See more number of songs does not directly equals to more revenues. If that would have been the case then Saregama with 4x the number of songs as compared to Tips should had 4x revenues right? Tips has ~100 crores from Music licensing, whereas Saregama has ~283 crores.

It is the success of music track itself that makes you money, because your revenues from the streaming services depends on the stream share and not the number of songs that you have.

This recent movie of Salman- Radhe’s music rights were sold for ~30 crores from what I have read. And I don’t think that the movie’s music is that successful. So there is skillset that is involved in acquiring rights. And Tips management has prove themselves with new content acquisition. Saregama has already displayed that with some latest music acquisition from big upcoming movies, obviously at what cost they have acquired the same is not known.

On valuation front, I think people have to stop looking at P/E ratio as displayed by various websites like screener and all, because those ratios are direct calculation. TIPS market cap is ~1200 crores, music business PAT is ~40-50 crores. So Tips is actually trading at 20-30x earnings and not 50x or so that these screener and all would display.

And with music business being so profitable and growth possibility also being good; I think there is enough scope of valuation growth in the current market environment wherein even LaLa businesses have 20-30x valuations.

Thank you for your detailed reply. I was looking at the number of songs as a proxy to the stream share. Obviously it not a perfect parallel for revenues, like you pointed out.

Essentially music reveues have two important parts = Stream share x Total revenues of the platform.

Stream share = TIPS songs streamed / All songs streamed

All songs streamed is increasing, and I guess reasonably fast. I am keen to understand what rate TIPS songs will be able to increase.

And ofcourse the quality of songs that they add makes a big difference. Seems like streams per song for TIPS is about 30% higher that Saregama from the revenue numbers you have shared (is this correct?). That said, at the end of the day, with more songs getting added to every streaming platform everyday, TIPS will have to add songs (and good songs) to maintain their stream share. It seems difficult to assess how this will pan out.

And so the actual increase in revenues seems to depend mainly on the increase in revenues of the streaming platforms themselves, and that will be the main driver of growth for TIPS. Now we know that the total global streaming revenues have increased by 20%+ CAGR over the past 3-4 years. Are the numbers for India similar? Is this trend likely to continue / increase / decrease? I’m not sure how to answer this question.

Since paid subscription make up about 75% of streaming revenues for platforms (rest 25% though Ads), I think the real monitorable or projection that we should try to make is what is likely to be the growth in paid subscriptions in India on streaming platforms. I think this is what will be the real game changer for TIPS and Saregama. Is there any study /trend that you have come accross on this?

1/ in short to mid term, the biggest trigger for music labels is the growth in paid subscription in music streaming. This variable will benefit both the cos. Key variable to track is how paid subscriptions has grown in last 2 yrs in India. Do we have this number?

2/ but in long term, once the paid subscriptions are matured, the growth will come from new content acquisition by these cos. Here we need to deepdive into what is the strategy of TIPS and how much money they spend in acquiring content in last 2-3 years vs industry total spend. Do we have this data?

Very good point Vineet. I think in the long run, its new acuisition which holds greater importance than paid subscription.

Given how T series is everywhere( regionals as well) in recent times, we need to be watchful of TIPS strategy.

Saregama preference seems to be more towards regional music (Bhojpuri and I guess Gujarati). They are aware about competition in Punjabi( T series is big there, Speed records and many other players, so difficult to make inroads)

Notes from the Earnings con call today. Jotted down in a hurry, tried to be as accurate and objective as possible, there may be minor mistakes

Clarification on Balance Sheet

There is an entry in balance sheet under non-current liabilities amounting to 37 Cr. Management clarified that this is erroneously placed under wrong heading (Employee benefit obligations… there are 2 entries there). These are actually advance payments from customer contracts. It was later clarified that most of the advances are for 1 year contracts but there is one contract of 2+ years period

Growth Guidance

68% revenue from digital channels, about 30% revenue from non-digital channels

Management is confident of delivering 20% to 25% growth over the next 3 years. They expect digital revenue to grow by 30% to 35%.

