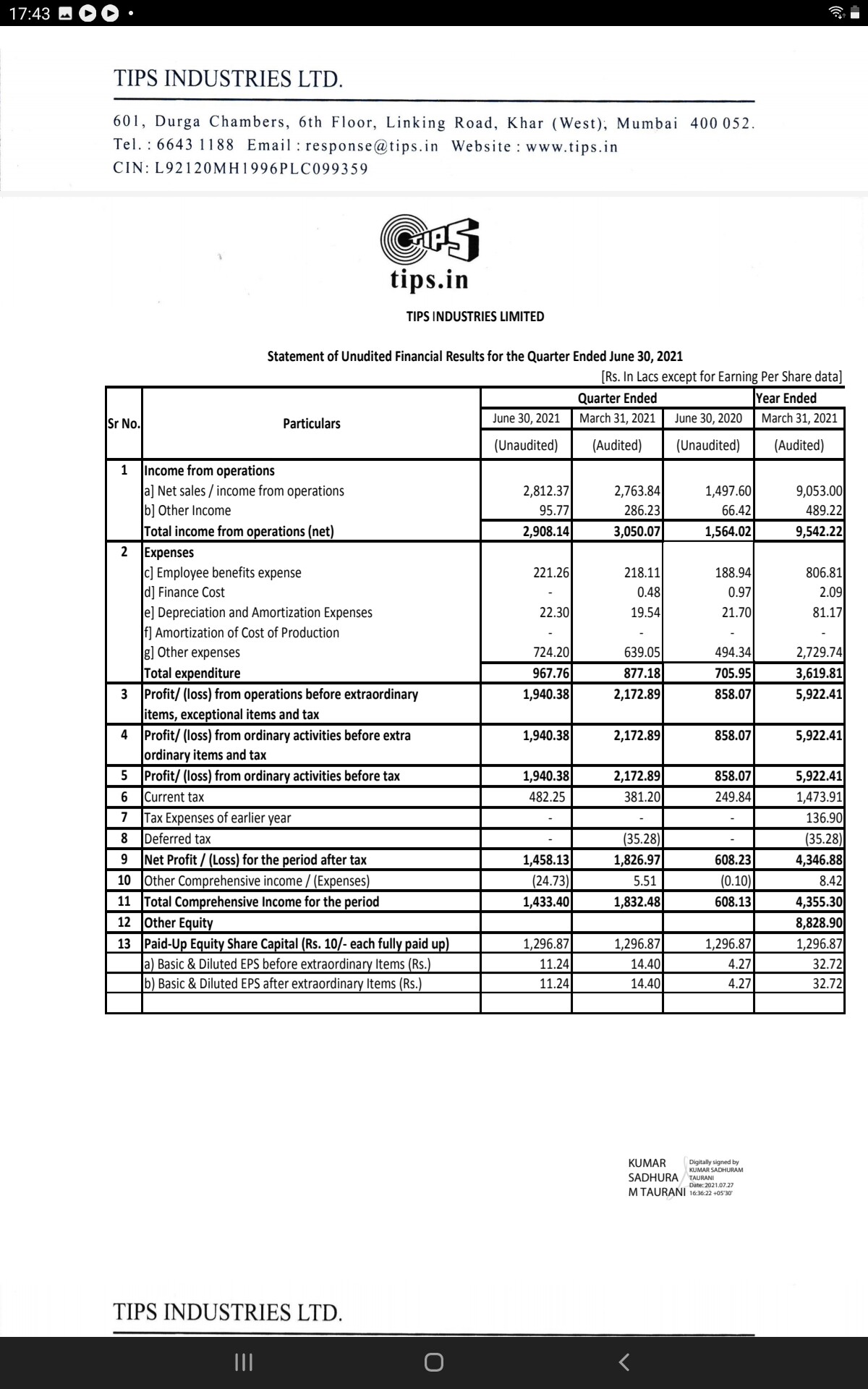

PBT is 20cr. PAT is under 15cr. And while there is growth YoY, for the last three quarters the topline has been flat, which is a cause of concern for me with the narritave of increasing revenues for streaming platforms through higher listenership paid subscribers, leading to growth for licensing companies. The margins seem to be maxing out - it would be unrealistic to expect north of 70 operating margin. So if there is no expansion in top line, then we are likely to get 60cr or so of PAT for the year.

I am curious to hear the management out on their expectation of top line growth, and why it hasn’t moved in nine months.

Q4 concall Tips have called out 25%+ growth for med term, Saregama has called out 20%+ for med term for music segment over concall and annual reports.

QoQ may not be best way to judge as there is some seasonality, eg. Festival season Q3 is usually higher for Music( per Saregama). Again as long as YoY is delivered should be good and inflection point seem to be from Covid onset hence base point.

optimist on this sector - invested in Tips and Saregama.

Reiterated 25-30% growth guidance, any new deal will be on top of it( 2 are under negotiations)

Looking to hire a professional CEO( much required step IMO)

Subscription to drive next leg of growth for industry in line with global trends

Mudic acquisition strategy seems bit unclear and more cost conscious, new artist/low cost etc. Have launch new songs and few doing okay( IMO Saregama is more structured and aggressive here)

Demerger by Nov approx

FY22 can do at 90-100 cr type profit at consol , music segment on own would be higher , Current market cap at 1700 Cr

QoQ flattish but believes new deals in pipeline and renewals which are happening at higher rates will deliver growth

one example given was Facebook deal was at lumpsump and dew for renewal in a year, expect substantial upside on all future renewal deals given heavy usage of music catalog as well as fact that amount is insignificant for value Added by music in social platforms

Next generation of promoter doesn’t seem to be on top of affairs hence professional CEO ( inferences)

Per mgmt threat of new age content/artists/ platforms vs established music labels such as Tips/ Tseries/saregama is negligible ( would be skeptical here as Digital channels in all other industries have created level playing field- need to watch out here for any new age music labels/ owners scaling up…as of now mgmt version seems to be playing out)

This industry is structurally benefited from digitization ( ir respective of covid, is following global trend) and has multiple triggers to continue monetization of content for long time to come

Hi Dev, I believe they did not explicitly mention they are looking for a CEO rather they said they are looking for a “senior person” on the upper level management.

Hi @arjunbadola , they did mention senior professionals to be hired to run the show. Question was asked by someone if new hire will be a CEO equivalent and their response was affirmative. Atleast my notes on con call says so

Once full transcript is out, we can further validate.

FY22 can do at 90-100 cr type profit at consol, music segment on own would be higher, Current market cap at 1700 Cr

I just heard the entire 1QFY22 results concall. I dont think the company gave any guidance for consolidated profits explicitly. What they said is FY21 topline of Rs91crs can be grown 25-30% and same growth can be maintained for bottomline. Profit in FY21 was Rs43crs. That implies FY22 profits of Rs54crs- Rs56crs.

@Dev_S where did you get this Rs90-100crs profits from? Is that your estimate? Or was it mentioned in the 4QFY21 concall?

Look at music segment profit( PBIT) on TTM basis …already hovering around 94 cr( post tax around 80 Cr at 25% tax rate) - projections are based on this number for FY22, Q3 and Q4 are relatively stronger quarter, Films have been in loss making hence lower figure for net profit.

Mgmt guided for 25-30% growth range , own projections were on music can do 100 cr+ profit, am optimist that there could be upside potential, not because of only mgmt efforts but simply sector tailwinds being too strong.

Again I could be wrong, novice and still learning.