YouTube subscribers collectively have reached 93 million across all our channels.

recorded 47 billion YouTube views, reflecting a 52% growth because of Shorts.

songs released this quarter are 165, of which 82 were film songs and 83 were non-film songs.

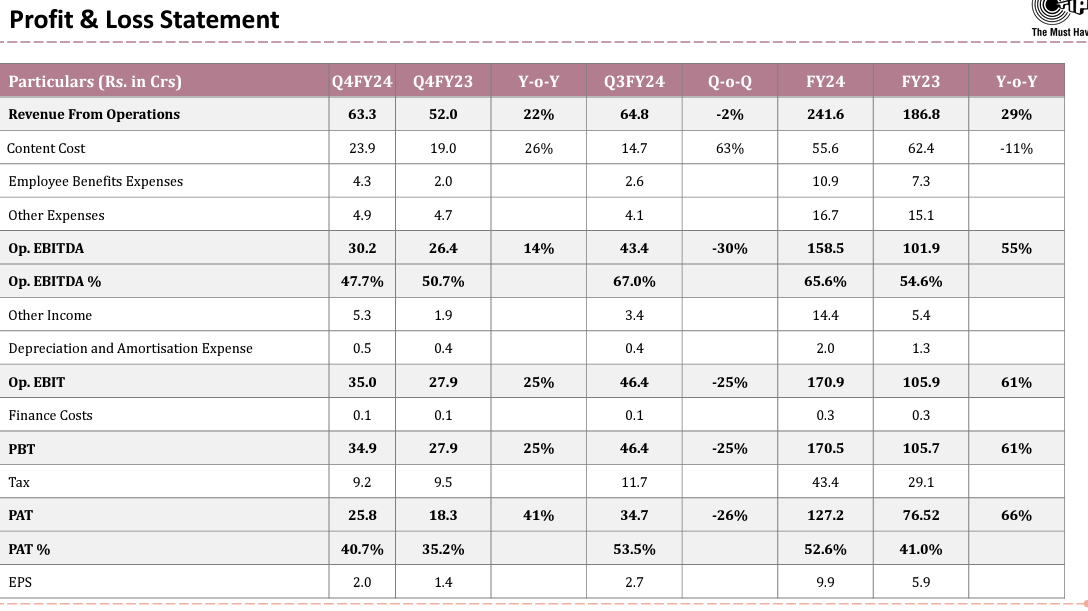

Profit after tax for Q3 FY ‘24 stood at INR34.7 crores versus INR20.2 crores in Q3 FY '23. That is a growth of 72%. PAT margins for the quarter was 53.5%.

Content cost for the quarter was INR14.7 crores.

digital business is around 75%, 76%.

We have a good pipeline of Ishq Vishk, Buckingham Murders, The Crew.

Our industry is around INR2,800 crores-odd. three years to five years, this industry has potential to grow INR10,000 crores, INR12,000 crores.

Even. one song or one promo will be released, we write-off 100% in that same quarter.

Digital is 75%, 76%. And non- digital, which is live performances, TV, sync rights, all those are 24%, 25%.

YouTube Shorts is a fixed fee deal.

YouTube is 45% to 50% of our total business, top line.

MANAGEMENT GUIDANCE

100- 125 will be released in Q4.

Top line 30% and bottom line 30%.

Meta reels good news to be expected soon.

40% – 35% of content we will acquire from Tips Films. And 30%, 35% content we will acquire from outside. And 25% we will create on our own.

RISK

The promoters have sold around 6% stake in Tips Industries to grow our film production business.

Promote may sell more stake to fund Tips films.

Content acquisition is very tough, particular content deserves INR5 crores, people are offering INR15 crores, INR18 crores. So, we are not following that path and we are not bidding anything.

Stance: Invested, Looking to add more in case of dips

Don’t think there is any news on this behind the recent rally.

I guess this is what the bull market does. However, the business continues to show strong fundamentals.

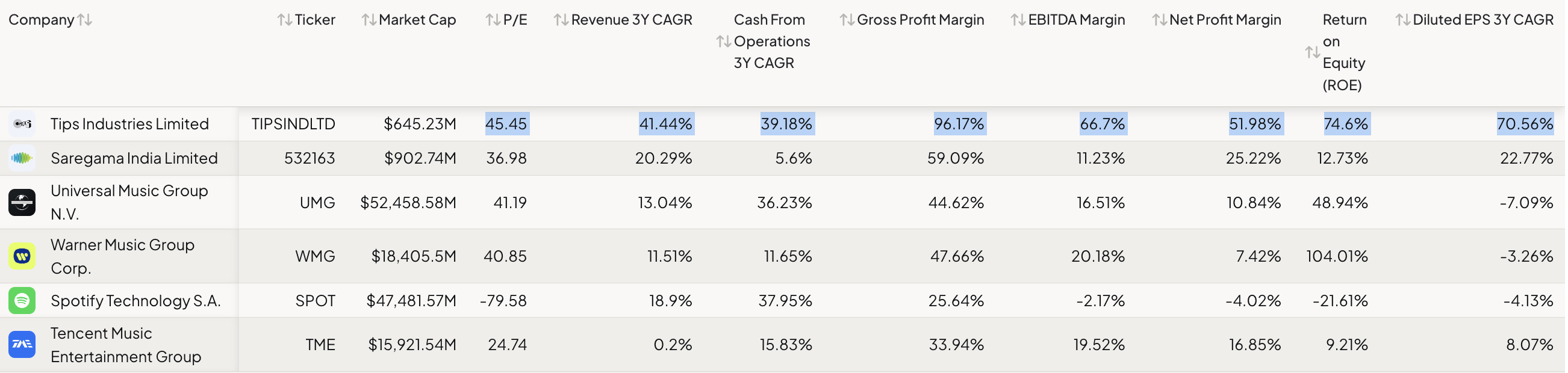

In fact, PE ratio of global music labels are also >40 presently.