We are currently no 5 player in Indian music industry. Aspiration is to be the no 3 player in next 2-3 years

Size of the no 3 music player is in 175 Cr to 200 Cr range

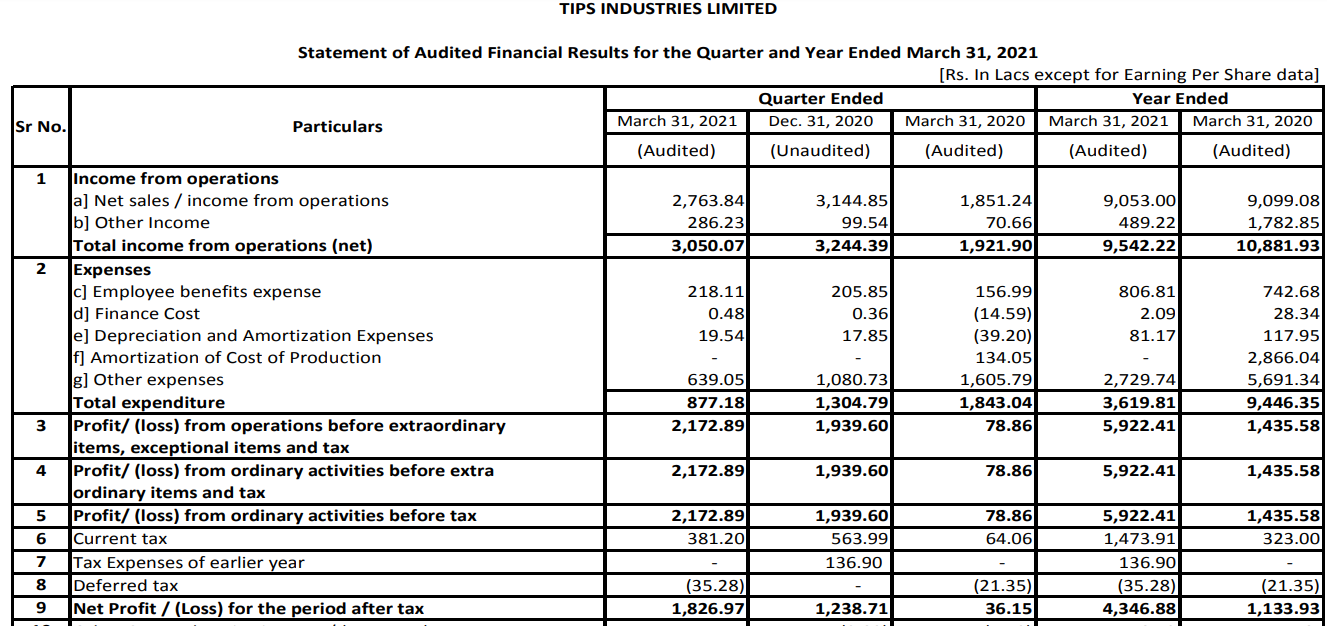

EBIDTA margin has grown, but is sustainable. Last year, we did some write-offs relating to films business, hence EBIDTA had fallen.

Covid Impact

Q1 & Q2 were weak, but we did well to recover in last 2 quarters.

Licensing revenue from events & live performances were hit badly due to covid situation. Revenue hit due to this was about 10%. Though, they have a very good deal in place with a partner to monetise, covid situation was a dampner.

Revenue from this channel had recovered very well in Q3 / Q4. Second round of lockdown has again been a dampener, though looking at the sharp recovery seen post 1st lockdown, management is very confident that a similar sharp recovery will be seen starting Q2 this year.

Catalog

About 29000 songs catalog. About 12000 are Hindi songs. Remaining are regional songs

Most of the content comprises of very popular hit songs of 90s and 2000s.