Warner Music - ~40 PE

Universal music - ~42 PE

Generally, there is a premium for Indian companies; Hence, the valuation of 50 PE for Tips can be justified, because they show strong promise of 30% growth.

However, nothing can be said about valuations in bull markets. Given the business model is superb, I may add this whenever there is a drop in price.

While I have not done an in-depth study of its global peers, I am keen to do it now considering its growth has been feverish thus far and at the same time valuation has been stretching beyond its 3/5y median PE.

However, looking at the global/domestic peer set, valuation vis-a-vis growth over time is the best in class.

@ankush12495 Sorry to bother and I don’t know if you still hold but would love to hear your thoughts on the same. thanks in advance.

Disc: Invested from 2021 levels (position size here). No transactions in the last 30 days.

Globally I think the markets are realizing the longevity of growth & terminal value that exists in these business on the back of their IP.

Monetization of music IP will only expand over the years, short format monetization has just started in the global markets and changes within streaming players wherein only streams over a certain count will be counted for monetization are some of the recent steps that further improves the monetization for these players.

In India music labels are even better placed as they have both master recording & publishing rights, plus some players like Tips have entire IP with no royalty and thus margins are higher. The growth is obviously top notch for Tips as it has gone from inefficient player to a decent player.

(Disclosure: SEBI Registered RA. Invested and Active recommendation in Research Service)

What is your view on the sustenance of growth (30% topline and bottom line) beyond 3 years?

What I feel, following are the growth levers

New listeners: Music library getting older day by day is my concern. However, paid listeners should keep on increasing for downstream platforms as a secular trend for longer.

New monetization channels: Short video content, Instagram - probably these are the only few monetization ways with some juice left.

I feel the growth would be high, whether it would be 30% or 5-10% here or there I don’t know.

The biggest low hanging fruit currently is proper monetization of shorts, Tips has already pulled its content from Instagram and I think the new deal would happen at a substantial amount whenever that happens.

And in the longer run, people will have to pay for convenience of streaming music like they are paying for now for say food delivery etc and that would trickle down to music labels.

I have shared some thoughts on monetization of convenience here if you are interested-

The CEO mentions that this means Tips catlog will be distributed via Meta as well. If that interpretation is true then the company should do even better growth over the next 4 quarters.

I would like to think that the newly hired CEO had a role in this deal. Maybe we will get more information next quarter

I am still positive on this stock. There has been a series of good news coming -

Global Deal with Warner music for entire library - This will increase the revenue and profits, as management told that this deal is multiple times bigger/ better Vs last time’s partial deal.

Buyback announced on INR 625. Also, even at this price, the promoter is not participating and selling its stake. They know the future revenue profile. I guess it is a way to improve own promoter shareholding for what Tips can become.

I am just not sure whether this is my rationality, or recency bias (Impact of bull run)? Any other thoughts?

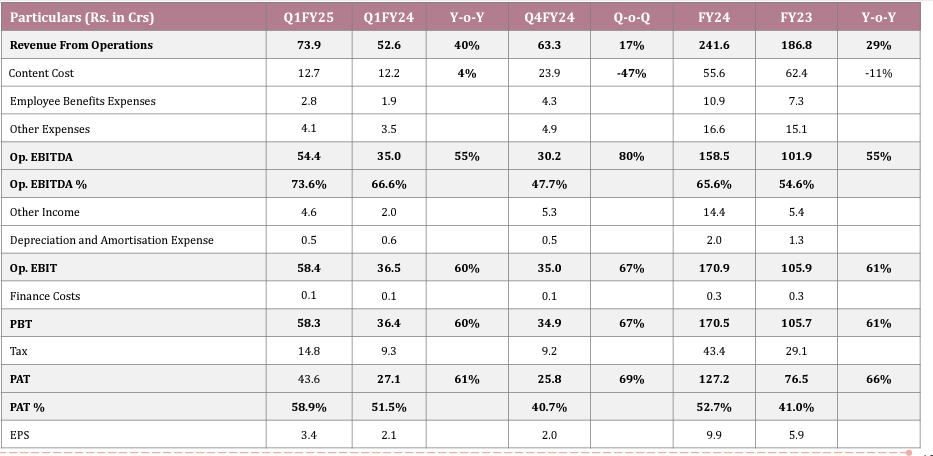

On the concall management was confident of 30% revenue and profit growth in FY25. Based on that FY25 profits should be Rs165 crs which implies the stock trades at 36.8x FY25E P/E

The OPM is going through the roof since they have not been able to acquire content, due to intense competition. We need to evaluate what kind of margins they will have going forward. Once the content acquisition resumes, the yoy results might start moderaing as margins will go down as per my understanding.