Catalog Longevity

Catalog has high number of hits. Can continue to deliver 20% to 25% revenue growth for next 2-3 years, even if we do not add much to the catalog,

With so many hits in catalog, we can continue generating revenue by recreating old hit songs (Gave example of 2-3 old hit songs which have been recreated and released recently, which have garnered massive attention recently)

Content Acquisition

Spent 12 Cr on content acquisition in previous year

Spent 10 Cr on content acquisition in this year. Spending on acquisition is low as there have been no major releases

Future content acquisition focus will be on buying bollywood music as well as producing own music

With normalisation of business, looking at spending 25 to 30 Cr on content acquisition

Will not buy content at any cost for sake of buying. Will buy if it makes business sense and can payback within certain time. Typically, content should payback in 2 to 3 years

30-35 songs are already in pipeline in this year, many will be recreated songs (A & B+ category songs)

There is some cost of recreation (engaging new music director, lyricist, video etc), though this can be controlled well.

Reinvesting of Cash flows - will prefer investing in content acquisition

Idea is to acquire quality content so that 20 years from now, whoever is running the company still has valuable content to monetise

Have signed up with 5 new artist for music. Have a 360 degree contract with them. Will generate revenue from not just recorded music, but also will handle their events / live performances.

Accounting & Content Expense

Content is charged to P&L, it is NOT capitalised.

Operating cost in current form is about 20 Cr

So given current cash flows, a substantial amount can be budgeted for content acquisition

Content Deals / Structure

No company expects huge revenue from radio.

There is an effort (by all music companies) to renegotiate licensing terms with radio industry. The matter is in court, but we expect this to be settled one way or the other

Have a mix of deal structures with other digital customers

Revenue sharing model OR Lump-sum outright with Minimum guaranteed (MG) payments

One or two indian OTT players (Jio Saavn) are on Lump-sum with MG. They are still evolving their systems to have detailed accounting reports

Most deals are annual deals, with significant (about 5 to 10%) incremental pricing negotiated on renewals

OTT guys pay about 10 paisa per stream

Most big guys such as spotify, Amazon etc have very detailed reporting, which provides ways to validate

Even with customers with whom we have fixed sum deal, we ask them for detailed reports, which we evaluate regularly

Ad revenue share with google on YouTube

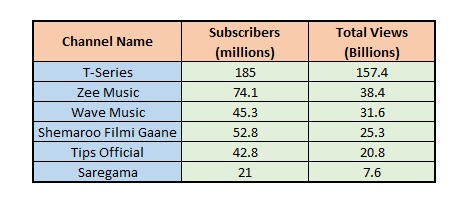

We have total of 14-15 different channels on YouTube, with cumulative subscriber base of 64 million users

Customer typically pay out on quarterly basis

Warner has Global deal with Apple, Amazon and Spotify. We have a deal with Warner, so out content is available on global platforms through warner deal

Have a lump-sum deal with FB.

Had a dispute with Gaana in 2020. Their 2 year old contract came up for renewal in May 2020, at peak of lockdown. Negotiations for renewal broke down over revenue increment, so Gaana decided to pull down Tips catalog.

If any OTT app does not have content catalog from the leading 5 players, they suffer. They realised their mistake and are now discussing a new contract. Hopefully, they will sign a new contract very soon.

Revenue Potential

We have a fixed sum deal with FB. Narrated an interesting fact about this. FB signed with partners on a fixed sum basis for 2 years, till their systems and processes evolve and stabilise. They share detailed reports. In 1st month Tips content was accessed 50 crore times. In 2nd month, the it gathered 100 Cr hits, in 3rd month 200 Cr and in 4th month 400 Cr!! Hits doubled every month!! Imagine the revenue potential!

If the OTT apps add subscribers as some of the reports suggest, the potential can be massive. Ad-based model will never go away in a country like India. But if the subscription-based model stabilises and grows, we can see 70 to 80% YoY growth in revenues for some time.

Films Division

Bhoot police (hope I got the name right ) is the only film being made this year

Films business is being demerged

Post demerger, all movie rights will be under demerged company

We will need funding for the films company, or a production partner. We are exploring those options

Will continue to produce 2-3 movies / web-series per year

Will come back with firm plans in 2 quarters, by around the time of demerger

Demerger

All music rights will be under music company, and films rights will be under films company

We have separate staff even today for both the divisions, so staff will be split accordingly

Management responsibilities of both the company will be shared by promoter family

Demerger should be complete within next 2 quarters

Corporate Governance

Lack of corporate governance in bollywood related companies is more of a perception problem

We have been listed since 2001, we have seen several ups and downs, financially and business wise. We were ravaged by piracy and other challenges, but we continued focussing on the core business

Even when several companies have mishandled their finances, we have always focussed on creating good business. Only those companies which have created solid content will stand in the long run, rest will vanish

We have 3 reputed directors on the board from leading companies

We are committed to creating value for investors

Succession planning - Son (Girish) is actively involved in day-to-day working of the company

We did a 19 Cr buyback recently

If we do not spend on content acquisition, we are open to giving substantial dividends to shareholders

DISC: Invested in Tips recently & in Saregama from lower levels.

I think, he was talking about a bhojpuri film being made this year.

I think majority of the non-current liabilities of 37.3 cr. came from advances from facebook deal, even though management didn’t say that explicitly. he mentioned that they have a fixed price deal with facebook for 2 years and not in ad revenue sharing model yet. But they seen phenomenal 100% MoM growth in facebook in first 4-5 months of association. Viewership has grown from 50L,1,2,to 4 cr in 4 months. So in future the deal may be on ad revenue sharing basis.

Any idea, how much content Tips company buy with 25-30 Cr, they have allocated.

They can make their own music, with new artist. That won’t cost much. But with new movie or reputed artist might be costly, to acquire lot of content.

How are they planning, to be No 3 in the industry, as stated in concall.

Digitalization has changed the game, but wait…

Just a point from my side, I have seen many downloading latest movies , music, series etc directly from telegram without any subscription!!!

Why all content owners ignoring such open theft like telegram ?

Makes a compelling case.

Though I don’t think there’s any merit in assuming that this may pan out anytime in the medium term. Is there a lobby already pushing for amendments to the act?

No specific source for the info, but I am certain that T-Series is at the top of the pile, and Saregama is also part of top 3. The other possible candidates in top 5 (besides Tips) could be Sony and Yash Raj music (I think they own and distribute music for all their films). Zee music also distributes music for movies produced by their production house. But only 2 of these players are listed - Saregama and Tips.

A quick search did not yield any current info on hindi film music deal pricing, but a dated 20 year old news article does provide glimpses into the deals done around year 2002 (link Hindi Film Music Industry Gets Real On Rights). The figures for music rights of blockbusters of the era are indicated in the range of 5 to 10 crores! The world has changed a lot in these 2 decades, so its likely the economics of the hindi film music would have changed too. But based on these figures, does not seem that 25 - 30 crores can buy much in current times - possibly 2 to 3 A-list movies at the most.

Above list is only based on one channel (Hindi Songs). Music labels maintain different channels for different languages. Numbers are as on today (22-06-2021)

Thanks.

They are talking out becoming No 3 player for that catalogue need to be improved. I understand their is a recall of old music. But that parameter is for all music players.

Large part of music is still coming from movies, these movies right are costly.

Sanjay Lella Bhansali / Devdas music right were sold at 12 cr around 2010-2012.

Want to understand ,what are drivers which will improve its position.

Good info Ravindra Mutyala

Surprised to see Saregama is having lower views (only in one channel). However, I believe there will be good uptick in number of views and subscriber as they start publishing new songs. Recent is song from badshah, which garner 120 million views in 2 weeks. That is why TIPS is preferable to investors compared to saregama.

However saregama have to two more cylinders, Physical products ( carvaan) and Film and web series , TV serials. I believe these business are difficult to earn money, however they learned lesson in 2019 and spend money wisely.

Disclosure: Missed TIPS, Invested in saregama.

) is the only film being made this year

) is the only film being made this year